Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

CPA / CMA REVIEW QUESTIONS

CPA Exam Questions

1. b. The entries to record the stock issuance and subsequent acquisition and

retirement (per share) are as follows:

Issuance

Cash ............................................................................... 25

2. c. A treasury stock account is created when a company reacquires its own

stock as treasury stock. The full purchase price (cost) is debited to Treasury

Stock. When treasury stock is sold, the Treasury Stock account is credited

18–42 Intermediate Accounting, 8/e

CPA Exam Questions (concluded)

3. b. Property dividends are recorded at the fair value of the property distributed

as of the date of declaration, with any gain or loss being recognized in the

4. c. The number of shares issued is less than 20—25%. Therefore, the

transaction is considered a small stock dividend and retained earnings should

5. a. When a company issues a stock dividend, earnings per share decreases as the

6. b.

$100,000

7. c. Both U.S. GAAP and IFRS require that mandatorily redeemable preferred

8. c. Both U.S. GAAP and IFRS require that companies report a statement of

CMA Exam Questions

1. b. Par value represents a stock’s legal capital. It is an arbitrary value assigned

2. c. Common shareholders usually have preemptive rights, which means they

have the right to purchase any new issues of stock in proportion to their

3. b. A stock dividend is a transfer of equity from retained earnings to paid-in

capital. The debit is to retained earnings, and the credits are to common

stock and additional paid-in capital. More shares are outstanding following

PROBLEMS

Problem 18–1

PART A

Jan. 9

($ in millions)

Cash (40 million shares x $20 per share) ....................................... 800

PART B

Jan. 12

($ in millions)

Land ........................................................................................ 2

Revenue—donation of land ............................................... 2

Sept. 1

($ in millions)

Common stock (2 million shares x $1 par) .................................. 2

Dec. 1

($ in millions)

Cash ........................................................................................ 26

Problem 18–2

Requirement 1

a. February 5, 2016

($ in millions)

Retirement Treasury Stock

Common stock (6 million sh. x $1) 6 Treasury stock (6 million sh. x $10) 60

Paid-in capital—excess of par Cash 60

b. July 9, 2016

Cash (2 million sh. x $12) 24 Cash (2 million sh. x $12) 24

c. November 14, 2018

Cash (2 million sh. x $7) 14 Cash (2 million sh. x $7) 14

18–46 Intermediate Accounting, 8/e

Problem 18–2 (concluded)

Requirement 2

Shareholders’ Equity $ in millions

Treasury

Retirement Stock

Paid-in capital:

Common stock, $1 par, .................................................. $ 238 $ 240

* $1,680 – 42 + 22 + 12

** $1,100 – 11

*** $1,100 – 1

or, alternatively:

Paid-in capital:

Common stock, $1 par, .................................................. $ 238 $ 240

Problem 18–3

Requirement 1

February 15, 2016

(a) Retired

Common stock (300,000 shares x $1 par) ......................... 300,000

February 17, 2017

(a) Retired

Common stock (300,000 shares x $1 par) ......................... 300,000

Problem 18–3 (concluded)

November 9, 2018

(a) Retired

Cash (200,000 shares x $7) ............................................... 1,400,000

Common stock (200,000 shares x $1 par) ..................... 200,000

Requirement 2

Shareholders’ Equity

SHARES RETIRED TREASURY STOCK

Paid-in capital:

Common stock, $1 par, ........................................ $ 5,600,000 $ 6,000,000

or, alternatively:

Paid-in capital:

Common stock, $1 par, ........................................ $ 5,600,000 $ 6,000,000

Additional paid-in capital ..................................... 28,350,000 30,000,000

Problem 18–4

2014

Retained earnings ........................................................ 160,500

Income summary ..................................................... 160,500

2015

Income summary ......................................................... 2,240,900

Retained earnings ................................................... 2,240,900

2016

Income summary ......................................................... 3,308,700

Retained earnings ................................................... 3,308,700

Retained earnings (given) ............................................. 242,000

18–50 Intermediate Accounting, 8/e

Problem 18–5

Requirement 1

2016

a. November 1—declaration date

Retained earnings ......................................................... 84,000,000

2017

b. March 1—declaration date

Investment in Warner bonds ........................................ 300,000

March 13– date of record

no entry

April 5– payment date

c. July 12

Retained earnings (5,250,000* x $21 per share) .............. 110,250,000

Common stock ([5,250,000* – 250,000] x $1 par) .... 5,000,000

Problem 18–5 (continued)

d. November 1—declaration date

Retained earnings ........................................................ 88,000,000

Cash dividends payable (110,000,000* x $.80) .............. 88,000,000

* 105,000,000 + 5,000,000 = 110,000,000 shares

2018

e. January 15

Paid-in capital—excess of par** ................................. 55,000,000

Common stock (55,000,000* shares at $1 par) ............. 55,000,000

f. November 1—declaration date

Retained earnings ........................................................ 107,250,000

Cash dividends payable (165,000,000 * x $.65) ............. 107,250,000

Problem 18–5 (concluded)

Requirement 2

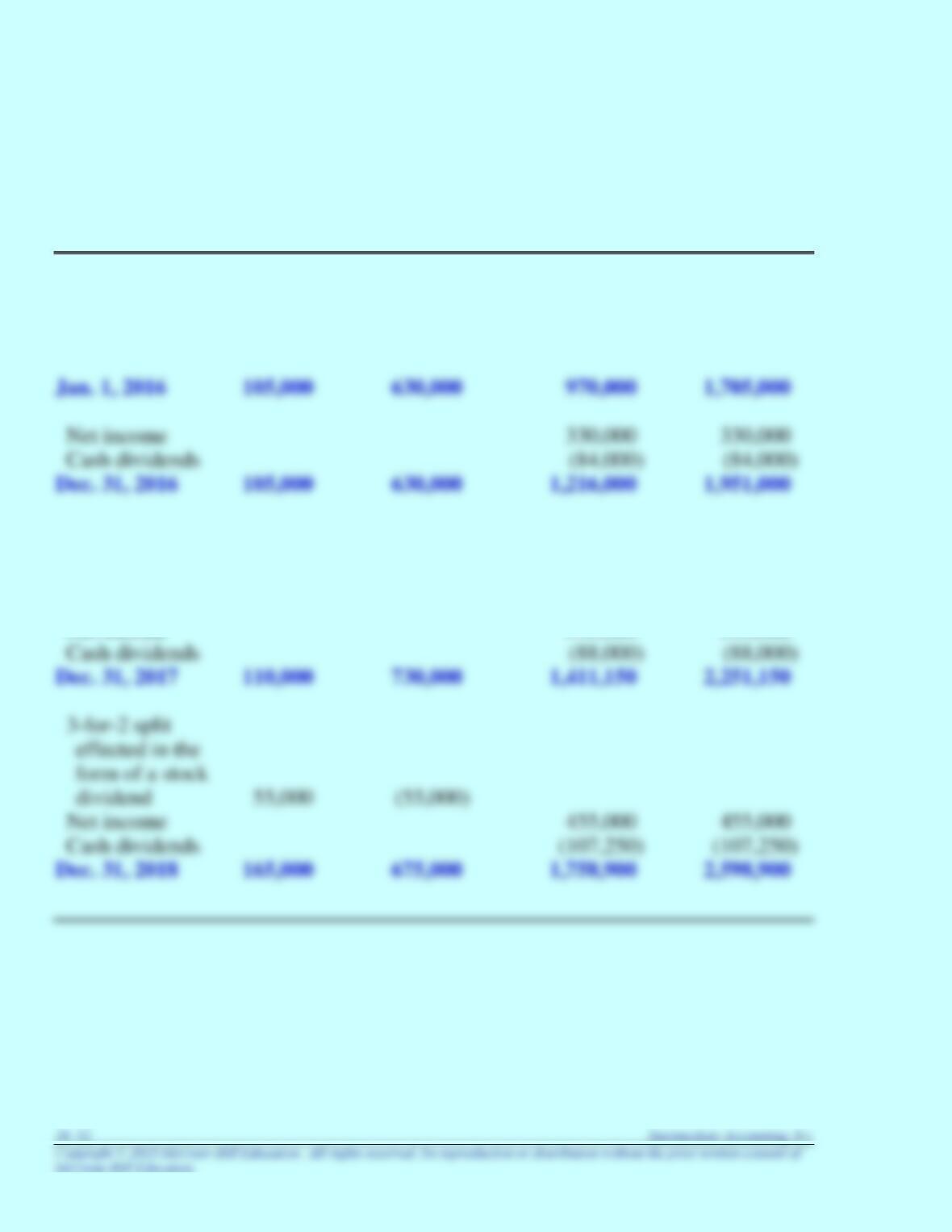

BRANCH-RICKIE CORPORATION

Statement of Shareholders’ Equity

For the Years Ended Dec. 31, 2016, 2017, and 2018 ($ in 000s)

Common

Stock

Additional

Paid-in Capital

Retained

Earnings

Total

Shareholders’

Equity

Property

dividends

(1,600)

(1,600)

Common stock

dividend

5,000

100,000

(110,250)

(5,250)

Net income

395,000

395,000

Problem 18–6

Requirement 1

2016 ($ in millions)

Cash ........................................................................................ 480

Preferred stock (1 million shares x $10 par per share) ............... 10

Paid-in capital—excess of par, preferred ........................... 470

Cash ........................................................................................ 70

2017 ($ in millions)

Common stock (3 million shares x $1 par) .................................. 3

Paid-in capital—excess of par (3 million shares x $9*) .............. 27

18–54 Intermediate Accounting, 8/e

Problem 18–6 (continued)

($ in millions)

Retained earnings ................................................................... 1

Cash dividends payable, preferred ................................... 1

Cash dividends payable, preferred ........................................ 1

2018 ($ in millions)

Retained earnings .................................................................. 65

Common stock .................................................................. 6

Paid-in capital—excess of par, common ........................... 59

Problem 18–6 (concluded)

Requirement 2

ANACONDA INTERNATIONAL CORPORATION

Balance Sheets

at December 31

2018 2017

Shareholders’ Equity:

Preferred stock $ 15 $ 15

Problem 18–7

Requirement 1

The statement of shareholders’ equity explains why and how the various

Requirement 2

Cisco accounts for its share repurchases by formally retiring them. The

Requirement 3

The price Cisco paid for the shares repurchased during the period shown was

more than the average price at which Cisco had sold the shares previously. We know

this because the Statement of Equity reports a reduction in retained earnings resulting

Problem 18–7 (continued)

Requirement 4

Comprehensive income is the total nonowner change in equity for a reporting

period. It encompasses all changes in equity other than from transactions with

owners. Transactions between the corporation and its owners primarily include

Requirement 5

The change in Comprehensive income in the period presented was due to (1) net

income ($3,425 million) and other comprehensive income (OCI) ($95 million). OCI

consists of some unreported combination of (1) net unrealized gain/loss on investment

18–58 Intermediate Accounting, 8/e

Problem 18–7 (concluded)

As we noted in Chapter 17, gains and losses, and prior service cost for

pensions and other postretirement benefit plans are not recognized currently

in earnings. Instead, we report them as part of other comprehensive

income.

Problem 18–8

Requirement 1

Cash ($385,000 – 1,500) .......................................................... 383,500

Requirement 2

Retained earnings ................................................................ 60,000

Requirement 3

Cash dividends payable ...................................................... 60,000

Cash ................................................................................ 60,000

Requirement 4

Common stock (10% x $30,000) ............................................. 3,000

18–60 Intermediate Accounting, 8/e

Problem 18–9

Assumption A – noncumulative

Preferred Common

Total $150

Current preference $10 (10% x $100) (10)

Assumption B – cumulative

Preferred Common

Total $150

Dividends in arrears:

-2015 $10 (10% x $100) (10)