Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

A

AP

PP

PE

EN

ND

DI

IX

X

A

A

D

De

er

ri

iv

va

at

ti

iv

ve

es

s

L

Le

ec

ct

tu

ur

re

e

O

Ou

ut

tl

li

in

ne

e

Derivatives

A. Derivatives are financial instruments that “derive” their values from some other security or

index. (TA-1)

B. They are extensively used to hedge against various risks, particularly interest rate risk.

C. Hedging means taking a risk position that is opposite to an actual position that is exposed

to risk. (TA-2)

1. Interest rate futures are derivative contracts often bought and sold to hedge against

risk. They allow a firm to sell (or buy) a financial instrument at a designated future

D. All derivatives, no exceptions, are carried on the balance sheet as either assets or liabilities

at fair value. When the fair value changes, a gain or loss occurs. (TA-4)

1. If the derivative is not designated as a hedging instrument, or doesn’t qualify as one,

E. When a derivative designated as a fair value hedge is adjusted to reflect changes in fair

value, the resulting gain or loss is included currently in earnings. At the same time,

though, the loss or gain from changes in the fair value, due to the risk being hedged, of the

item being hedged also is included currently in earnings. (TA-5) (TA-8)

F. When a derivative designated as a cash flow hedge is adjusted to reflect changes in fair

A-2 Intermediate Accounting, 8/e

G. A foreign currency hedge can be a hedge of foreign currency exposure of: (TA-7)

1. a firm commitment – treated as a fair value hedge.

H. To qualify as a hedge, the hedging relationship must be “highly effective” in achieving

offsetting changes in fair values or cash flows. Hedge accounting must be terminated for

hedging relationships that no longer are highly effective. (TA-9)

P

Po

ow

we

er

rP

Po

oi

in

nt

t

S

Sl

li

id

de

es

s

A PowerPoint presentation of the Appendix is available at the textbook website.

T

Te

ea

ac

ch

hi

in

ng

g

T

Tr

ra

an

ns

sp

pa

ar

re

en

nc

cy

y

M

Ma

as

st

te

er

rs

s

The following can be reproduced on transparency film as they appear here, or

DERIVATIVES

Derivatives are financial instruments that “derive” their

The most frequently used derivatives are:

o Financial futures

Derivatives can manage or hedge companies’ exposures to

risk, including interest rate risk, price risk, and foreign

exchange risk.

TA-1

A-4 Intermediate Accounting, 8/e

DERIVATIVES USED TO HEDGE RISK

Hedging means taking a risk position that is opposite to an

actual position that is exposed to risk.

A forward contract is similar to a futures contract but does

not call for a daily cash settlement for price changes in the

underlying contract. Gains and losses on forward contracts are

paid only when they are closed out.

An option gives its holder the right either to buy or to sell an

INTEREST RATE SWAP

Swap of annual payments on $100,000 notional amount; fixed

interest rate: 10% ($10,000)

TA-3

A-6 Intermediate Accounting, 8/e

ACCOUNTING FOR DERIVATIVES

All derivatives, no exceptions, are carried on the balance sheet

How we account for the gain or loss depends on how the

derivative is used.

1. If the derivative is not designated as a hedging

2. If the derivative is used to hedge against exposure to

risk, the gain or loss is either

TA-4

FAIR VALUE HEDGES

A change in either prices or interest rates can cause a change

in the fair value of an asset, a liability, or a commitment to buy

A gain or loss from a fair value hedge is recognized

immediately in earnings along with the loss or gain from the

item being hedged.

o When the derivative is adjusted to reflect changes in fair

TA-5

A-8 Intermediate Accounting, 8/e

CASH FLOW HEDGES

If a derivative is used to hedge against exposure to changes in

cash inflows or outflows of an asset or liability or a forecasted

transaction, it can be designated as a cash flow hedge.

When the derivative is adjusted to reflect changes in fair

Comprehensive income includes net income itself and

changes in elements of the balance sheet that the FASB feels

don’t (yet) belong in net income:

o foreign currency translation adjustments

FOREIGN CURRENCY HEDGES

The possibility that foreign currency exchange rates might

change exposes many companies to foreign currency risk.

• a forecasted transaction – treated as a cash flow hedge.

• a company's net investment in a foreign operation – the

TA-7

A-10 Intermediate Accounting, 8/e

ILLUSTRATION

INTEREST RATE SWAPS

Wintel Semiconductors issued $1 million of 18-month, 10% notes

payable to First Bank on January 1, 2016. Wintel is exposed to the risk that

general interest rates will decline, causing the fair value of its debt to rise.

To hedge against this fair value risk, the firm entered into an 18-month

Illustration A-1

TA-8

Floating settlement rates were 9% at June 30, 2016, 8% at December 31,

2016, and 9% at June 30, 2017, and December 31, 2017. Net interest

receipts can be calculated as shown below. Fair values of both the

derivative and the note resulting from those market rate changes are

assumed to be quotes obtained from securities dealers.

1/1/2016 6/30/2016 12/31/2016 6/30/2017

Fixed rate 10% 10% 10% 10%

Illustration A-1

TA-8 (continued)

When the floating rate declined from 10% to 9%, the fair values of both the

derivative (swap) and the note increased. This created an offsetting gain on the

derivative and loss on the note. Both are recognized in earnings the same period

(June 30, 2016).

January 1, 2016

Cash ..................................................................... 1,000,000

Notes payable ......................................................... 1,000,000

To record the issuance of the notes.

June 30, 2016

Interest expense (10% x ½ x $1 million) ................... 50,000

Cash ..................................................................... 50,000

The net interest settlement on June 30, 2016, is $5,000 because the fixed rate is

Illustration A-1

TA-8 (continued)

December 31, 2016

Interest expense .................................................... 50,000

Cash (10% x ½ x $1,000,000) ........................................ 50,000

To record interest.

The fair value of the swap increased by $252 (from $9,363 to $9,615).

Similarly, we adjust the note’s book value by the amount necessary to

Illustration A-1

TA-8 (continued)

A-14 Intermediate Accounting, 8/e

At June 30, 2017, Wintel repeats the process of adjusting to fair value both the

derivative investment and the notes being hedged.

June 30, 2017

Interest expense .......................................................... 50,000

Cash (10% x ½ x $1,000,000) ................................ 50,000

To record interest.

Illustration A-1

TA-8 (continued)

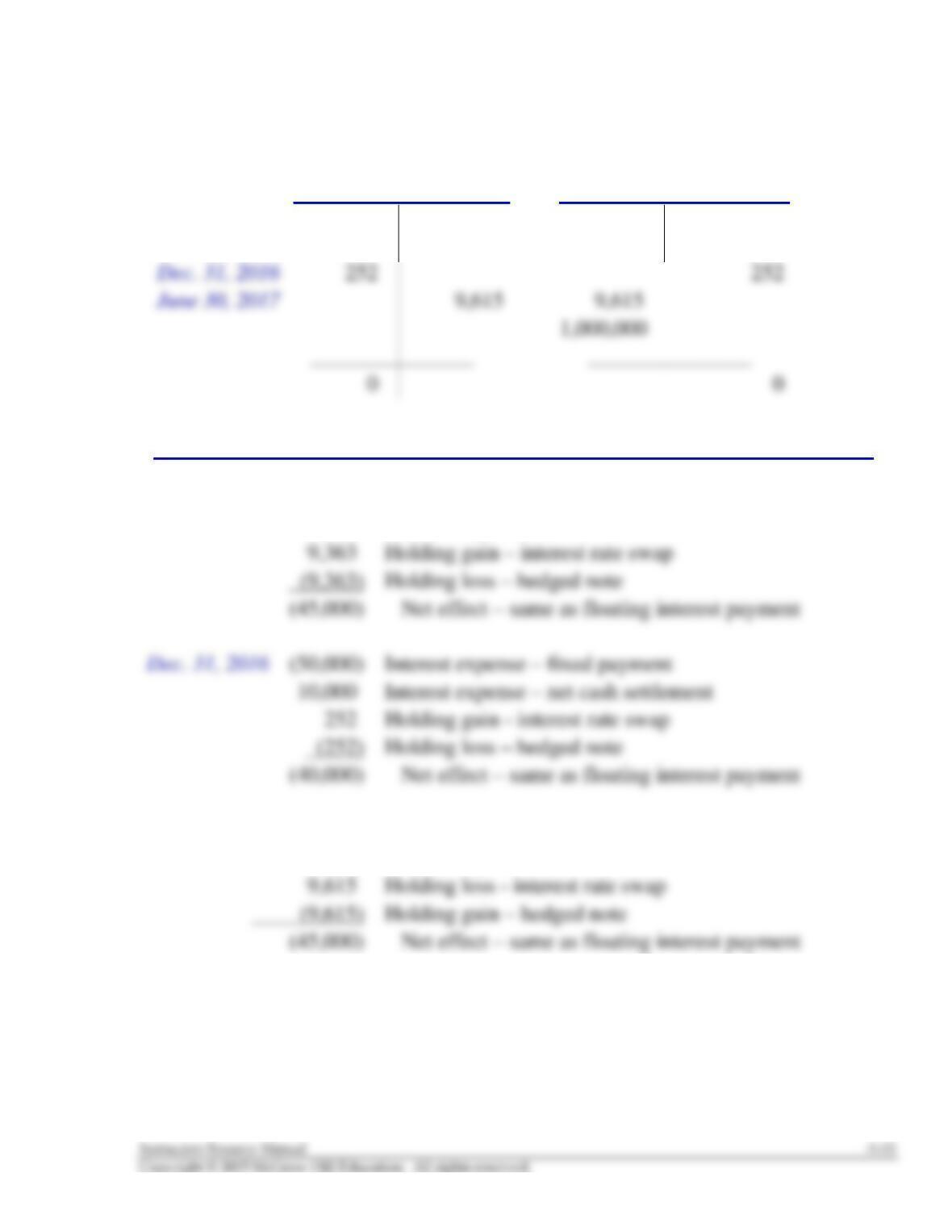

EFFECTS ON BALANCES

Swap Notes

Jan. 1, 2016 1,000,000

June 30, 2016 9,363 9,363

Income Statement + (−)

June 30, 2016 (50,000) Interest expense – fixed payment

5,000 Interest expense – net cash settlement

June 30, 2017 (50,000) Interest expense – fixed payment

5,000 Interest expense – net cash settlement

Illustration A-1

TA-8 (continued)

A-16 Intermediate Accounting, 8/e

HEDGE EFFECTIVENESS

To qualify as a hedge, the hedging relationship must be highly

effective in achieving offsetting changes in fair values or cash

flows.

HEDGE INEFFECTIVENESS

The loss and gain will not exactly offset each other if the

hedging arrangement is ineffective.

FAIR VALUE CHANGES UNRELATED TO RISK BEING HEDGED

Fair value changes unrelated to the risk being hedged are

ignored.

S

Su

ug

gg

ge

es

st

ti

io

on

ns

s

f

fo

or

r

C

Cl

la

as

ss

s

A

Ac

ct

ti

iv

vi

it

ti

ie

es

s

Professional Skills Development Activities

The following are suggested assignments from the end-of-chapter material that will help your

Communication Skills. Communication Cases A-2 requires group interaction. Real World

Cases A-1 and A-3 are suitable for student presentation(s). Questions A-6 and A-7 create good

Research Skills. In their professional lives, our graduates will be required to locate and extract

Analysis Skills. Communication Case A-2 and Real World Case A-3 provide opportunities to

develop analysis skills.

A

As

ss

si

ig

gn

nm

me

en

nt

t

C

Ch

ha

ar

rt

t

Est. time

Questions Topic (min.)

A-1

Derivatives

5

A-2

Hedge accounting

5

Est. time

Exercises Topic (min.)

A-1

Derivatives – hedge classification

15

A-2

Derivatives; interest rate swap; fixed rate debt

15

Est. time

Problems Topic (min.)

A-1

Derivatives - interest rate swap

20

Est. time

Cases Topic (min.)

Research Case A-1

Disclosure of derivative risk; research article in

Accounting Horizons

45