Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

177

CHAPTER 6

RECEIVABLES AND INVENTORIES

CLASS DISCUSSION QUESTIONS

1. Receivables are normally classified as

(1) accounts receivable, (2) notes re-

ceivable, or (3) other receivables.

5. Carter’s should use the direct write-off

method because it is a small business

that has a relatively small number and

volume of accounts receivable.

6. The allowance method

7. Contra asset

$428,200.

9. (1) The percentage rate used is exces-

sive in relationship to the volume of

accounts written off as uncollectible;

hence, the balance in the allowance

account is excessive.

(2) A substantial volume of old uncollectible

accounts is still being carried in the accounts

receivable account.

sitions costs rather than the most recent acquisi-

tions costs.

12. a. FIFO c. FIFO

b. LIFO d. LIFO

13. FIFO

14. LIFO. In periods of rising prices, the use of LIFO

178

EXERCISES

E6–1

Accounts receivable from the U.S. government are significantly different from re-

ceivables from commercial aircraft carriers such as Delta and United. For example,

U.S. government receivables often involve complex contracts, but are backed by

E6–2

Due Date Interest Due at Maturity

a. Feb. 14 $125 [$25,000 × 0.06 × (30/360)]

b. June 30 $135 [$13,500 × 0.04 × (90/360)]

E6–3

a. MGM: 14.6% ($92,571,000 ÷ $633,116,000)

b. IBM: 3.2% ($297,000,000 ÷ $9,225,000,000)

c. Casino operations experience greater bad debt risk since it is difficult to

control the creditworthiness of customers entering the casino. In addition,

individuals who may have adequate creditworthiness could overextend them-

179

E6–4

Collected $5,000

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accounts

Wrote-off $10,000

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Retained

Accounts Receivable = Earnin

g

s

Ma

r

. 18.

(

10,000

)

(

10,000

)

Statement of Cash Flows Income Statement

No effect 0 Mar. 18. Bad debt

expense

(

10,000

)

Reinstated Account

Balance Sheet

Assets = Liabilities + Stockholders’ Equity

Retained

180

E6–4, Concluded

Collected $10,000

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accounts

E6–5

Collected $2,500

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accounts

Cash + Receivable

Jul

y

3. 2,500

(

2,500

)

Statement of Cash Flows Income Statement

Jul

y

3. Operatin

g

2,500 No effect 0

Wrote-off $11,000

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accounts Allowance fo

r

181

E6–5, Concluded

Reinstated Account

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accounts Allowance for

Collected $11,000

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accounts

Cash + Receivable

Oct. 8. 11,000

(

11,000

)

Statement of Cash Flows Income Statement

Oct. 8. Operatin

g

11,000 No effect 0

182

E6–6

a.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accounts Retained

b.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accts. Allowance for

Rec.

–

Doubtful Accounts

(

13,000

)

13,000

Statement of Cash Flows Income Statement

No effect 0 No effect 0

E6–7

Estimated balance of Allowance for Doubtful Accounts: $48,700

Computed as shown below.

Estimated

Uncollectible Accounts

Age Interval Balance Percent Amount

Not past due ............................................... $ 925,000 1% $ 9,250

1–30 days past due .................................... 375,000 2 7,500

183

E6–8

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Allowance for Retained

E6–9

a. $172,500 ($34,500,000 × 0.005) c. $258,750 ($34,500,000 × 0.0075)

b. $181,500 ($200,000 – $18,500) d. $264,000 ($255,000 + $9,000)

E6–10

$108,200 [$120,000 + $16,000 – ($2,780,000 × 1%)]

184

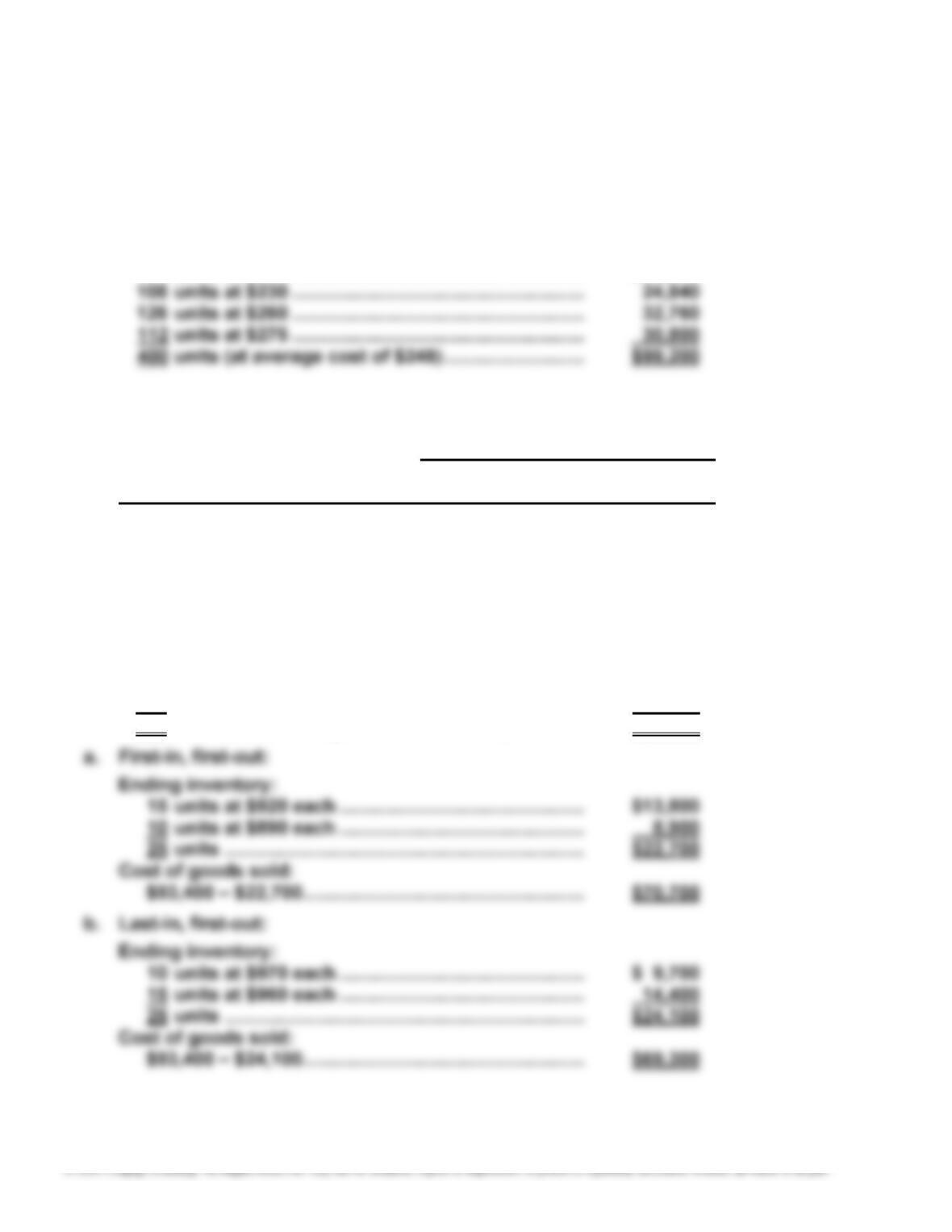

E6–12

a. $24,750 (90 units at $275)

b. $19,080 [(54 units × $200) + (36 units × $230) = $10,800 + $8,280]

c. $22,320 (90 units at $248; $99,200 ÷ 400 units = $248)

Cost of merchandise available for sale:

54 units at $200 ........................................................ $10,800

E6–13

Cost

Ending Cost of Goods

Inventory Method Inventory Sold

a. FIFO ........................................ $22,700 $70,700

b. LIFO ........................................ 24,100 69,300

c. Weighted average ................. 23,350 70,050

Cost of merchandise available for sale:

10 units at $970 each ............................................... $ 9,700

45 units at $960 each ............................................... 43,200

30 units at $890 each ............................................... 26,700

15 units at $920 each ............................................... 13,800

100 units (at an average unit cost of $934) .............. $93,400

185

E6–13, Concluded

c. Weighted average cost:

E6–14

1. a. FIFO ending inventory > (greater than) LIFO ending inventory

b. FIFO cost of goods sold < (less than) LIFO cost of goods sold

2. In periods of rising prices, the net income shown on the company’s tax return

would be lower under LIFO than under FIFO; thus, there is a tax advantage of

using LIFO.

Note to Instructors: The federal tax laws require that if LIFO is used for tax pur-

poses, LIFO also must be used for financial reporting purposes. This is known

E6–15

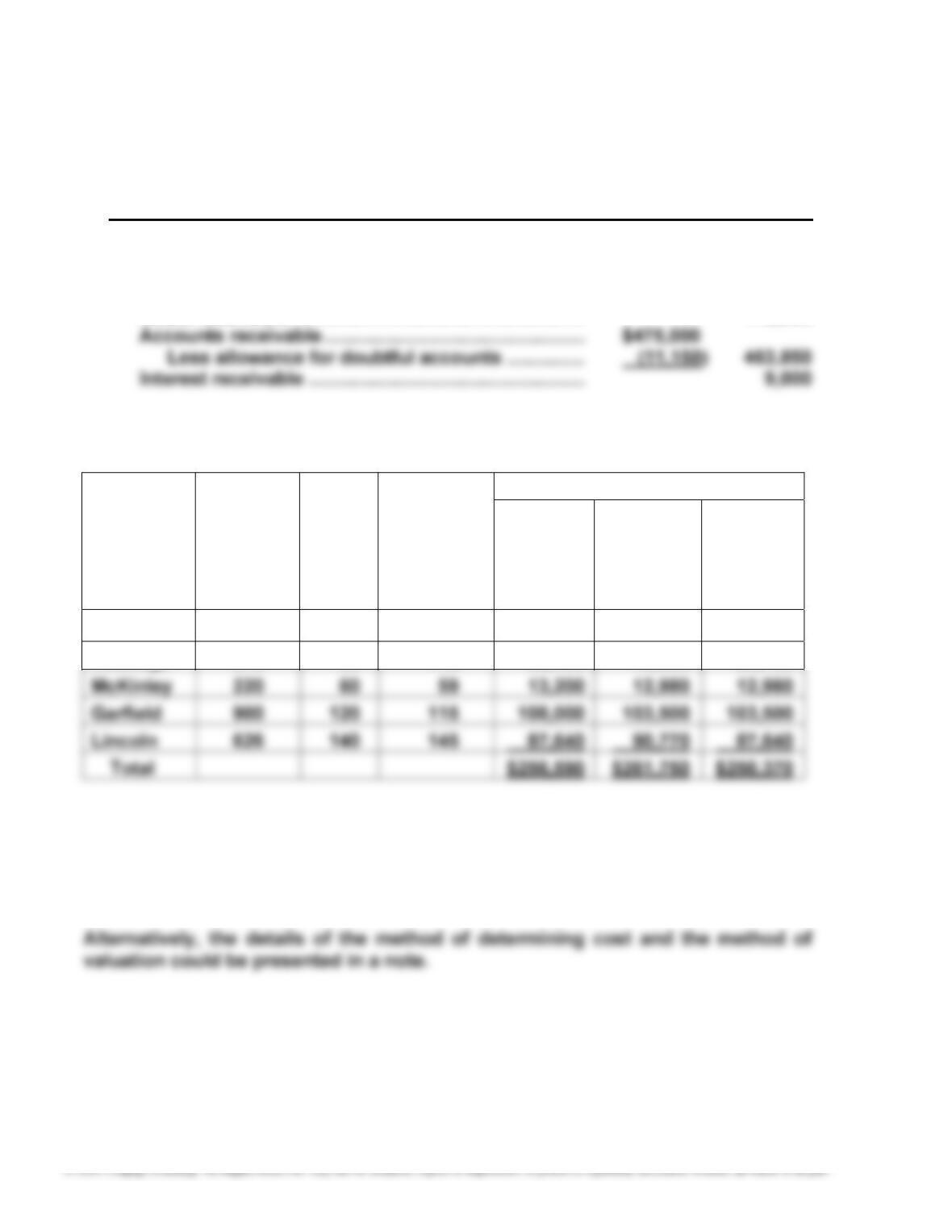

1. a. The interest receivable should be reported separately as a current asset.

It should not be deducted from notes receivable.

186

E6–15, Concluded

ZABEL COMPANY

Balance Sheet

December 31, 20Y4

Assets

Current assets:

Cash ............................................................................ $ 75,000

Notes receivable ........................................................ 115,000

E6–16

Product

Inventory

Quantit

y

Cost

per

Unit

Market

Value per

Unit (Net

Realizable

V

alue

)

Total

Cost Market LCM

Adams 100 $140 $125 $ 14,000 $ 12,500 $ 12,500

Coolid

g

e 375 90 112 33,750 42,000 33,750

E6–17

The inventory would appear in the Current Assets section, as follows:

Inventory—at lower of cost (FIFO) or market ............................... $250,370

187

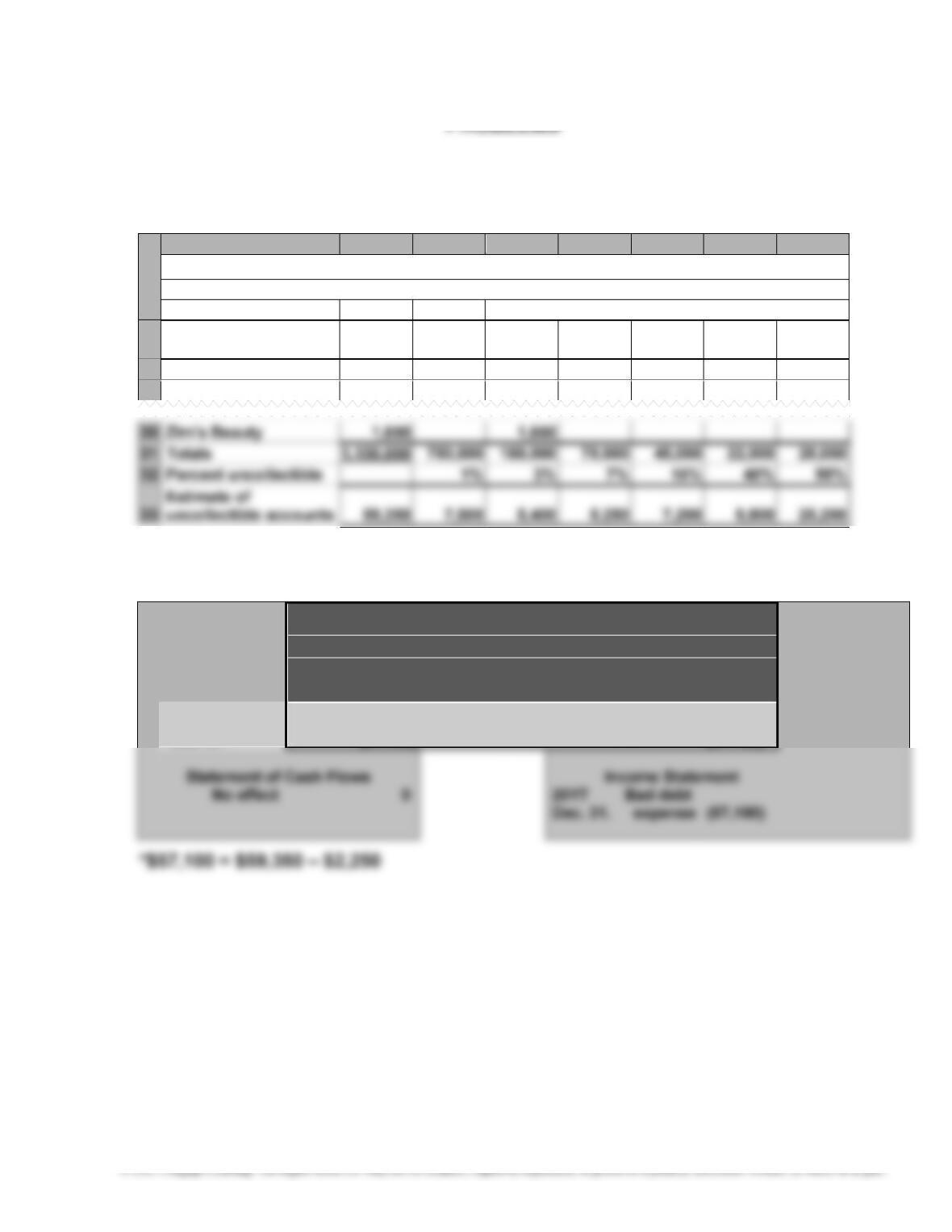

P6–1

1.

A

B C D E F G H

1 Aging-of-Receivables Schedule

2 December 31, 20

Y

7

3 Da

y

s Past Due

4 Custome

r

Balance

Not Past

Due 1

–

30 31

–

60 61

–

90 91

–

120

Over

120

5 AAA Beaut

y

27,500 27,500

6 Amelia’s Wigs 3,750 3,750

2.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Allowance for Retained

–

Doubtful Accounts = Earnin

g

s

20Y7

188

P6–1, Continued

3.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Allowance for Retained

4.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accounts Allowance fo

r

Receivable

–

Doubtful Accounts

20Y8

Mar. 4.

(

2,950

)

2,950

Statement of Cash Flows Income Statement

No effect 0 No effect 0

189

P6–1, Continued

5.

Reinstated Account

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accounts Allowance for

Receivable

–

Doubtful Accounts

20Y8

Au

g

. 17. 2,950

(

2,950

)

Statement of Cash Flows Income Statement

No effect 0 No effect 0

Collected $2,950

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accounts

6. a.

Write-off of Account

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Retained

190

P6–1, Concluded

6. b.

Reinstated Account

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Retained

Accounts Receivable = Earnin

g

s

20Y8

Au

g

. 17. 2,950

2,950

Statement of Cash Flows Income Statement

No effect 0 20Y8

Au

g

. 17.

Bad debt

expense

2,950

Collected $2,950

Balance Sheet

Assets = Liabilities + Stockholders’ Equity

Accounts