Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

103

CHAPTER 4

ACCOUNTING FOR RETAIL OPERATIONS

CLASS DISCUSSION QUESTIONS

1. Retail businesses acquire merchandise for

resale to customers. It is the selling of mer-

chandise, instead of a service, that makes

the activities of a retail business different

from the activities of a service business.

2. Under the periodic method, the inventory

3. a. A 2% discount is allowed if paid within

10 days of date of invoice; otherwise,

the entire amount of the invoice is due

within 30 days of date of invoice.

b. Payment is due within 90 days of date of

invoice.

c. Payment is due by the end of the month

6. Since the buyer is paying for the destination

charge, the car is being purchased FOB

shipping point.

7. Sales to customers who use credit cards are

generally treated as cash sales. The credit

card invoices representing these sales are

9. The major advantages of the single-step

form of the income statement are its simplicity

and its emphasis on total revenues and total

expenses as the determinants of net income.

The major objection to the form is that such

relationships as gross profit to sales and

operating income to sales are not as readily

determinable as when the multiple-step form

104

EXERCISES

E4–1

a. $512,000 ($3,200,000 – $2,688,000)

b. 16% ($512,000 ÷ $3,200,000)

E4–2

$51,125 million ($71,879 million – $20,754 million)

E4–3

a. $7,350 {Purchase of $8,820 [$9,000 – ($9,000 × 2%)] less return of $1,470

E4–4

Offer B is lower than offer A. Details are as follows:

A B

List price ..................................................................... $78,000 $80,000

Less discount ............................................................. (780) (1,600)

105

E4–5

a.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accts.

Inventor

y

= Pa

y

able

b.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accts.

Inventor

y

= Pa

y

able

(

15,680

)

*

(

15,680

)

Statement of Cash Flows Income Statement

No effect 0 No effect 0

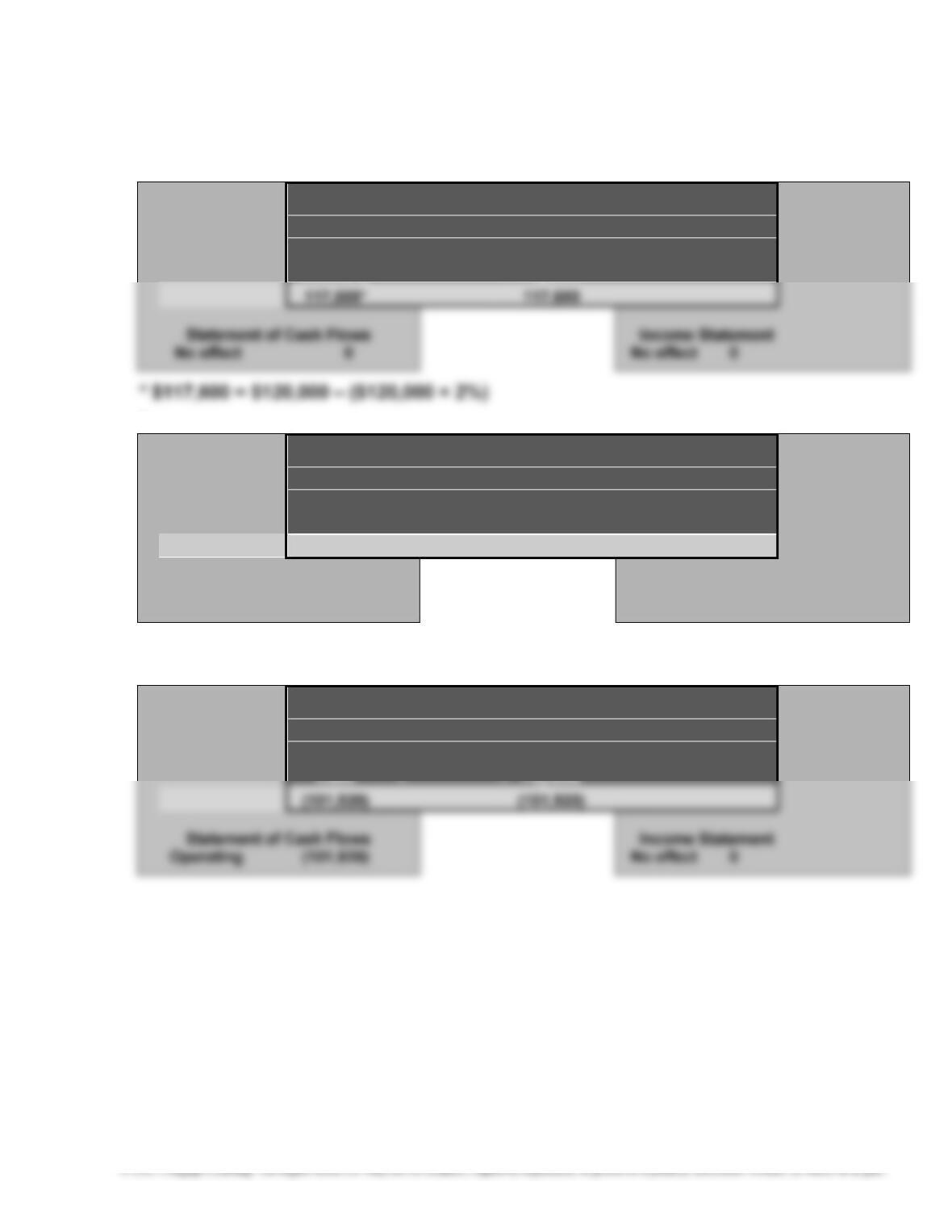

* $15,680 = $16,000 – ($16,000 × 2%)]

c.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accts.

106

E4–6

a.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accts.

b.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accts.

Cash + = Payable

(

198,000

)

(

198,000

)

Statement of Cash Flows Income Statement

Operating (198,000) No effect 0

c.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accts.

d.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accts.

Inventor

y

= Pa

y

able

17,325* 17,325

Statement of Cash Flows Income Statement

No effect 0 No effect 0

* $17,325 = $17,500 – ($17,500 × 1%)

107

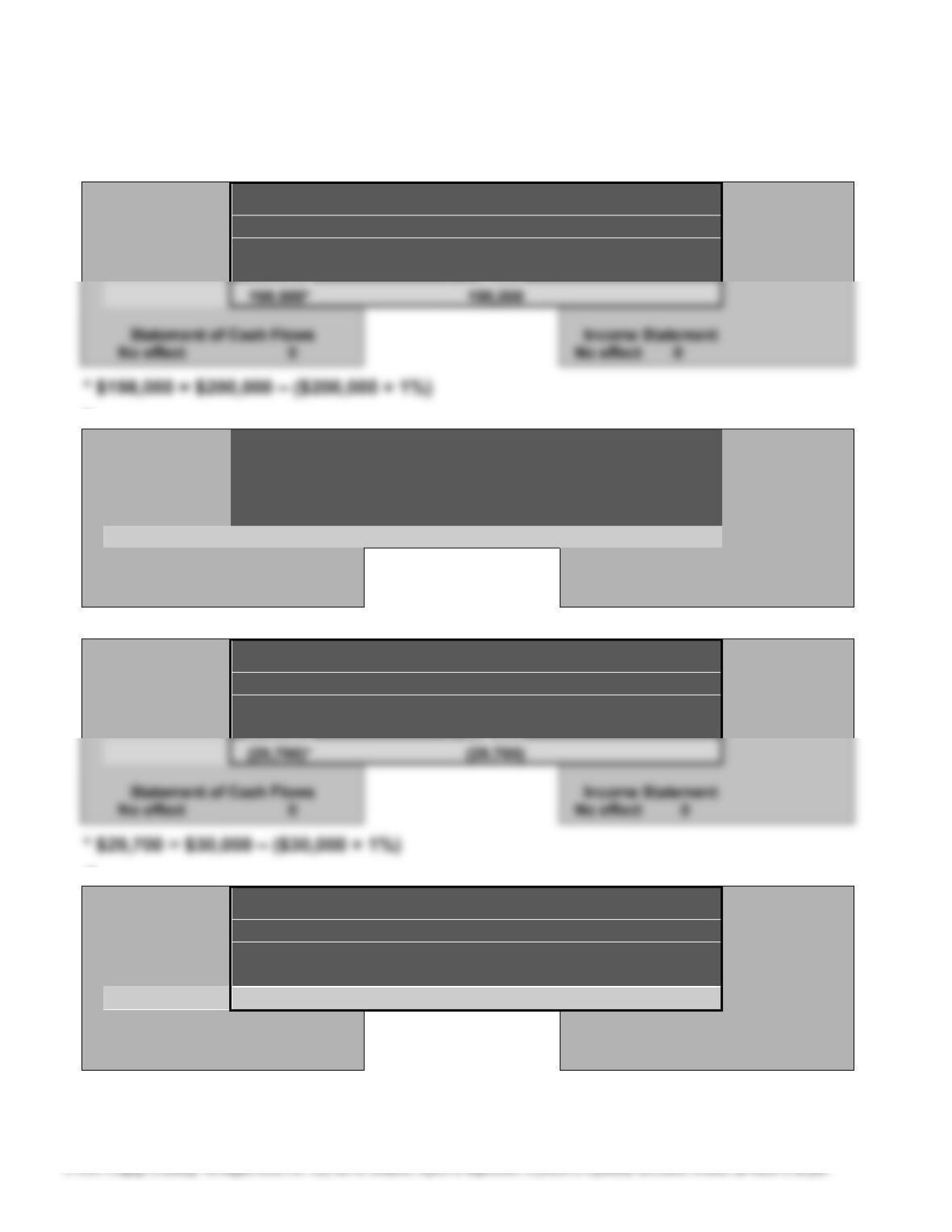

E4–6, Continued

e.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accts.

Cash = Pa

y

able

c.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accts.

Rec. + Inventor

y

29,700*

(

29,700

)

Statement of Cash Flows Income Statement

No effect 0 No effect 0

* $29,700 = $30,000 – ($30,000 × 1%)

d.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accts.

108

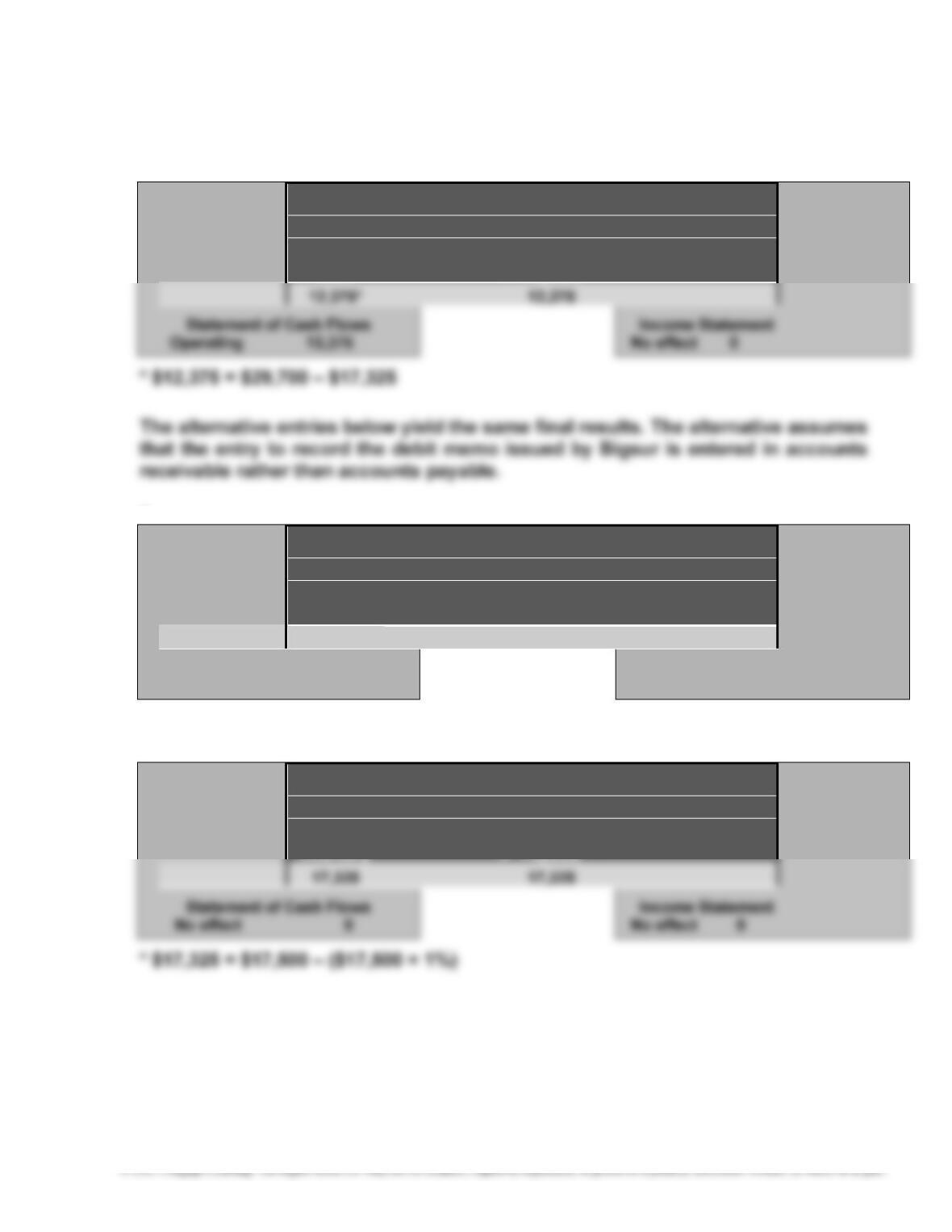

E4–6, Concluded

e.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accts. Accts.

Cash + Rec. = Pa

y

able

12,375

(

29,700

)

(

17,325

)

Statement of Cash Flows Income Statement

Operating 12,375 No effect 0

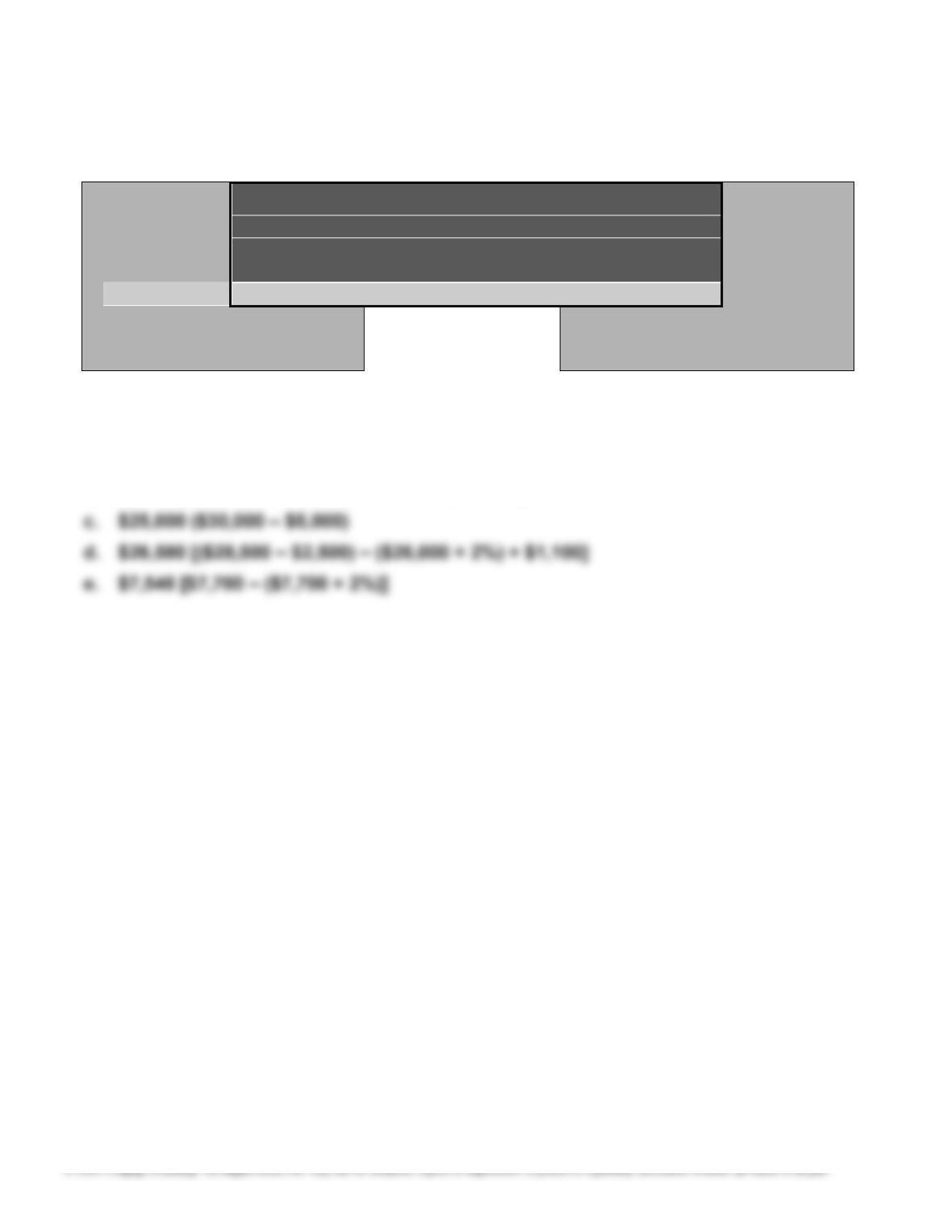

E4–7

a. $11,682 [($12,800 – $1,000) – ($11,800 × 1%)]

b. $5,565 [($6,000 – $500) – ($5,500 × 2%) + $175]

109

E4–8

a.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Retained

b.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accts. Retained

Rec. + Inventor

y

= Earnin

g

s

27,800

(

16,000

)

11,800

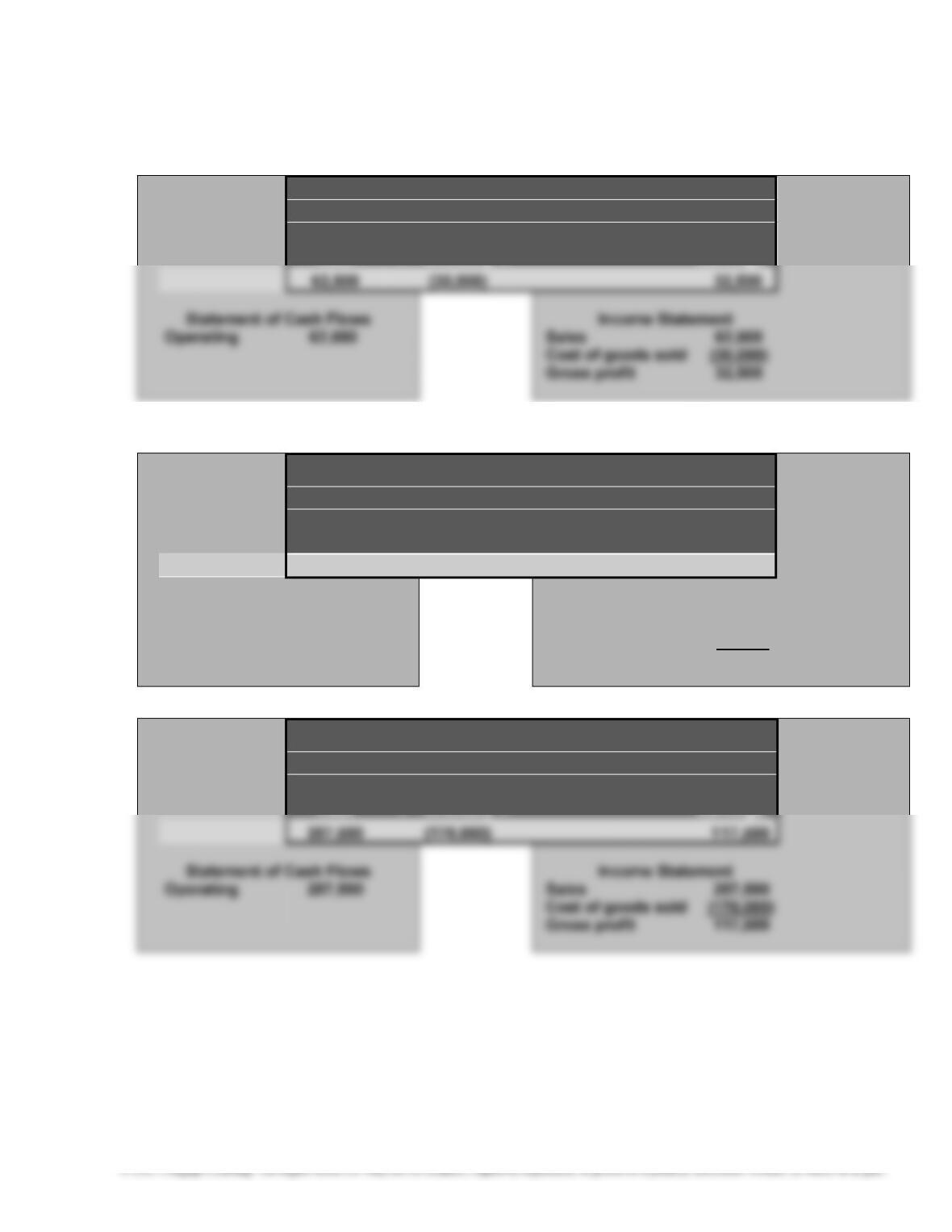

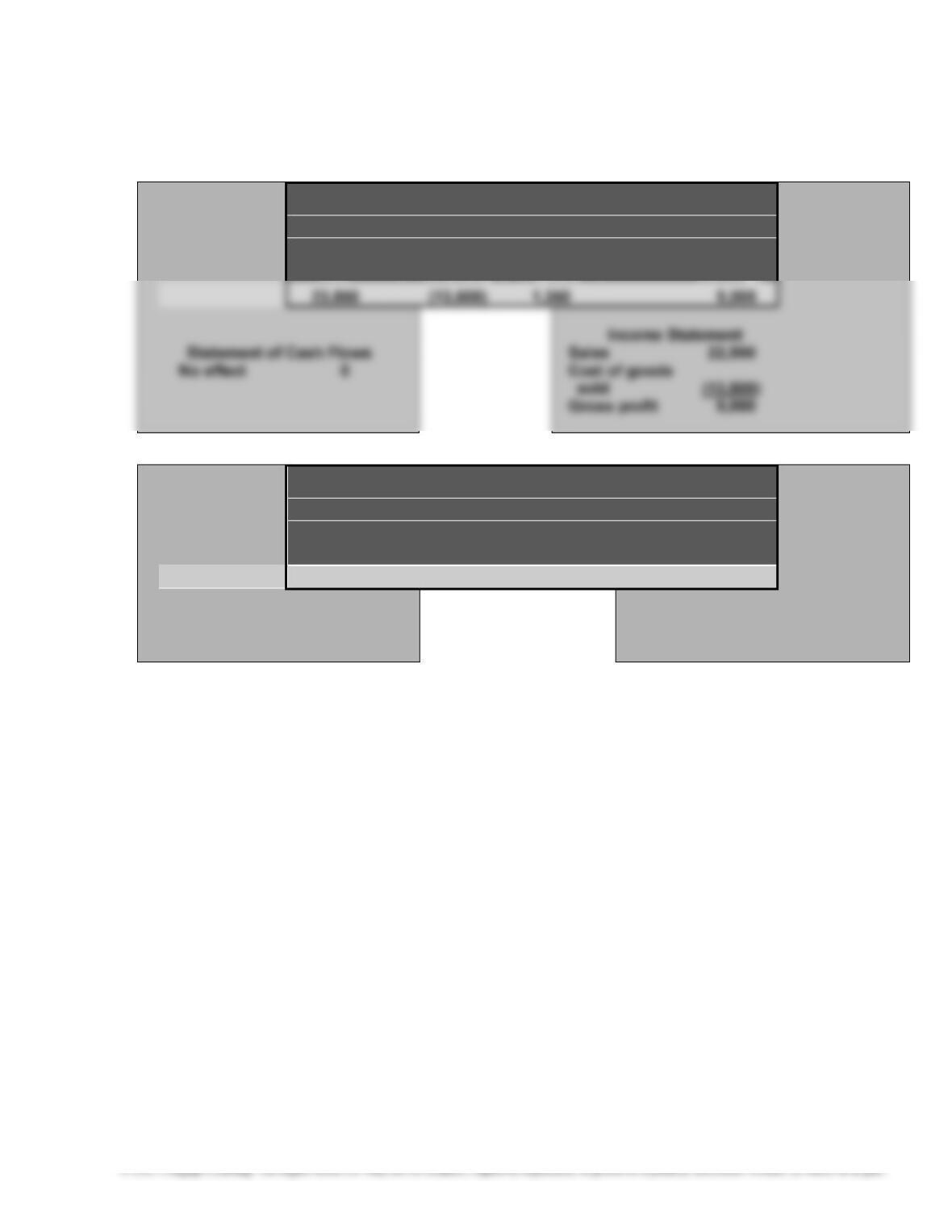

Statement of Cash Flows Income Statement

No effect 0 Sales 27,800

Cost of

g

oods sold

(

16,000

)

Gross profit 11,800

c.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Retained

110

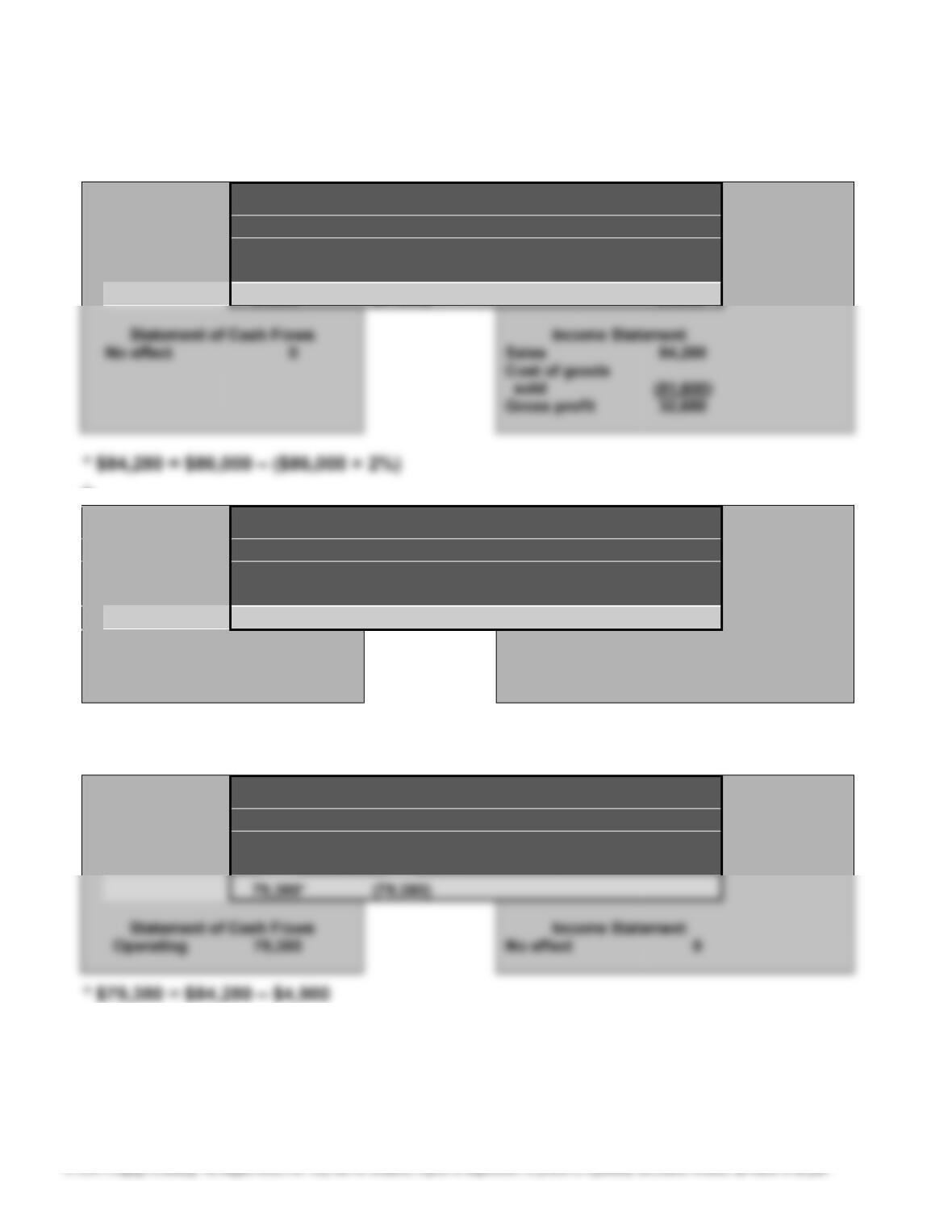

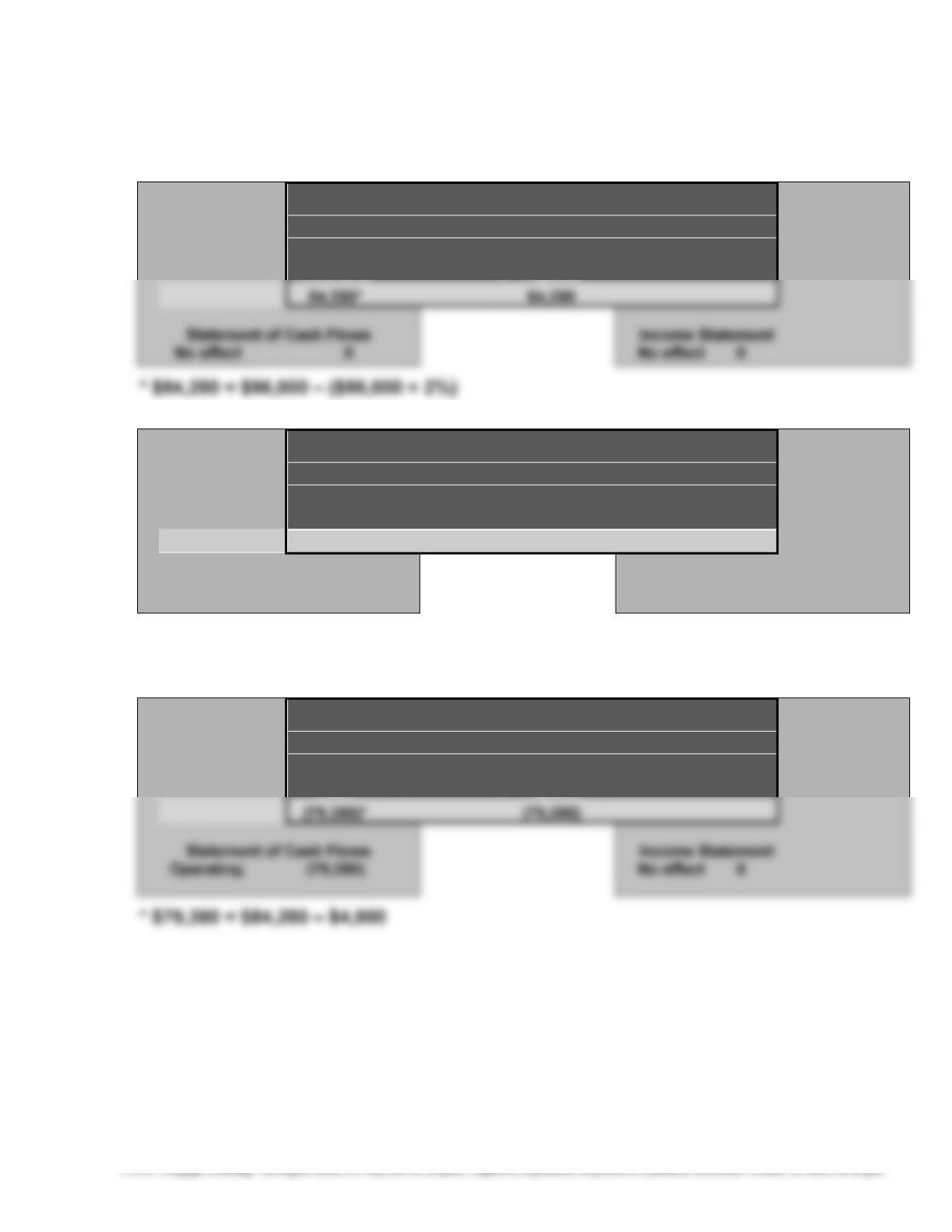

E4–9

a. $15,680 [$16,000 – ($16,000 × 2%)]

b.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Est. Ret. Customer

E4–10

a. $7,920 [$8,000 – ($8,000 × 1%)]

b. $8,220 ($7,920 + $300)

E4–11

a. At the time of sale

b. $5,000

111

E4–12

a.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accts. Sales Tax Retained

b.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Sales Tax

Cash = Pa

y

able

(

1,350

)

(

1,350

)

Statement of Cash Flows Income Statement

Operatin

g

(

1,350

)

No effect 0

112

E4–13

a.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accts. Retained

Rec. + Inventor

y

= Earnin

g

s

b.

Balance Sheet

Assets = Liabilities + Stockholders’ Equity

Accts. Cust. Refunds

Rec. = Payable

(4,900)* (4,900)

Statement of Cash Flows Income Statement

No effect 0 No effect 0

* $4,900 = $5,000 – ($5,000 × 2%)

c.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accts.

113

E4–14

a.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accts.

b.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accts.

Inventor

y

= Pa

y

able

(

4,900

)

*

(

4,900

)

Statement of Cash Flows Income Statement

No effect 0 No effect 0

* $4,900 = $5,000 – ($5,000 × 2%)

c.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accts.

114

E4–15

Balance Sheet

Assets = Liabilities + Stockholders’ Equity

Retained

Inventory = Earnings

E4–16

Balance Sheet

Assets = Liabilities + Stockholders’ Equity

Estimated Returns Custome

r

Retained

Inventory = Refunds Payable Earnings

July 31. 6,000 13,500* (7,500)

115

E4–17

a. Selling expense, (1), (2), (7), (8)

E4–18

a.

VIBE TRIBE INC.

Income Statement

For the Year Ended March 31, 20Y5

Sales ............................................................... $ 8,925,000

Cost of goods sold ......................................... (5,175,000)

Gross profit ..................................................... $ 3,750,000

Operating expenses:

Selling expenses ....................................... $825,000

Administrative expenses .......................... 475,000

116

E4–19

LOMA COMPANY

Income Statement

For the Year Ended April 30, 20Y6

Revenues:

Sales ............................................................................ $ 13,580,000

Rent revenue ............................................................... 120,000

Total revenues......................................................... $ 13,700,000

Expenses:

117

E4–20

a. 1. Deducting cost of goods sold from sales yields $1,570,000 not $1,930,000.

2. Deducting the cost of goods sold from sales yields gross profit and not

operating income.

b. A correct income statement would be as follows:

CARLSBAD COMPANY

Income Statement

For the Year Ended February 28, 20Y8

Sales ................................................................ $ 4,220,000

Cost of goods sold ......................................... (2,650,000)

Gross profit ..................................................... $ 1,570,000

Expenses:

118

E4–21 (Appendix 1)

a.

Balance Sheet

Assets = Liabilities + Stockholders’ Equity

Accounts Retained

Receivable + Inventory = Earnings

b.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accounts Retained

Cash + Receivable = Earnin

g

s

9,800

(

10,000

)

(

200

)

Statement of Cash Flows Income Statement

Operatin

g

9,800 Sales

(

200

)

c.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accounts Retained

119

E4–22 (Appendix 1)

Balance Sheet

Assets = Liabilities + Stockholders’ Equity

Accounts Retained

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accounts Retained

Receivable + Inventor

y

= Earnin

g

s

Mar. 8. 24,000

(

14,400

)

9,600

Statement of Cash Flows Income Statement

No effect 0 Mar. 8. Sales 24,000

Cost of

g

oods sold

(

14,400

)

Gross profit 9,600

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accounts Retained

Cash + Receivable = Earnin

g

s

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accounts Retained

Cash + Receivable = Earnin

g

s

Mar. 20. 23,520

(

24,000

)

(

480

)

Statement of Cash Flows Income Statement

Mar. 20. Operatin

g

23,520 Mar. 11. Sales

(

480

)

E4–23 (Appendix 1)

a.

Balance Sheet

Assets = Liabilities + Stockholders’ Equity

Accounts Allowance fo

r

Retained

b. Sales would be reported as $9,993,000 ($10,000,000 − $7,000) on the income

statement. Accounts receivable would be reported as a current asset on the

balance sheet as follows:

Accounts receivable $850,000

Allowance for sales discounts (7,400)

Net accounts receivable $842,600

E4–24 (Appendix 1)

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accounts Allowance for

121

PROBLEMS

P4–1

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accts.

Inventor

y

= Pa

y

able

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Accts.

Inventor

y

= Pa

y

able

Au

g

. 9.

(

1,225

)

*

(

1,225

)

Statement of Cash Flows Income Statement

No effect 0 No effect 0

*$1,225 = $1,250 – ($1,250 × 2%)

Balance Sheet

Assets = Liabilities + Stockholders’ Equity

Accts.

122

P4–1, Concluded

Balance Sheet

Assets = Liabilities + Stockholders’ Equity

Accts.

Cash = Payable

Balance Sheet

Assets = Liabilities + Stockholders’ Equity

Accts.

Cash = Payable

Aug. 31. (12,500) (12,500)

Statement of Cash Flows Income Statement

Au

g

. 31. Operatin

g

(

12,500

)

No effect 0