Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 16

Question 1

This is not an appropriate approach, as DiversCo should be valued using a sum-of-the-parts methodology. One should create a comparable group of firms

operating in the retail apparel sector and another comparable group operating in the energy sector. Multiples should then be constructed for each peer group

and applied to the appropriate division profits for DiversCo.

Chapter 16

Question 2

A forward-looking multiple is a multiple that uses projected earnings or revenues in the denominator. Forward-looking multiples are preferable to backward-looking

multiples for three reasons. First, the latter may include extraordinary items. Second, the former aligns better with the numerator in that they both are based on future values.

Finally, there is less variance in peer-group multiples for forward-looking than for backward-looking multiples.

Chapter 16

Questions 3 and 4

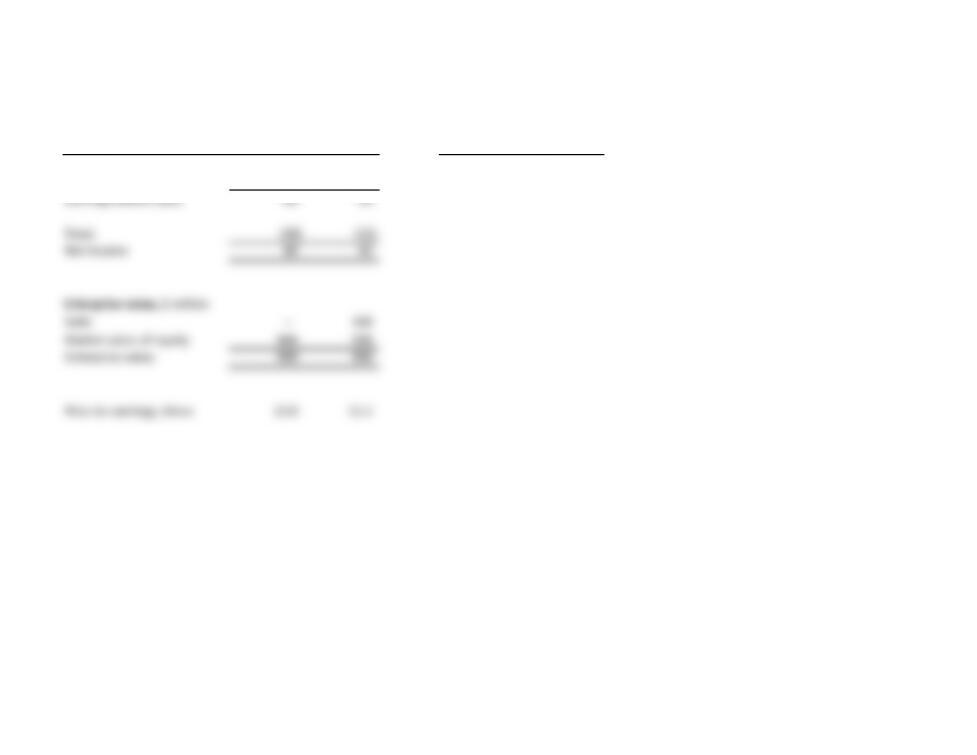

$ million Company 1 Company 2 Company 3

Share price, $ 25 16 30

Shares outstanding, millions 5 8 15

Equity value 125 128 450

Short-term debt 25 15 30

Long-term debt 50 70 40

Total debt 75 85 70

Gross enterprise value 200 213 520

Nonconsolidated subsidiaries – – (50)

Core operating value1200 213 470

EBITDA will be lower for Company 1 if the company outsources

Operating income production. This causes its enterprise-value-to-EBITDA

EBITDA 25 30 59 multiple to be higher than the EV-to-EBITDA multiples of

EBITA 22 23 51 competitors that produce internally.

Multiples, times

Enterprise value to EBITDA 8.0 7.1 8.0 Ignoring the impact of nonconsolidated subsidiaries in the numerator

Enterprise value to EBITA 9.1 9.3 9.2 would overstate both ratios, with the EV/EBITDA being 8.8 and the

EV/EBITA being 10.2. We want to exclude these nonoperating assets

1Also known as net enterprise value. because EBITDA and EBITA are both focused on profits from operations.

Chapter 16

Questions 5 and 6

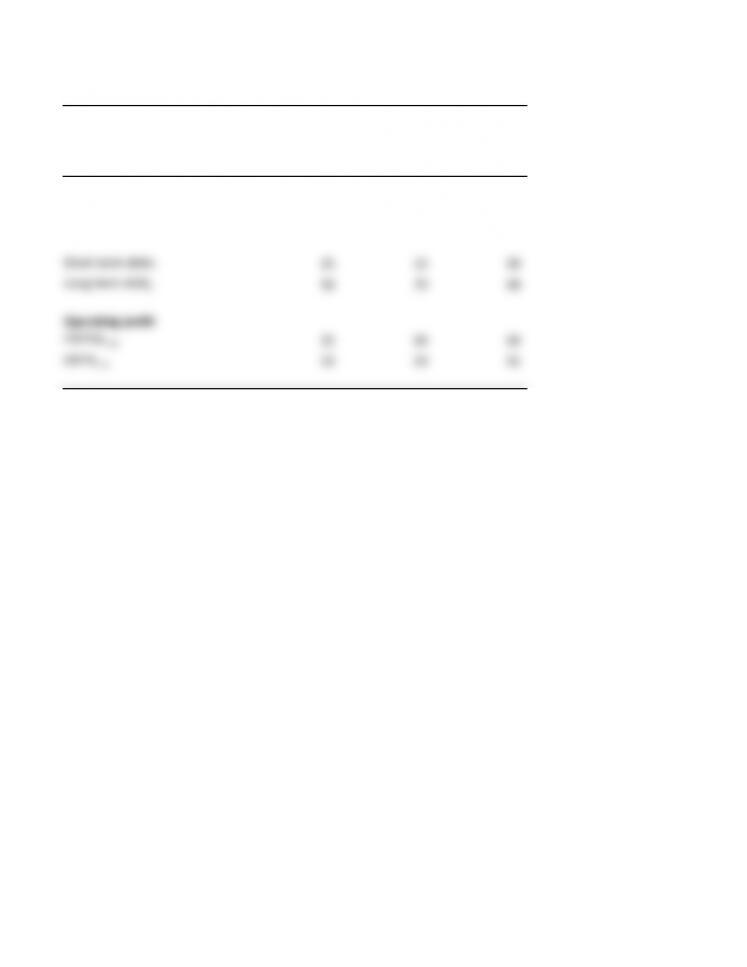

Driver, $ million Company A Company B Company C Other input

Operating profit 160 160 160 Tax rate, % 25%

Operating taxes 40 40 40

NOPLAT 120 120 120

Growth, % 2% 6% 5%

ROIC, % 15% 10% 12%

WACC, % 10% 10% 10%

Value 1,300 1,200 1,400

EV-to-EBITA multiple, times 8.1 7.5 8.8

Question 5: Company A versus Company B

Company B has an ROIC equal to its cost of capital, so growth fails to create value. Consequently, no premium

is paid for growth, and the company trades at a lower multiple.

Question 6: Company A versus Company C

Both Company A and Company C have ROIC above their cost of capital, so growth leads to higher value. Company C

also has a lower ROIC, but this is more than offset by the higher growth rate.

Chapter 16

Question 7

If future cash flows (and the cost of capital) are the same for two companies, their valuations will be the same. If one

company has lower short-term earnings, as RedBev does, then its enterprise value to EBITA will be higher, since value

remains the same but earnings drop. This can make multiples analysis confusing. A higher multiple doesn't always

mean better long-term prospects. It could just represent a short-term depression in earnings.

Chapter 16

Question 8

All

Income statement, $ million equity Levered Other inputs, %

Operating profit 80 80 Interest rate 5%

Interest expense – (20) Tax rate 25%

Earnings before taxes 80 60

Taxes (20) (15)

Net income 60 45

Enterprise value, $ million

Debt – 400

Market value of equity 900 500

Enterprise value 900 900

Price to earnings, times 15.0 11.1

It is difficult to tell a priori whether a P/E will go up or down with increasing leverage. The calculations here show a decrease in P/E with leverage.

However, this is not always the case. In general, for low- (high-) multiple firms, using debt lowers (raises) the P/E. However, the cost of debt

is also a factor. A takeaway then is that it may be hard to distinguish why one firm has a higher P/E than another firm.

Is it due to operating performance or leverage?

Chapter 16

Question 9

Enterprise-value-to-revenues multiples may mask differences in cost structures between firms. If Firm Y and Firm Z have the same

enterprise-value-to-revenues multiple and the same amount of invested capital, but Firm Z has better operating-profit margins

going forward, then Firm Z should be worth more. This would not show up in the enterprise-value-to-revenues multiple.

Enterprise-value-to-revenues multiples are useful when profits are negative and/or when a firm's current operating profits are

different from long-term expected profits.

Exhibit 16.12 Multiples Analysis: Market and Profit Data

$ million

Company 1 Company 2 Company 3

Market data

Share pricet, $ 25 16 30

Shares outstandingt, millions 5 8 15

Short-term debtt25 15 30

Long-term debtt50 70 40

Operating profit

EBITDAt+1 25 30 59

EBITAt+1 22 23 51