Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 12 - Strategy and the Analysis of Capital Investments

CHAPTER 12: STRATEGY AND THE ANALYSIS OF CAPITAL

INVESTMENTS

QUESTIONS

12-1 Capital-budgeting decisions: (a) are long-term in nature (i.e., they affect profitability

and cash flows for many years into the future), and (b) involve substantial amounts

discounted after-tax flows are needed for investment-analysis purposes.

12-2 As members of managerial decision-making teams, accountants can add value to

the capital budgeting process in at least four ways: (1) ensuring linkage between the

capital budgeting process and the organization’s master budget; (2) ensuring linkage

to the strategic plans of the organization (e.g., integrating capital budgeting into an

12-3 The analytic hierarchy process (AHP) is one of several multi-criteria decision-making

techniques, that is, decision models that include more than a single decision

criterion. As such, the model can incorporate both financial and nonfinancial

(strategic) decision criteria, weighted according to managerial preferences.

to numerous decision contexts.

12-4 Income-tax effects represent changes (i.e., increases or decreases) to the income-

tax liability of the firm. Tax effects of a decision to acquire new factory equipment

may include:

Decreases in income taxes because of the deductibility of depreciation

expenses of the factory equipment.

Increases in tax payments for taxable gains (or decreases in tax payments for

12-5 Among the limitations of the payback period decision model are its failure to

12-1

Education.

Chapter 12 - Strategy and the Analysis of Capital Investments

consider a project’s total profitability over its useful life and failure to incorporate the

time value of money. The present value payback period model considers the time

12-6 The book (accounting) rate of return of an investment is not likely to yield a true

measure of the rate of return on the investment because it does not consider the

time value of money and because it includes in its computation accrual-based

accounting numbers (rather than after-tax cash flows). In contrast, the internal rate

of return (IRR) of a project, because it focuses on discounted cash flows, represents

an estimate of the true (i.e., economic) rate of return on a proposed investment. For

12-7 The decision criterion for the NPV method is the amount and direction of the net

present value. A proposed investment with a positive NPV should be accepted.

Furthermore, a higher NPV signals a better capital investment, from the standpoint

of the goal of maximizing shareholder value.

The IRR method uses a different decision criterion for evaluating capital

12-8 Among important behavioral factors that might affect capital investment decisions

are:

Desires of managers to grow through acquisitions and new investments

12-9 The NPV method weighs early cash flows more heavily than cash flows in the

12-2

Education.

Chapter 12 - Strategy and the Analysis of Capital Investments

distant future in at least two ways. First, amounts of discount applied to early cash

flows are less than those of later cash flows. Thus, one dollar to be received in the

12-10 Depreciation expense per se has no effect on cash flows. However, depreciation

deductions do affect capital investment decisions in two indirect ways:

economic life, which in turn affects the tax liability of the firm in the year of

asset disposal.

12-11 a. The firm can expect to earn a higher return than the cost of funds needed for the

investment; thus, using the IRR decision model, this project should be accepted. It

promises to fully recover the initial investment in the project plus provide an

firm a present-value return of $148,000 above the required 10% rate of return.

12-12 The internal rate of return (IRR) of a project assumes that the cash inflows from the

project are reinvested at the project’s IRR. The modified internal rate of return

(MIRR) assumes, by contrast, that these cash flows are reinvested at the firm’s

discount rate (i.e., its WACC). Some individuals believe that MIRR more accurately

reflects the profitability of a project.

For example, assume a two-year project with an initial outlay of $195, a cost of

capital of 12%, a return of $121 in the first year and a return of $131 in the second

12-3

Chapter 12 - Strategy and the Analysis of Capital Investments

NPV = 17.47 when MIRR = 12%

The following function in Excel can be used to estimate a project’s MIRR:

MIRR(values,finance_rate,reinvest_rate)

where values is an array or a reference to cells that contain numbers. These

numbers represent a series of payments (negative values) and cash inflows (positive

12-13 (Appendix B): With unlimited funds available at a 10 percent cost of capital, the firm

needs to ensure that all investments will earn an economic return of at least 10

percent. As explained in the appendix, if the firm operates under a capital constraint,

12-14 (Appendix B): The NPV model and the IRR model may yield conflicting results when

two investment projects are being compared and these projects differ in:

12-15 (Appendix B): Because of the scaling process, the size of initial investment has no

effect on the rate of return as determined using the IRR model. However, a project

with a larger initial investment will likely have a higher NPV than a project with a

smaller initial investment (simply because it is bigger) and often becomes the

preferred investment when using a NPV method to analyzing capital investments. An

12-4

Education.

Chapter 12 - Strategy and the Analysis of Capital Investments

BRIEF EXERCISES

12-16 Calculating After-tax Cash Flows

Given a marginal income-tax rate of 34%:

a) The after-tax cash effect of a $1,000 increase in cash contribution margin =

= $500 × (1 – 0.34) = $330.00 decrease

12-17 SL Depreciation Calculation Using Excel

12-18 Calculating Net After-tax Cash Flows:

Indirect Method:

Pre-tax Income ($260 – $140 – $50) = $70.00

Less: Income-tax Expense = 24.50

Direct Method:

After-tax cash operating income

($260 – $140) × (1 – 0.35) = $78.00

Plus: Depreciation tax shield

12-5

Education.

Chapter 12 - Strategy and the Analysis of Capital Investments

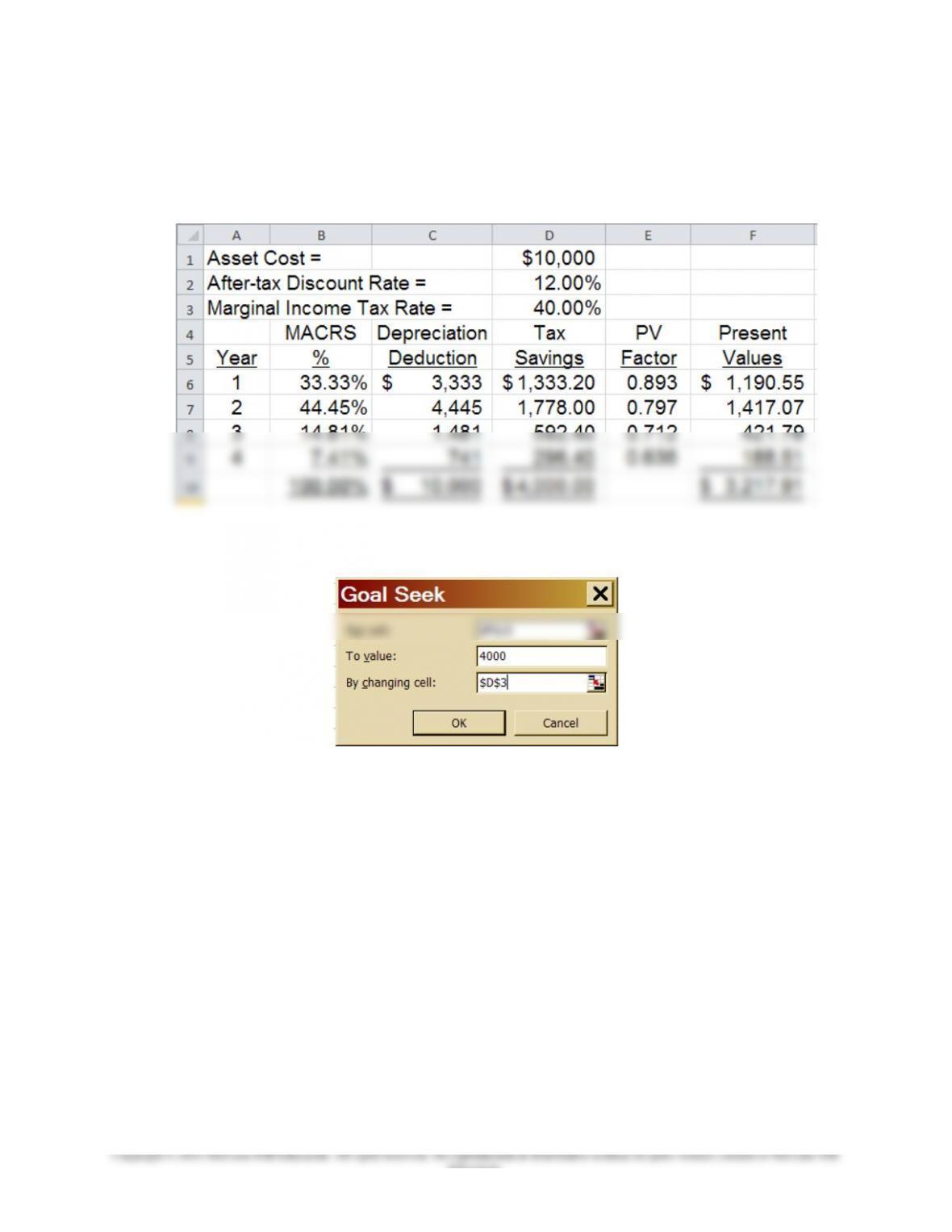

12-19 MACRS Depreciation Calculations

3-year property, cost = $10,000:

Year 1 = $10,000 × 33.33% = $3,333

12-20 Present Value of MACRS Depreciation Deductions

Net present value of depreciation tax deductions, given an after-tax discount rate of

12.00%, MACRS 3-year property, and an asset-acquisition cost of $10,000 = $3,217,

as follows (note: the PV factors are taken from Table1, Appendix C; Present Value

amounts are rounded):

(rounded)

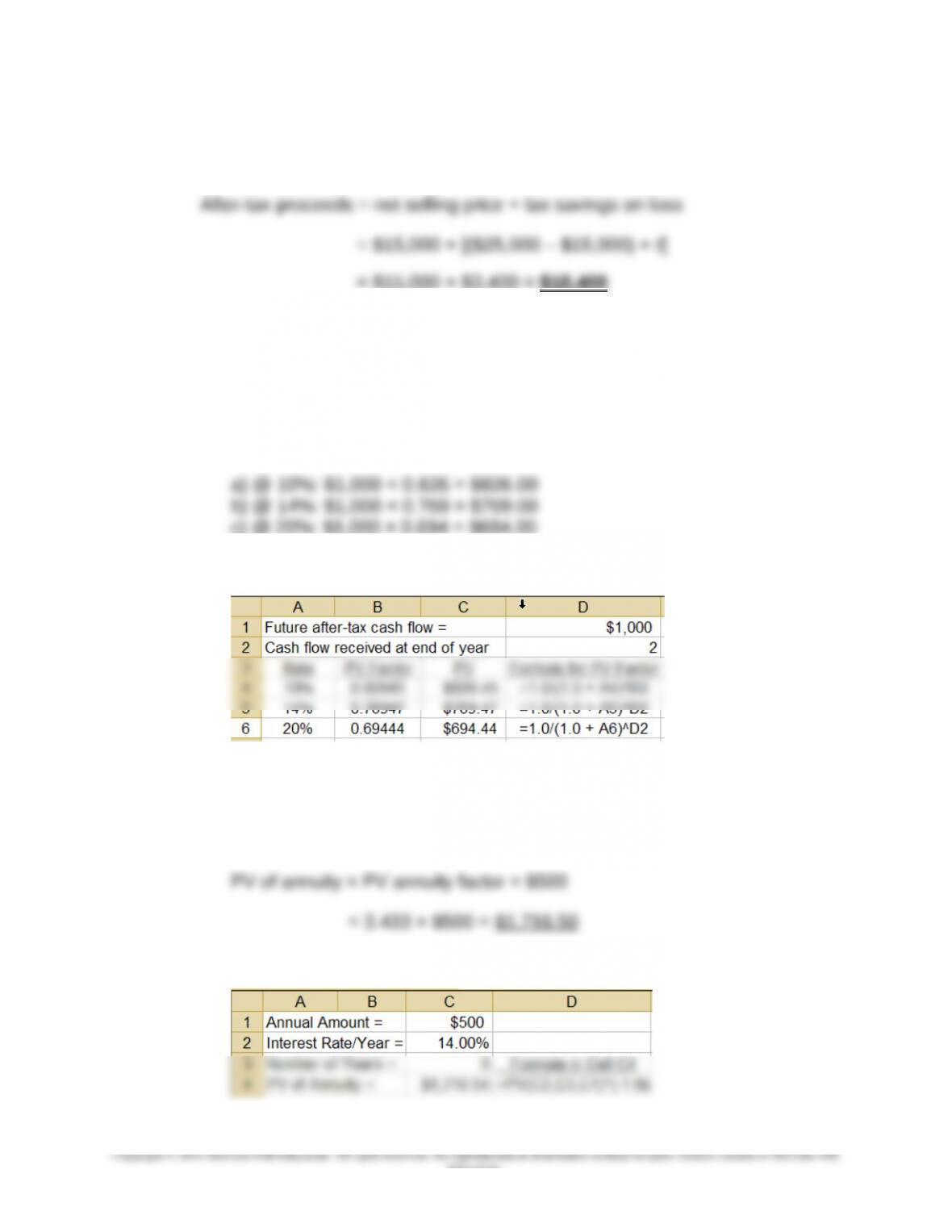

12-21 After-tax Proceeds, Asset Disposals

Given an NBV of $25,000 and a marginal income-tax rate of 34%:

a) If sales price = $35,000 (i.e., gain situation):

After-tax proceeds = net selling price – tax on gain

12-6

Education.

Asset Cost = $10,000

After-tax Discount Rate = 12.00%

Marginal Income-Tax Rate = 40.00%

MACRS Depreciation Tax PV Present

Year % Deduction Savings Factor Values

Chapter 12 - Strategy and the Analysis of Capital Investments

b) If sales price = $15,000 (i.e., loss situation):

= $15,000 + $3,400 = $18,400

12-22 Present Value of a Single Amount

Present value of $1,000 to be received two years from now (note that the difference

in answers below is attributable to rounding):

1) Using PV table (Chapter 12, Appendix C, Table 1):

2) Using Excel:

12-23 Present Value of an

Annuity

Given a 5-year stream of cash flows, $500 per year, at 14%:

a) Using the annuity table (Chapter 12, Appendix C, Table 2):

b) Using the built-in PV function in Excel:

12-7

Education.

Chapter 12 - Strategy and the Analysis of Capital Investments

12-24 IRR vs. MIRR

These two measures of investment profitability make different assumptions as to the

rate of return on cash inflows from the investment: the IRR assumes that these cash

inflows are reinvested at the IRR; the MIRR, on the other hand, assumes that these

cash inflows are reinvested at the WACC (discount rate). As such, the MIRR is a

more conservative estimate of a project's rate of profitability.

12-25 Estimating Weighted-Average Cost of Capital (WACC)

The weighted-average cost of capital (WACC) = 9.83%, as follows:

(1) (2)

Source of Funds Market Value

Required Rate of

Return Weights (1) × (2)

Long-term Debt $40 7.00% 0.3333 2.33%

12-8

Education.

Chapter 12 - Strategy and the Analysis of Capital Investments

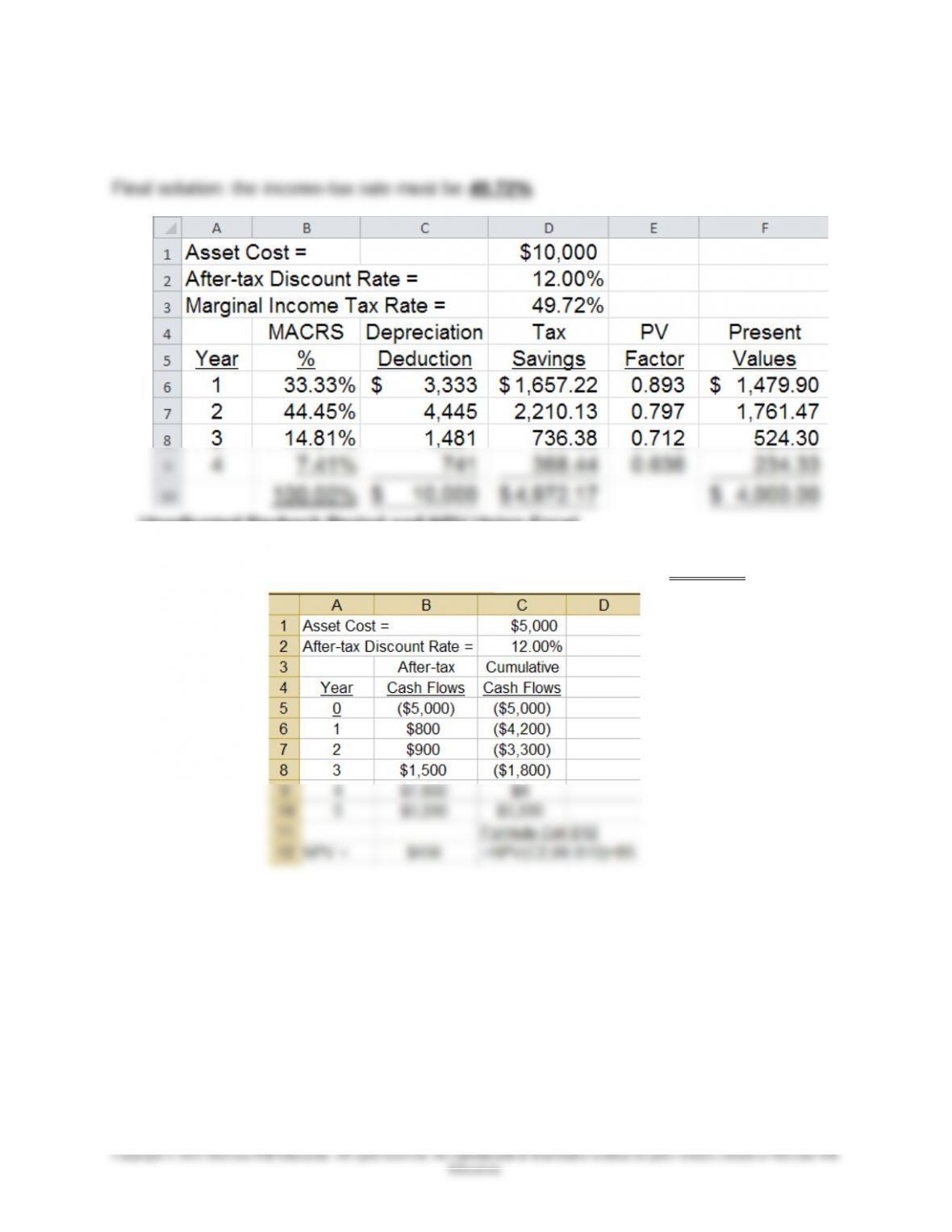

12-26 Sensitivity Analysis: Use of “Goal Seek” Function in Excel

Starting point = solution to Brief Exercise 12-20, as follows (note: the PV factors

below are entered from Appendix C, Table 1):

Then, use the following Goal Seek commands in Excel:

12-9

Education.

Chapter 12 - Strategy and the Analysis of Capital Investments

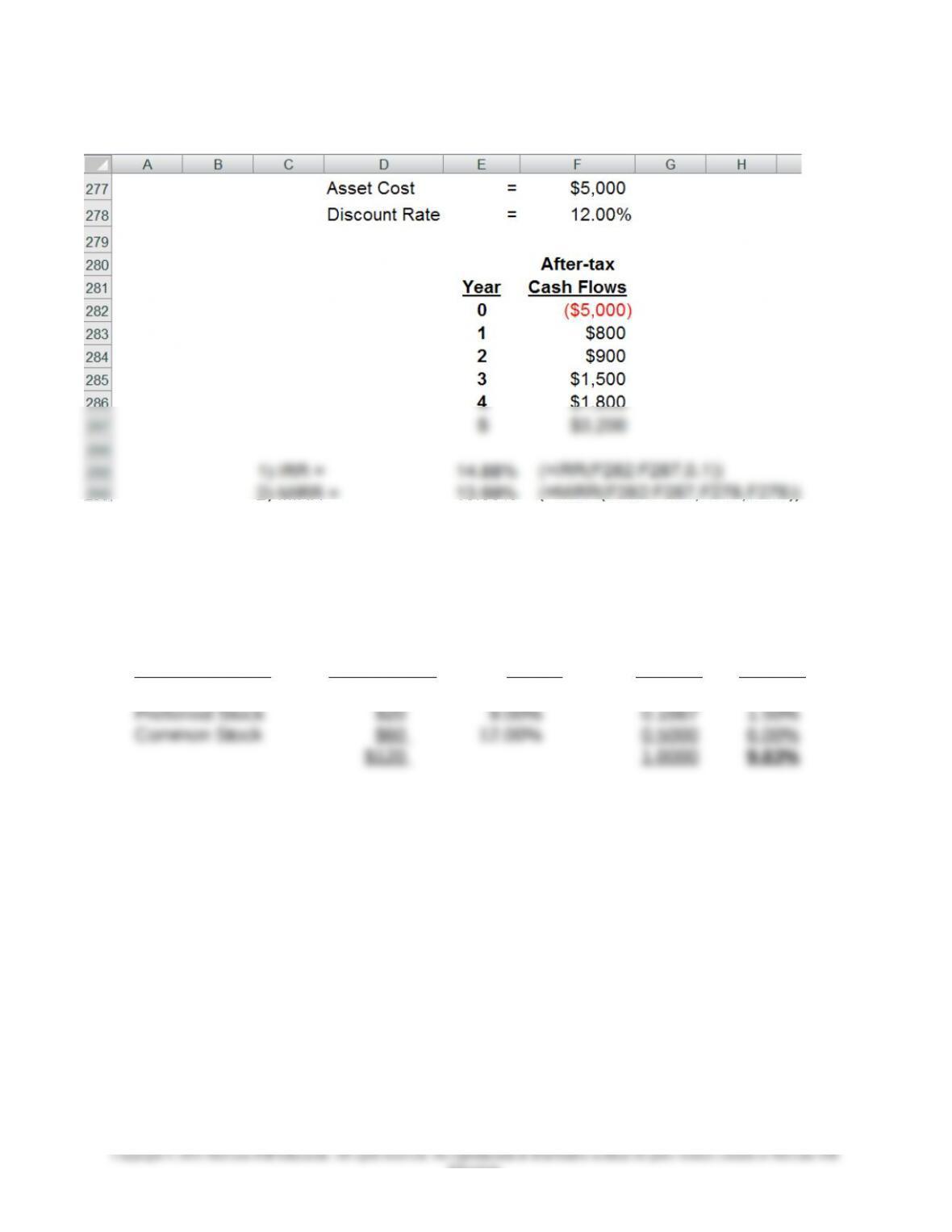

12-27

Unadjusted Payback Period and NPV Using Excel

The project’s NPV = $459 and the unadjusted payback period = 4.0 years

12-10