Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 4

Accounting for Merchandising

Operations

QUESTIONS

1. Merchandising companies report Merchandise Inventory on the balance sheet,

do not.

2. Additional accounts of a merchandising company likely include Merchandise

3. A company can have a net loss if its expenses (absent cost of goods sold) are

4. A cash discount can be offered to encourage customers to promptly pay. This

5. For a perpetual inventory system, inventory shrinkage is determined by taking a

6. Cash discounts are granted in return for early payment and reduce the amount paid

7. Sales discount is a term used by a seller to describe a cash discount granted to a

8. A manager is concerned about the quantity of its purchase returns because the

9. The sender (maker) of a debit memorandum records a debit in an account of the

Financial & Managerial Accounting, 5th Edition

232

10. The single-step income statement format presents cost of goods sold and expenses

11. Polaris calls its inventory account “Inventories, net.” A detailed calculation of cost

12. Arctic Cat titles its cost of goods sold account “Cost of goods sold.” Arctic Cat

13. Piaggio titles its cost of goods sold account “Cost for materials.”

14. KTM reports a separate gross margin figure on its consolidated income statement.

QUICK STUDIES

Quick Study 4-1 (10 minutes)

Quick Study 4-2 (5 minutes)

Quick Study 4-3 (15 minutes)

Nov. 5 Merchandise Inventory ..................................... 6,000

Accounts Payable ..................................... 6,000

To record credit purchase [(600 x $10].

Quick Study 4-4 (10 minutes)

Apr. 1 Accounts Receivable ..................................... 3,000

Sales ....................................................... 3,000

To record credit sale.

1 Cost of Goods Sold ........................................ 1,800

Merchandise Inventory ......................... 1,800

Financial & Managerial Accounting, 5th Edition

234

Quick Study 4-5 (10 minutes)

(a)

(b)

(c)

(d)

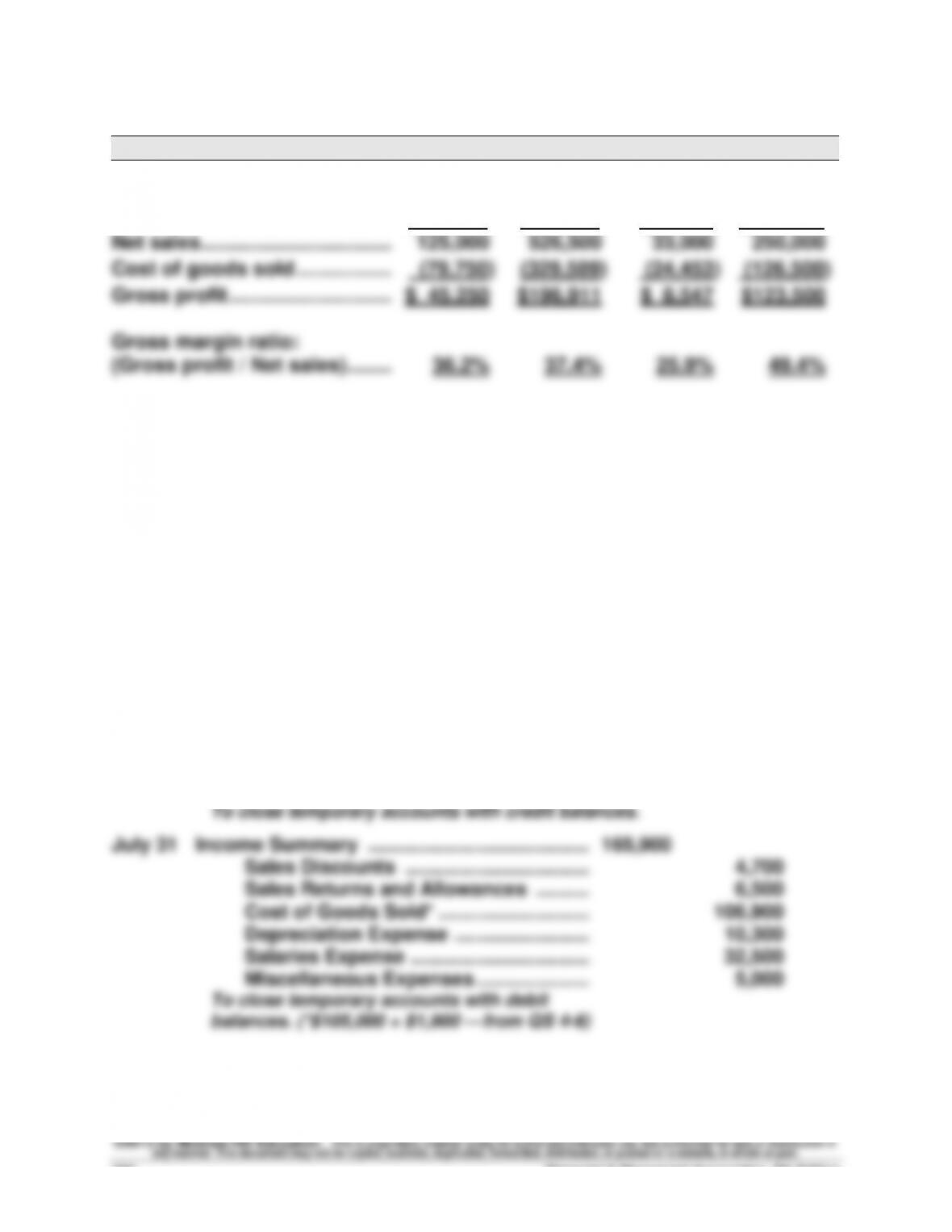

Sales ............................................

$150,000

$550,000

$38,700

$255,700

Sales discounts ..........................

(5,000)

(17,500)

(600)

(4,800)

Sales returns and allowances .......

(20,000)

(6,000)

(5,100)

(900)

Net sales ......................................

125,000

526,500

33,000

250,000

Cost of goods sold .....................

(79,750)

(329,589)

(24,453)

(126,500)

Gross profit ................................

$ 45,250

$196,911

$ 8,547

$123,500

Gross margin ratio:

(Gross profit / Net sales) ........ 36.2% 37.4% 25.9% 49.4%

Interpretation of gross margin ratio for case a: The ratio of 36.2% implies

that for each dollar in net sales the company earns 36.2 cents in gross

profit. The company must still deduct other expenses that it incurs in

running the business when computing net income.

Quick Study 4-6 (10 minutes)

July 31 Cost of Goods Sold .................................... 1,900

Merchandise Inventory ..................... 1,900

To adjust for shrinkage based on

physical count [$37,800 - $35,900].

Quick Study 4-7 (10 minutes)

July 31 Sales .............................................................. 160,200

Income Summary ................................. 160,200

Quick Study 4-8 (10 minutes)

in current liabilities as they come due. An acid-test ratio less than one usually

suggests some concern and encourages further analysis of liquidity.

Quick Study 4-9 (10 minutes)

Similarities: Both the acid-test ratio and current ratio are used to assess

liquidity. Both ratios are computed with current liabilities as the denominator.

Differences: The current ratio includes all current assets in the numerator.

The acid-test ratio includes current assets less inventories and prepaids in its

Quick Study 4-10 (10 minutes)

Quick Study 4-11A (5 minutes)

a. Periodic inventory system

Financial & Managerial Accounting, 5th Edition

236

Quick Study 4-12A (10 minutes)

Nov. 5 Purchases ........................................................... 6,000

Accounts Payable ...................................... 6,000

To record credit purchase [(600 x $10].

Quick Study 4-13A (10 minutes)

Apr. 1 Accounts Receivable ........................................ 3,000

Sales .......................................................... 3,000

To record credit sale.

Quick Study 4-14 (20 minutes)

1. Multiple-step income statement

adidas Group

Income Statement (€ millions)

For Year Ended December 31, 2011

Net sales ...................................................................... €13,344

Cost of sales ............................................................... 7,000

Gross profit ................................................................. 6,344

2. Single-step income statement

adidas Group

Income Statement (€ millions)

For Year Ended December 31, 2011

Revenues

Net sales ...................................................................... €13,344

Royalty and commission income ............................ 93

Quick Study 4-15 (10 minutes)

a. Both U.S. GAAP and IFRS include broad and similar guidance for the

accounting of merchandise purchases and sales.

b. Under IFRS, reference to finance costs usually refers to interest expense.

c. IFRS permits alternative measures of income to be reported as part of

the income statement.

Quick Study 4-16 (10 minutes)

a)

Aug. 1 Merchandise Inventory ...................................... 60,000

Accounts Payable ...................................... 60,000

Quick Study 4-17 (10 minutes)

a)

Sept. 15 Merchandise Inventory ...................................... 35,000

Accounts Payable ...................................... 35,000

To record credit purchase.

b)

Quick Study 4-18 (15 minutes)

Computation of net income:

Krug Service Co.

Revenues ...................................................

$14,000

Less: Expenses .........................................

8,500

Net income .................................................

$ 5,500

Kleiner Merchandising Co.

Sales ...........................................................

$ 9,500

Less: Cost of goods sold (see below*) ...

7,200

Gross profit ...............................................

2,300

Less: Operating expenses .......................

1,450

Net income .................................................

$ 850

*Computation of cost of goods sold: _

Beginning Inventory

$ 5,000

Plus: Purchases

3,900

Goods available for sale

8,900

Less: Ending inventory

1,700

Cost of goods sold

$ 7,200

EXERCISES

Exercise 4-1 (10 minutes)

Operating cycle of a merchandiser with credit sales follows (chronological):

Exercise 4-2 (30 minutes)

Apr. 2 Merchandise Inventory ..................................... 4,600

Accounts Payable—Lyon .......................... 4,600

Purchased merchandise on credit.

3 Merchandise Inventory ..................................... 300

Cash ............................................................ 300

Paid shipping charges on purchased

merchandise.

Financial & Managerial Accounting, 5th Edition

242

Exercise 4-3 (30 minutes)

1. BUYER- Santa Fe Company

a) Credit Purchase

Merchandise Inventory .................................... 24,000

Accounts Payable ..................................... 24,000

Purchased merchandise on credit.

2. SELLER – Mesa Company

a) Credit Sale

Accounts Receivable ....................................... 24,000

Sales ........................................................... 24,000

Sold merchandise on account.

3. Amount borrowed to pay with discount ....................... $ 23,280

Annual rate of interest ................................................... x 8%

Interest per year .............................................................. $1,862.40

Exercise 4-4 (30 minutes)

May 5 Accounts Receivable ....................................... 21,000

a.

May 7 Sales Returns and Allowances ....................... 2,800

Accounts Receivable ................................ 2,800

b.

May 8 Sales Returns and Allowances ........................ 600

Accounts Receivable ................................. 600

Granted allowance for damaged merchandise.

c.

May 15 Sales Returns and Allowances ........................ 680

Financial & Managerial Accounting, 5th Edition

244

Exercise 4-5 (15 minutes)

May 5 Merchandise Inventory .................................... 21,000

Accounts Payable ..................................... 21,000

Purchased merchandise on credit (1,500 x $14).

a.

May 7 Accounts Payable ............................................ 2,800

Merchandise Inventory ............................. 2,800

Exercise 4-6 (20 minutes)

In today’s competitive world, organizations must concentrate on meeting their

customers’ needs and avoiding dissatisfaction. If these needs are not met

and dissatisfaction grows, the customers will deal with other companies or

entities. One measure of dissatisfaction of customers is the amount of sold

goods that are later returned. Customer dissatisfaction needs to be

understood and then dealt with promptly to encourage them to remain loyal.