Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Problem 22-2B (Continued)

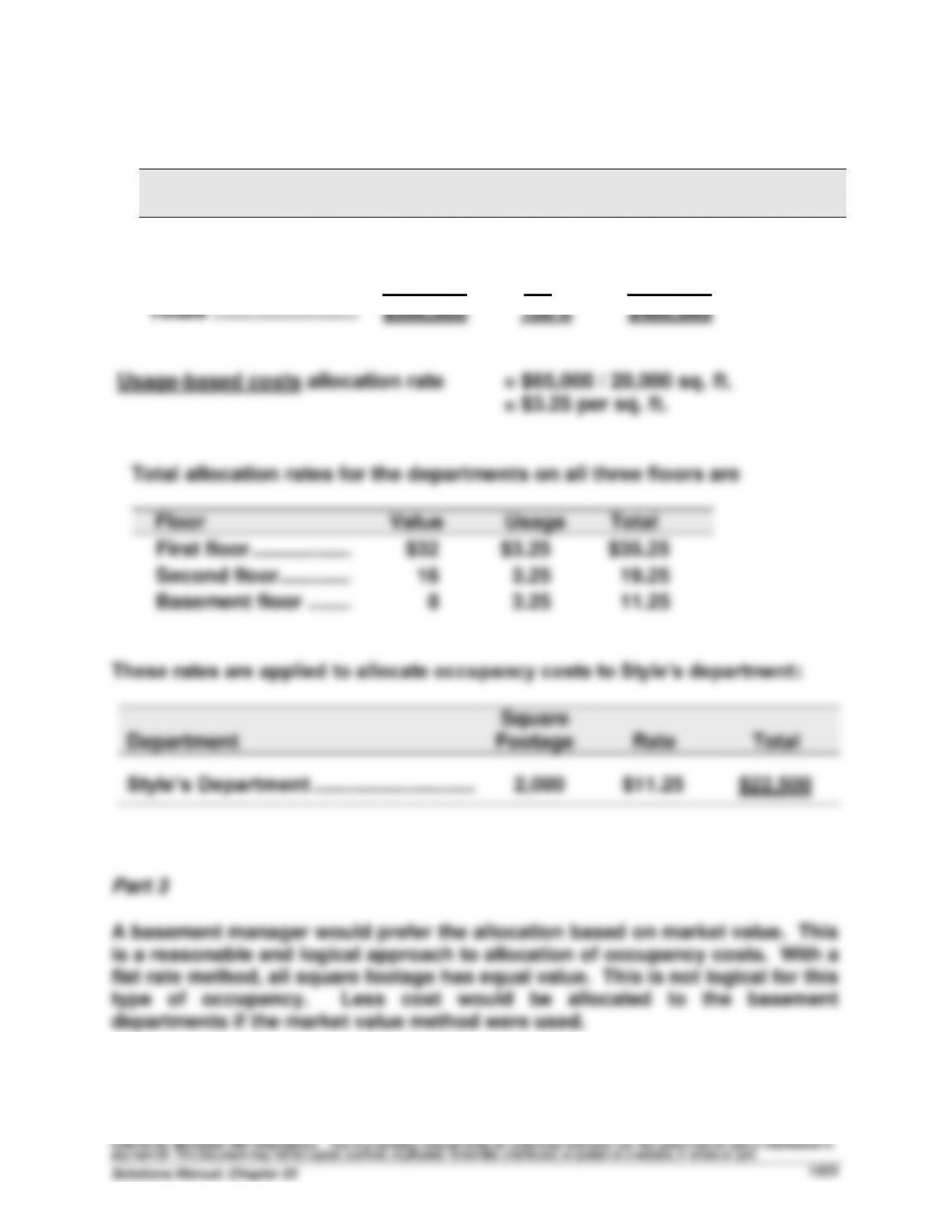

(ii) Allocate the $400,000 to each floor based on its percent of market value

Floor

Market

Value

% of

Total

Allocated

Cost

Cost per

Sq. Ft.

First floor ................................

$300,000

60%

$240,000

$32.00

Second floor ...........................

150,000

30

120,000

16.00

Basement floor .......................

50,000

10

40,000

8.00

Totals ................................

$500,000

100%

$400,000

Usage-based costs allocation rate = $65,000 / 20,000 sq. ft.

= $3.25 per sq. ft.

Total allocation rates for the departments on all three floors are

Floor

Value

Usage

Total

First floor ..............................

$32

$3.25

$35.25

Second floor .........................

16

3.25

19.25

Basement floor ....................

8

3.25

11.25

These rates are applied to allocate occupancy costs to Style’s department:

Department

Square

Footage

Rate

Total

Style’s Department ................................

2,000

$11.25

$22,500

Part 3

A basement manager would prefer the allocation based on market value. This

is a reasonable and logical approach to allocation of occupancy costs. With a

flat rate method, all square footage has equal value. This is not logical for this

type of occupancy. Less cost would be allocated to the basement

departments if the market value method were used.

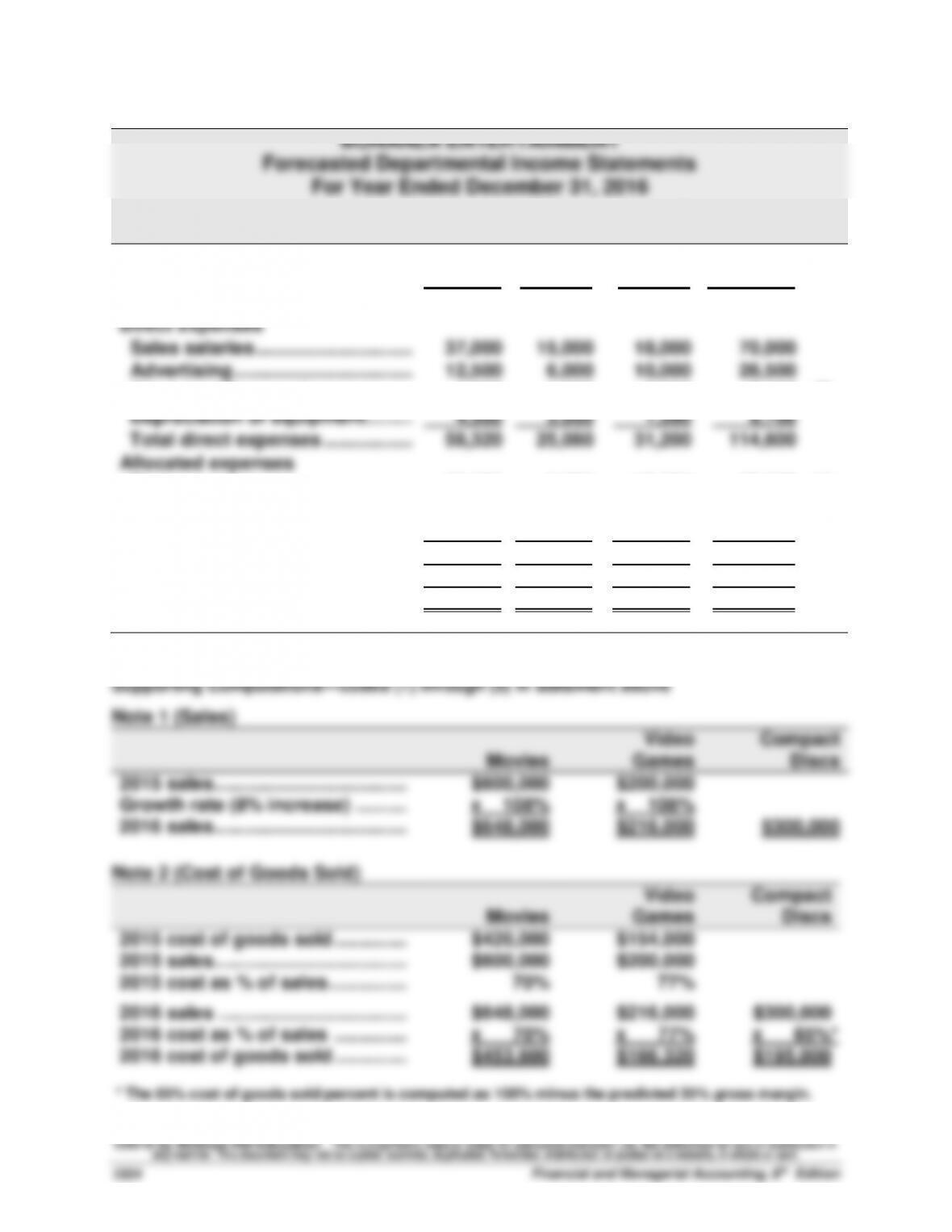

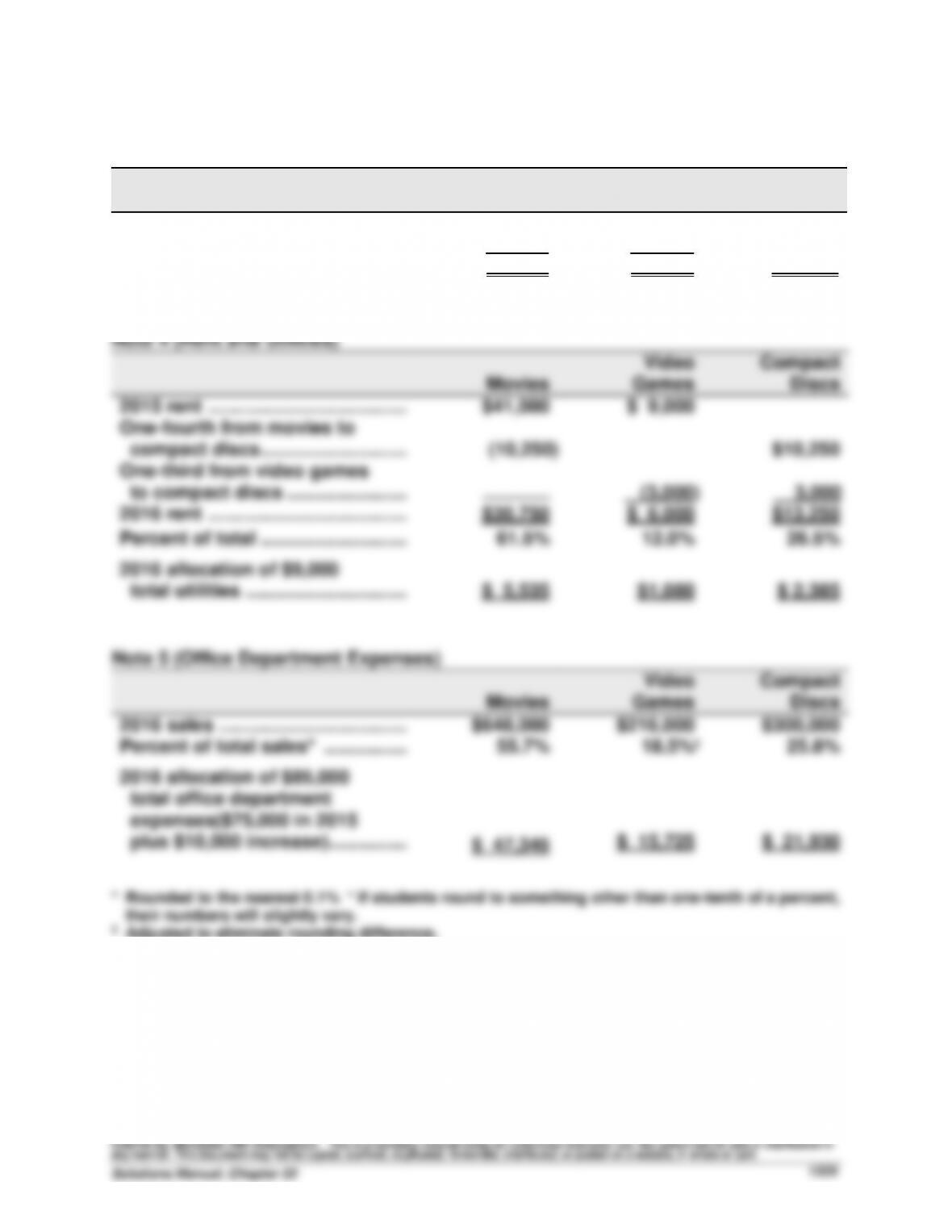

Problem 22-3B (70 minutes)

BONANZA ENTERTAINMENT

Forecasted Departmental Income Statements

For Year Ended December 31, 2016

Movies

Video

Games

Compact

Discs

Combined

Sales ...............................................

$648,000

$216,000

$300,000

$1,164,000

(1)

Cost of goods sold ........................

453,600

166,320

195,000

814,920

(2)

Gross profit ....................................

194,400

49,680

105,000

349,080

Direct expenses

Sales salaries ...............................

37,000

15,000

18,000

70,000

Advertising ...................................

12,500

6,000

10,000

28,500

Store supplies used .....................

4,320

1,080

2,000

7,400

(3)

Depreciation of equipment..........

4,500

3,000

1,200

8,700

Total direct expenses ..................

58,320

25,080

31,200

114,600

Allocated expenses

Rent expense ...............................

30,750

6,000

13,250

50,000

(4)

Utilities expense ..........................

5,535

1,080

2,385

9,000

(4)

Share of office dept. expenses ...

47,345

15,725

21,930

85,000

(5)

Total allocated expenses ............

83,630

22,805

37,565

144,000

Total expenses ...............................

141,950

47,885

68,765

258,600

Net income .....................................

$ 52,450

$ 1,795

$ 36,235

$ 90,480

Problem 22-3B (Continued)

Note 3 (Store Supplies Used)

Movies

Video

Games

Compact

Discs

2015 store supplies used ...........

$ 4,000

$ 1,000

Growth rate (8% increase) ..........

x 108%

x 108%

2016 store supplies ....................

$ 4,320

$ 1,080

$ 2,000

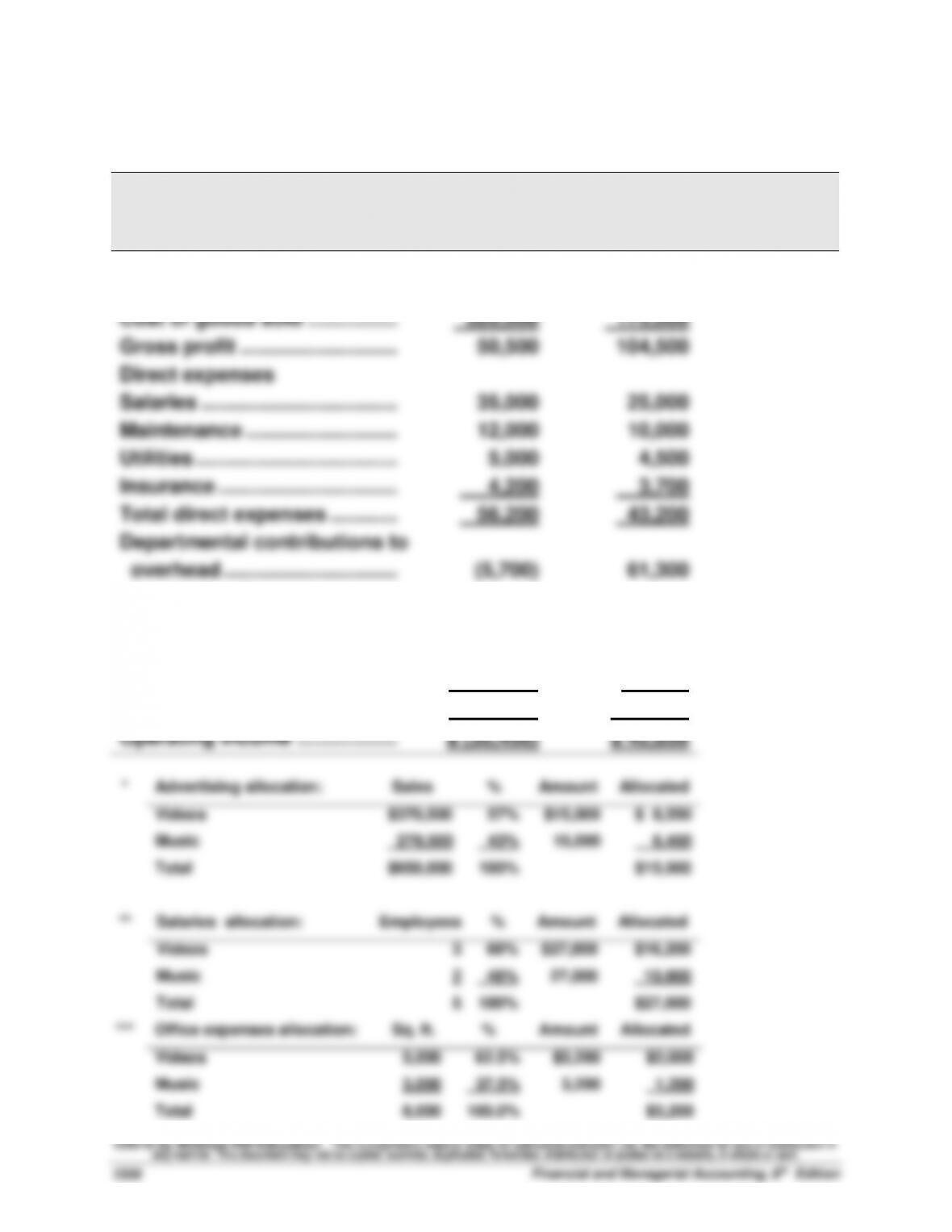

Problem 22-4B (45 minutes)

Part 1

SADAR COMPANY

Departmental Contribution Statements

Videos

Music

Sales ........................................

$370,500

$279,500

Cost of goods sold ................

320,000

175,000

Gross profit ............................

50,500

104,500

Direct expenses

Salaries ...................................

35,000

25,000

Maintenance ...........................

Utilities ....................................

Insurance ................................

12,000

5,000

4,200

10,000

4,500

3,700

Total direct expenses ............

56,200

43,200

Departmental contributions to

overhead ...............................

Allocated indirect expenses

(5,700)

61,300

Advertising* ............................

8,550

6,450

Salaries** ................................

16,200

10,800

Office**** .................................

Total indirect expenses .........

2,000

26,750

1,200

18,450

Operating income ..................

$ (32,450)

$ 42,850

*

Advertising allocation:

Sales

%

Amount

Allocated

Videos

$370,500

57%

$15,000

$ 8,550

Music

279,500

43%

15,000

6,450

Total

$650,000

100%

$15,000

**

Salaries allocation:

Employees

%

Amount

Allocated

Videos

3

60%

$27,000

$16,200

Music

2

40%

27,000

10,800

Total

5

100%

$27,000

***

Office expenses allocation:

Sq. ft.

%

Amount

Allocated

Videos

5,000

62.5%

$3,200

$2,000

Music

3,000

37.5%

3,200

1,200

Total

8,000

100.0%

$3,200

Problem 22-4B (Concluded)

Part 2

The videos department has both a negative contribution to overhead and a

negative departmental net income. It is not even covering its own direct

Problem 22-5BB (60 minutes)

Part 1

Allocations of joint cost on the basis of sales values

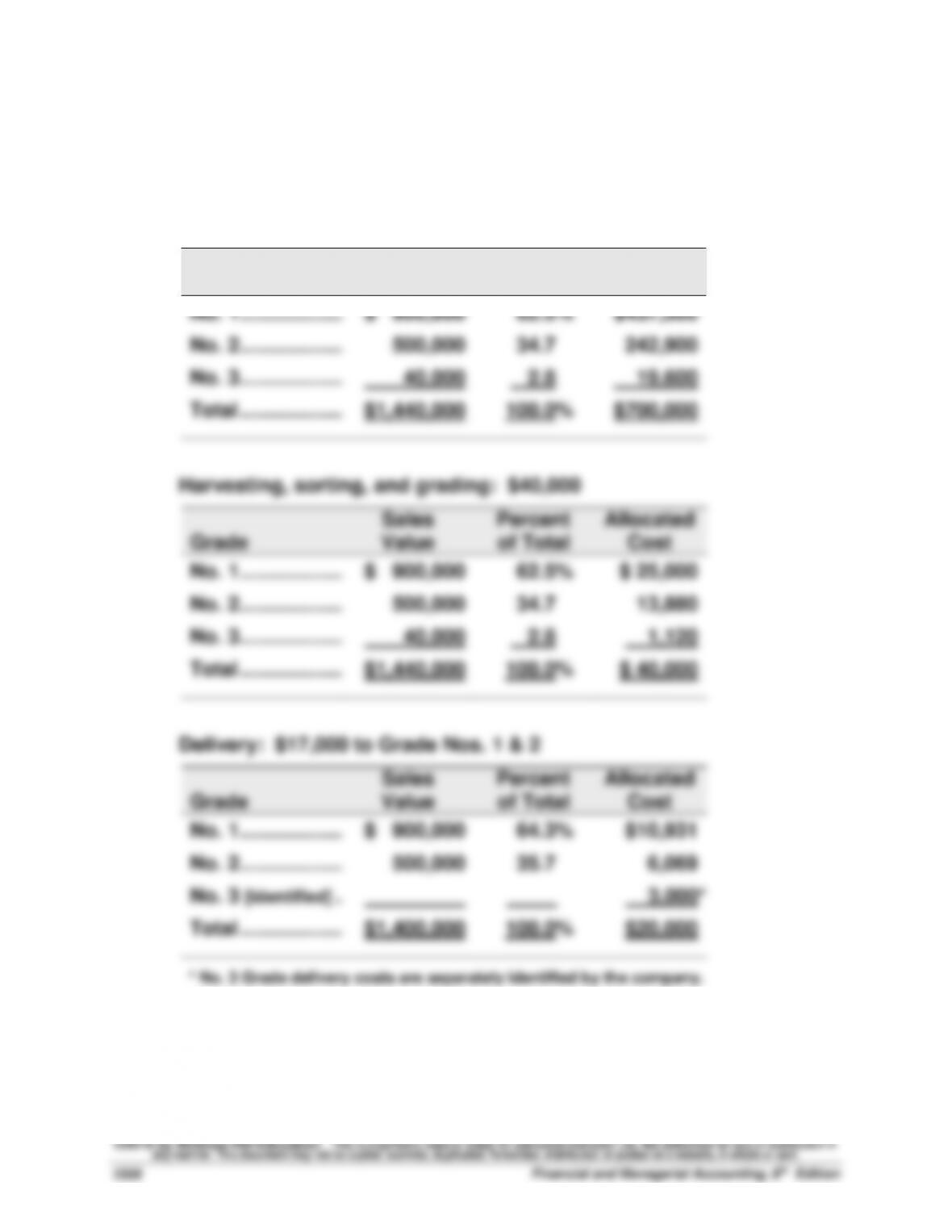

Land preparation, seeding, and cultivating: $700,000

Grade

Sales

Value

Percent of

Total

Allocated

Cost

No. 1 ...............................

$ 900,000

62.5%

$437,500

No. 2 ...............................

500,000

34.7

242,900

No. 3 ...............................

40,000

2.8

19,600

Total ...............................

$1,440,000

100.0%

$700,000

Harvesting, sorting, and grading: $40,000

Grade

Sales

Value

Percent

of Total

Allocated

Cost

No. 1 ...............................

$ 900,000

62.5%

$ 25,000

No. 2 ...............................

500,000

34.7

13,880

No. 3 ...............................

40,000

2.8

1,120

Total ...............................

$1,440,000

100.0%

$ 40,000

Delivery: $17,000 to Grade Nos. 1 & 2

Grade

Sales

Value

Percent

of Total

Allocated

Cost

No. 1 ...............................

$ 900,000

64.3%

$10,931

No. 2 ...............................

500,000

35.7

6,069

No. 3 [identified] ..............

3,000*

Total ...............................

$1,400,000

100.0%

$20,000

* No. 3 Grade delivery costs are separately identified by the company.

Problem 22-5B (Continued)

Part 2

RITA AND RICK REDDING

Income Statement

For Year Ended December 31, 2015

No. 1

No. 2

No. 3

Combined

Sales (by grade)

No. 1: 500,000 lbs. @ $1.80 ..........

$900,000

No. 2: 400,000 lbs. @ $1.25 ..........

$500,000

No. 3: 100,000 lbs. @ $0.40 ..........

$40,000

Total sales .....................................

$1,440,000

Costs

Land preparation, seeding,

and cultivating ............................

437,500

242,900

19,600

700,000

Harvesting, sorting & grading .....

25,000

13,880

1,120

40,000

Delivery ..........................................

10,931

6,069

3,000

20,000

Total costs .....................................

473,431

262,849

23,720

760,000

Net income (loss) ............................

$426,569

$237,151

$16,280

$680,000

Part 3

Delivery costs include both crating and hauling costs. The Reddings are

able to identify the portion of the cost directly related to the No. 3

tomatoes, presumably because the No. 3s are going to a different

destination than the No. 1 and No. 2 tomatoes. If the No. 1s and No. 2s are

going to the same place, then the hauling portion of the delivery cost may

truly be a joint cost, at least for the No. 1 and No. 2 tomatoes.

However, since the No. 1 and No. 2 tomatoes are different grades and are

sold for different prices per pound, it seems safe to assume they are crated

separately. If the cost of crating the No. 3 tomatoes can be traced as a

direct cost, then it seems the crating costs for the No. 1s and No. 2s should

1. The balanced scorecard is a system of performance measures that

requires managers to think of their company from four perspectives:

Customer, internal process, innovation and learning, and financial.

2. Below are some examples of balanced scorecard measures that

Santana could use. Other examples are possible:

Customer: Percentage of computer workstations returned, number of

on-time workstation deliveries, number of on-time