Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 18 - Portfolio Performance Evaluation

CHAPTER 18

PORTFOLIO PERFORMANCE EVALUATION

1. a. Possibly. Alpha alone does not determine which portfolio has a larger Sharpe

ratio. Sharpe measure is the primary factor, since it tells us the real return per

unit of risk. We only invest if the Sharpe measure is higher. The standard

b. Yes. It is possible for a positive alpha to exist, but the Sharpe measure declines.

Thus, we would experience inferior performance.

2. Maybe. Provided the addition of funds creates an efficient frontier with the existing

3. No. The M-squared is an equivalent representation of the Sharpe measure, with the

4. Definitely the FF model. Research shows that passive investments (e.g., a market index

5.

a.

E(r)

Portfolio A

11%

10%

.8

Portfolio B

14%

31%

1.5

Chapter 18 - Portfolio Performance Evaluation

b. If you hold only one of the two portfolios, then the Sharpe measure is the

appropriate criterion:

6. We first distinguish between timing ability and selection ability. The intercept of the

scatter diagram is a measure of stock selection ability. If the manager tends to have a

positive excess return even when the market’s performance is merely “neutral” (i.e., the

market has zero excess return) then we conclude that the manager has, on average,

made good stock picks. In other words, stock selection must be the source of the

positive excess returns.

We can therefore classify performance ability for the four managers as follows:

Selection Ability

Timing Ability

A

Bad

Good

a. Actual: (.70 .02) + (.20 .01) + (.10 .005) = .0165 = 1.65%

Chapter 18 - Portfolio Performance Evaluation

b. Security Selection:

(1)

(2)

(3)

(4)

(5) = (3) (4)

Bonds

1.0%

1.2%

– .2%

.20

– .04%

c. Asset Allocation:

(1)

(2)

(3)

(4)

(5) = (3) (4)

Actual

Benchmark

Excess

8. Support: A manager could be a better forecaster in one scenario than another. For

example, a high-beta manager will do better in up markets and worse in down markets.

Therefore, we should observe performance over an entire cycle. Also, to the extent that

9. It does, to some degree. If those manager groups are sufficiently homogeneous with

respect to style, then relative performance is a decent benchmark. However, one would

like to be able to adjust for the additional variation in style or risk choice that remains

10. The manager’s alpha is: Actual return – Required return predicted by CAPM

11. a. The most likely reason for a difference in ranking is due to the absence of

diversification in Fund A. The Sharpe ratio measures excess return per unit of total

12. The within sector selection calculates the return according to security selection. This is

done by summing the weight of the security in the portfolio multiplied by the return of

the security in the portfolio minus the return of the security in the benchmark:

Selection effect = (Portfolio return – Bogey return) Portfolio weight

Large-cap growth: (.17 – .16) = =

13. Primo return

0.6 17% 0.15 24% 0.25 20% 18.8%= + + =

Benchmark return

0.5 16% 0.4 26% 0.1 18% 20.2%= + + =

14. Because the passively managed fund is mimicking the benchmark, the

2

R

of the

regression should be very high (and thus probably higher than the actively managed

fund).

15. a. The euro appreciated while the pound depreciated. Primo had a greater stake in the

euro-denominated assets relative to the benchmark, resulting in a positive currency

allocation effect. British stocks outperformed Dutch stocks resulting in a negative

16.

a. SP = E(rP) - rf

P = .102 - .02

.37 = .2216

b. To compute

2

M

measure, blend the Miranda Fund with a position in T-Bills

such that the “adjusted” portfolio has the same volatility as the market index.

Calculate the difference in the adjusted Miranda Fund return and the

benchmark:

[Note: The adjusted Miranda Fund is now 59.46% equity and 40.54% cash.]

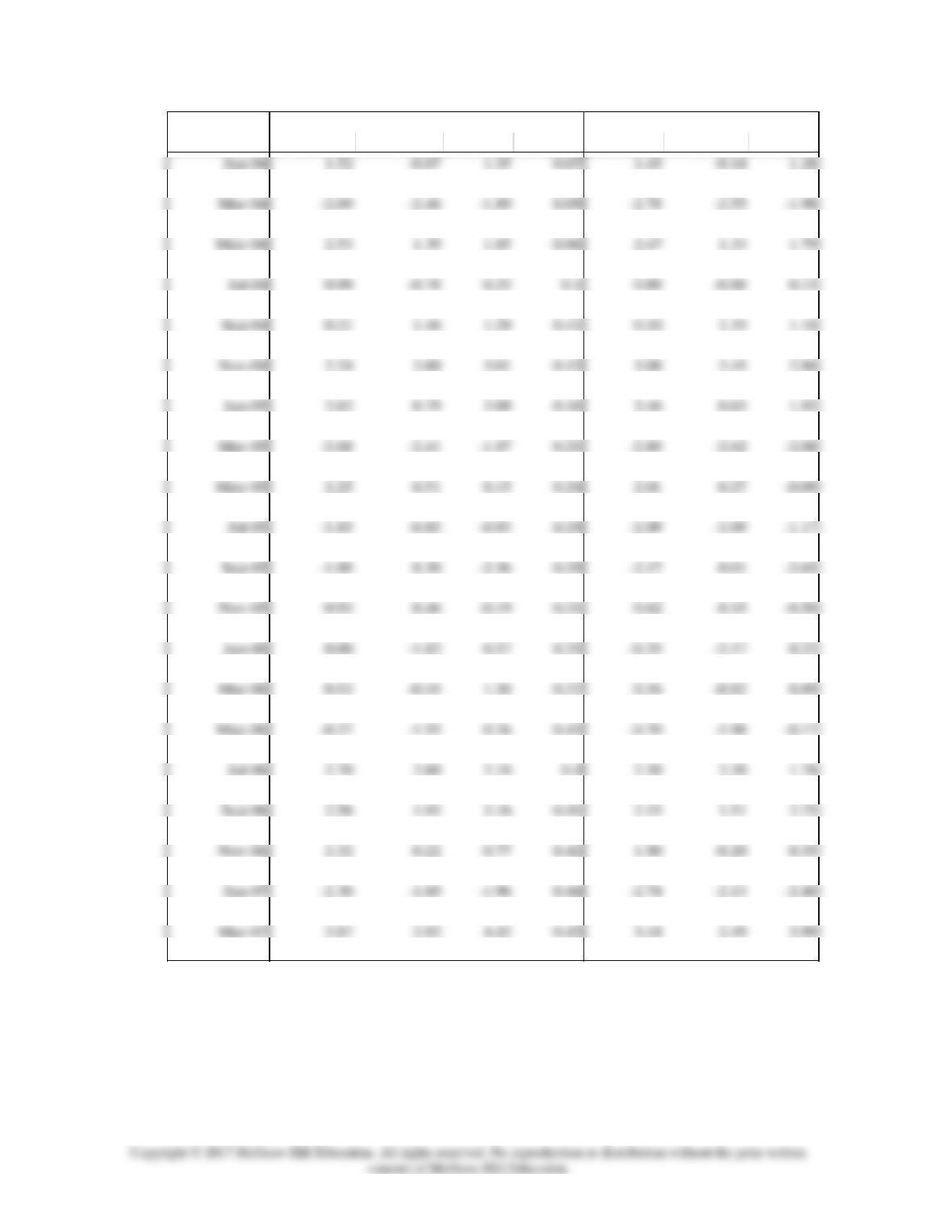

17. The spreadsheet below displays the monthly returns and excess returns for the

Vanguard U.S. Growth Fund, the Vanguard U.S. Value Fund and the S&P 500.

Chapter 18 - Portfolio Performance Evaluation

Total monthly returns Excess Returns

Month Vanguard Value Fund S&P T-bills Vanguard Value Fund S&P

Feb-04 -0.53 -0.99 -1.32 0.06 -0.59 -1.05 -1.38

Apr-04 0.22 2.52 1.70 0.08 0.14 2.44 1.62

Jun-04 -1.93 -7.46 -3.22 0.08 -2.01 -7.54 -3.30

Aug-04 1.52 2.49 1.00 0.11 1.41 2.38 0.89

Oct-04 5.22 4.66 4.46 0.11 5.11 4.55 4.35

Dec-04 -2.36 -3.48 -2.24 0.16 -2.52 -3.64 -2.40

Feb-05 -2.33 -2.86 -1.83 0.16 -2.49 -3.02 -1.99

Apr-05 4.08 7.13 3.22 0.21 3.87 6.92 3.01

Jun-05 3.55 5.28 3.82 0.23 3.32 5.05 3.59

Aug-05 0.38 1.34 0.80 0.3 0.08 1.04 0.50

Oct-05 2.87 5.04 4.39 0.27 2.60 4.77 4.12

Dec-05 3.41 3.30 2.41 0.32 3.09 2.98 2.09

Feb-06 0.71 0.34 1.65 0.34 0.37 0.00 1.31

Apr-06 -3.00 -5.84 -3.01 0.36 -3.36 -6.20 -3.37

Jun-06 1.09 -2.36 0.45 0.4 0.69 -2.76 0.05

Aug-06 2.63 2.87 2.70 0.42 2.21 2.45 2.28

Oct-06 0.75 1.94 1.99 0.41 0.34 1.53 1.58

Dec-06 1.86 2.18 1.51 0.4 1.46 1.78 1.11

Feb-07 0.81 0.89 1.16 0.38 0.43 0.51 0.78

Apr-07 3.65 3.37 3.39 0.44 3.21 2.93 2.95

Chapter 18 - Portfolio Performance Evaluation

Jun-07 -4.74 -0.79 -3.13 0.4 -5.14 -1.19 -3.53

Aug-07 2.54 4.91 3.88 0.42 2.12 4.49 3.46

Oct-07 -5.86 -3.90 -3.87 0.32 -6.18 -4.22 -4.19

Dec-07 -5.39 -10.34 -6.04 0.27 -5.66 -10.61 -6.31

Feb-08 -0.89 -0.06 -0.90 0.13 -1.02 -0.19 -1.03

Apr-08 1.44 3.00 1.51 0.17 1.27 2.83 1.34

Jun-08 -1.80 -0.40 -0.90 0.17 -1.97 -0.57 -1.07

Aug-08 -7.50 -11.63 -9.42 0.12 -7.62 -11.75 -9.54

Oct-08 -7.16 -7.93 -6.96 0.08 -7.24 -8.01 -7.04

Dec-08 -10.76 -4.49 -8.22 0.09 -10.85 -4.58 -8.31

Average -0.59 -0.60 -0.55

bSD 4.05 4.21 3.81

c Beta 1.03 1.02 1.00

a. The excess returns are noted in the spreadsheet.

d. The formulas for the three measures are below and results listed above.

Sharpe: E(rP) - rf

P

Chapter 18 - Portfolio Performance Evaluation

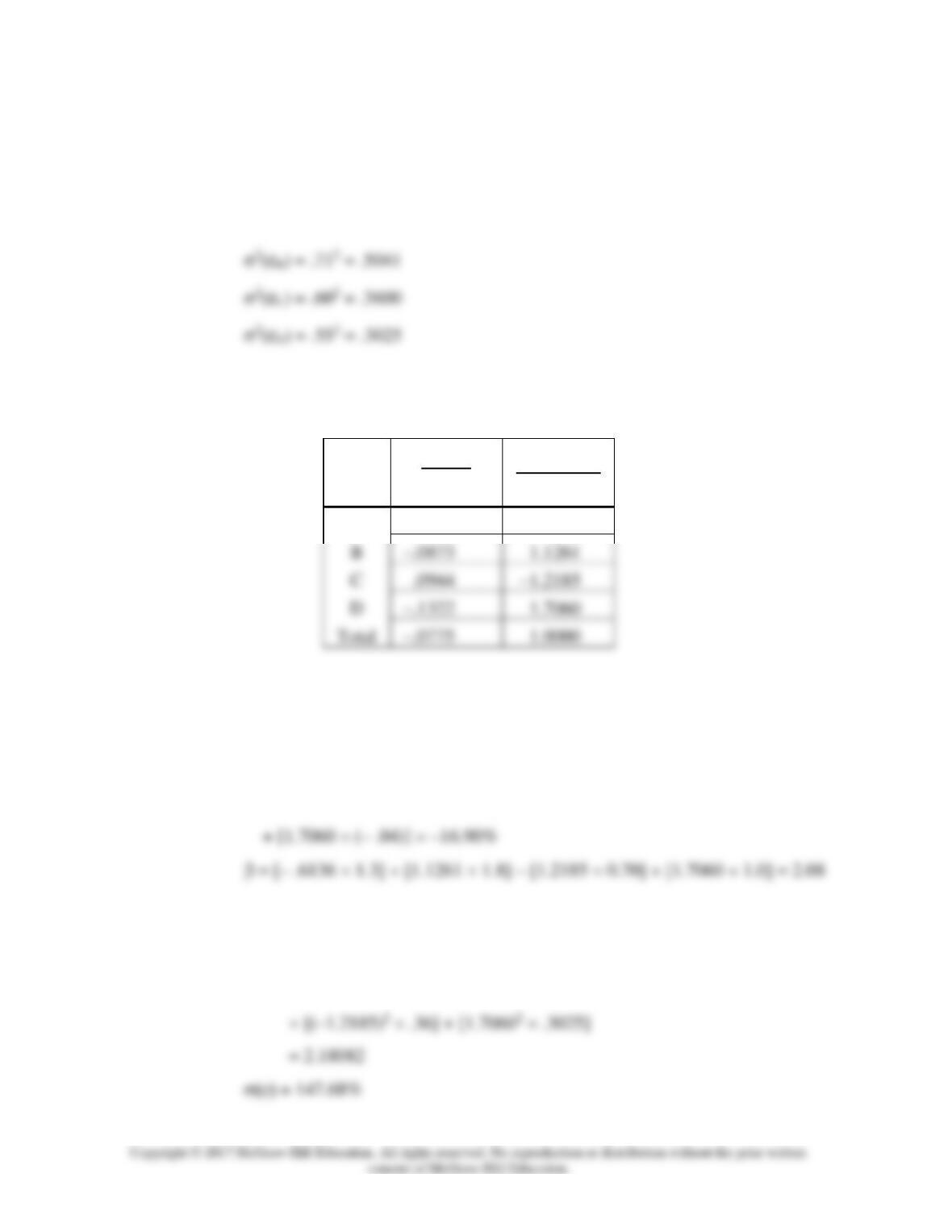

SUMMARY OUTPUT Vanguard

Regression Statistics

Multiple R 0.97

ANOVA

df SS MS F

Regression 1.00 907.97 907.97 876.67

Coefficients Standard Error t Stat P-value

SUMMARY OUTPUT Value Fund

Regression Statistics

Multiple R 0.93

R Square 0.86

ANOVA

df SS MS F

Regression 1.00 896.12 896.12 343.89

Coefficients Standard Error t Stat P-value

Intercept (0.04) 0.21 (0.17) 0.86

18. See the Black-Scholes formula. Substitute:

Current stock price = S0 = $1.0

Exercise price = X = (1 + rf) = 1.01

Standard deviation = = .055

Chapter 18 - Portfolio Performance Evaluation

N(/2) is the cumulative standard normal density for the value of half the standard

deviation of the equity portfolio.

19.

a. Using the relative frequencies to estimate the conditional probabilities P1 and P2

for timers A and B, we find:

Timer A

Timer B

P1

78/135 = 0.58

86/135 = 0.64

b. Use the following equation and the previous answer to value the imperfect timing

services of Timer A and Timer B:

C(P*) = C(P1 + P2 – 1)

CFA 1

Answer:

CFA 2

Answer:

a. αA = .24 – [ .12 + 1.0 ( .21 – .12)] = 3.0%

b. (i) The managers may have been trying to time the market. In that case, the

Chapter 18 - Portfolio Performance Evaluation

CFA 3

Answer:

a. Indeed, the one year results were terrible, but one year is a poor statistical base

from which to draw inferences. Moreover, the fund manager was directed to

b. The sample of pension funds held a much larger share in equities compared to

the Alpine pension fund. The stock and bond indexes indicate that equity returns

significantly exceeded bond returns. The Alpine fund manager was explicitly

c. Over the five-year period, Alpine’s alpha, which measures risk-adjusted

performance compared to the market, was positive:

d. Note that, over the last five years, and particularly the last one year, bond

performance has been poor; this is significant because this is the asset class that

Alpine had been encouraged to hold. Within this asset class, however, the

e. A trustee may not care about the time-weighted return, but that return is more

CFA 4

Answer:

a.

Alpha (): αi = E(ri) – {rf + βi [E(rM) – rf ]}

Expected excess return: E(ri) – rf

αA = .20 – [ .08 + 1.3 ( .16 – .08)] = 1.6%

.20 – .08 = 12%

Chapter 18 - Portfolio Performance Evaluation

Stocks A and C have positive alphas, whereas stocks B and D have negative

alphas.

The residual variances are:

2(eA) = .582 = .3364

b. To construct the optimal risky portfolio, we first determine the optimal active

portfolio. Using the Treynor-Black technique, we construct the active

portfolio:

2(e)

2(e)

αi2(ei)

A

.0476

–0.6136

Do not be disturbed by the fact that the positive alpha stocks get negative

weights and vice versa. The entire position in the active portfolio will turn out

to be negative, returning everything to good order.

With these weights, the forecast for the active portfolio is:

α = [– .6136 .016] + [1.1261 (– .044)] – [1.2185 .034]

The high beta (higher than any individual beta) results from the short positions

in the relatively low beta stocks and the long positions in the relatively high

beta stocks.

2(e) = [(– .6136)2 .3364] + [1.12612 .5041]

Chapter 18 - Portfolio Performance Evaluation

Here, again, the levered position in stock B [with the high 2(e)] overcomes the

diversification effect, and results in a high residual standard deviation. The

optimal risky portfolio has a proportion w* in the active portfolio, computed as

follows:

The negative position is justified for the reason given earlier.

The adjustment for beta is:

Because w* is negative, we end up with a positive position in stocks with

positive alphas and vice versa. The position in the index portfolio is:

c. To calculate Sharpe's measure for the optimal risky portfolio we compute the

appraisal ratio for the active portfolio and Sharpe's measure for the market

portfolio. The appraisal ratio of the active portfolio is:

Hence, the square of Sharpe's measure (S) of the optimized risky portfolio is:

The difference is: .0184

Note that the only-moderate improvement in performance results from the fact

that only a small position is taken in the active portfolio A because of its large

residual variance.

We calculate the "Modigliani-squared" (M2) measure, as follows: