Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

CHAPTER 3

WORKING WITH FINANCIAL

STATEMENTS

Answers to Concepts Review and Critical Thinking Questions

1. a. If inventory is purchased with cash, then there is no change in the current ratio. If inventory is

3. A current ratio of 0.50 means that the firm has twice as much in current liabilities as it does in current

CHAPTER 3 - 2

5. Common-size financial statements express all balance sheet accounts as a percentage of total assets

7. Return on equity is probably the most important accounting ratio that measures the bottom-line

CHAPTER 3 - 3

11. Reporting the sale of Treasury securities as cash flow from operations is an accounting “trick,” and as

Solutions to Questions and Problems

Basic

1. Using the formula for NWC, we get:

2. We need to find net income first. So:

CHAPTER 3 - 4

5. Total debt ratio = 0.46 = TD / TA

CHAPTER 3 - 5

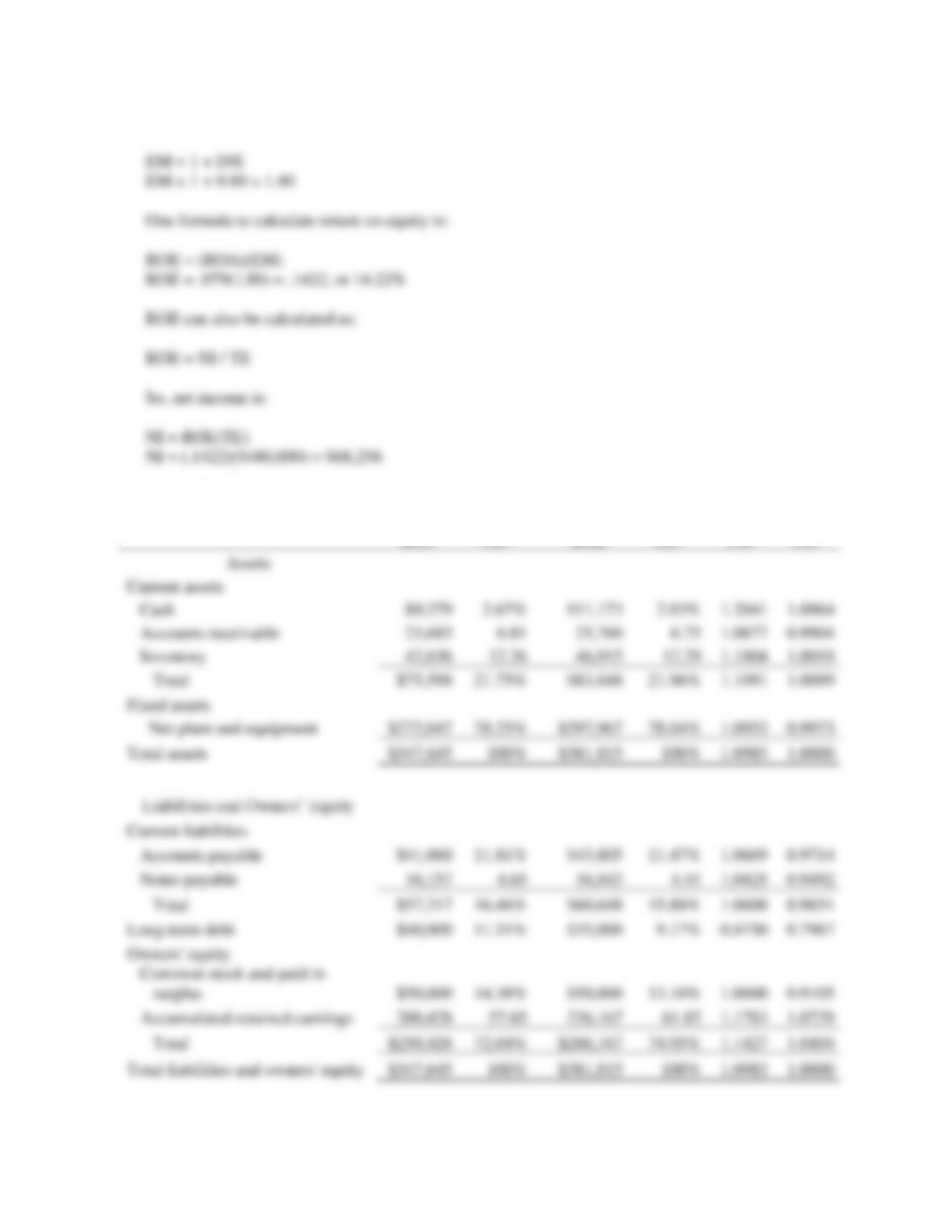

8. This question gives all of the necessary ratios for the DuPont Identity except the equity multiplier, so,

using the DuPont Identity:

11. First, we need the enterprise value, which is:

CHAPTER 3 - 6

12. The equity multiplier is:

13. through 15:

2011

#13

2012

#13

#14

#15

CHAPTER 3 - 7

CHAPTER 3 - 8

Intermediate

18. This is a multistep problem involving several ratios. The ratios given are all part of the DuPont Identity.

CHAPTER 3 - 9

19. This is a multistep problem involving several ratios. It is often easier to look backward to determine

20. The solution to this problem requires a number of steps. First, remember that CA + NFA = TA. So, if

we find the CA and the TA, we can solve for NFA. Using the numbers given for the current ratio and

the current liabilities, we solve for CA:

CHAPTER 3 - 10

Substituting the total equity into the equation and solving for long-term debt gives the following:

22. The solution requires substituting two ratios into a third ratio. Rearranging D/TA:

CHAPTER 3 - 11

23. This problem requires you to work backward through the income statement. First, recognize that

24. The only ratio given that includes cost of goods sold is the inventory turnover ratio, so it is the last

ratio used. Since current liabilities is given, we start with the current ratio:

26. Short-term solvency ratios:

CHAPTER 3 - 12

27. The DuPont identity is:

CHAPTER 3 - 13

28. SMOLIRA GOLF CORP.

Statement of Cash Flows

For 2012

CHAPTER 3 - 14

30. First, we will find the market value of the company’s equity, which is:

Using the book value of debt implicitly assumes that the book value of debt is equal to the market