Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Fraud, Internal Control, and Cash

FOR INSTRUCTOR USE ONLY

7-41

*199. A petty cash fund should be replenished

a. every day.

b. at the end of every accounting period.

c. once a year.

d. as soon as an expense is paid from the fund.

*200. Entries are made to the Petty Cash account when

a. establishing the fund.

b. making payments out of the fund.

c. recording shortages in the fund.

d. replenishing the fund.

Answers to Multiple Choice Questions

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

7-42

BRIEF EXERCISES

Be. 201

Below are descriptions of internal control problems. In the space to the left of each item, enter the

code letter of the one best internal control principle that is related to the problem described.

Internal Control Principles

A. Establishment of responsibility

B. Segregation of duties

C. Physical control devices

D. Documentation procedures

E. Independent internal verification

F. Human resource controls

____ 1. The same person opens incoming mail and posts the accounts receivable subsidiary

ledger.

____ 2. Three people handle cash sales from the same cash register drawer.

____ 3. A clothing store is experiencing a high level of inventory shortages because people try

on clothing and walk out of the store without paying for the merchandise.

____ 4. The person who is authorized to sign checks approves purchase orders for payment.

____ 5. Some cash payments are not recorded because checks are not prenumbered.

____ 6. Cash shortages are not discovered because there are no daily cash counts by

supervisors.

____ 7. The treasurer of the company has not taken a vacation for over 20 years.

Fraud, Internal Control, and Cash

7-43

Solution 201 (5 min.)

Be. 202

Indicate whether each of the business practices listed below strengthens (S) or weakens (W) a

company’s system of internal control.

____ a. Cashiers are not bonded.

____ b. All payments are made with checks.

____ c. Discouraging employees from taking paid vacations.

____ d. Two people handle cash sales from the same cash register drawer.

____ e. Using prenumbered sales tickets.

Be. 203

Identify the internal control procedures applicable to cash receipts for Colorado Company in each

of the following situations.

1. All cashiers are bonded.

2. The treasurer compares the total cash receipts to the bank deposit daily.

3. The bookkeeper records cash receipts which are held by the treasurer.

4. Only the treasurer holds cash receipts.

5. Deposit slips are completed for each deposit.

Be. 204

Identify the internal control procedures applicable to cash disbursements followed by Tolan

Company in each of the following cases.

1. Company checks are pre-numbered.

2. Only the treasurer is authorized to sign checks.

3. Bonding of employees that handle cash.

4. Blank checks are stored in a locked safe.

5. The bookkeeper, not the treasurer, records cash disbursements.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

7-44

Be. 205

Identify whether each of the following items would be (a) added to the book balance, or (b)

deducted from the book balance in a bank reconciliation.

1. EFT transfer to a supplier.

2. Bank service charge.

3. Check printing charge.

4. Error recording check # 214 which was written for $230 but recorded for $320.

5. Collection of note and interest by bank on company’s behalf.

Be. 206

Identify which of the following reconciling items would require an adjusting entry to be made by

Costello Company.

1. Deposits in transit totaled $2,000.

2. A check written to the company for $350 by Grover Company was returned NSF.

3. The bank charged the company $46 for printing checks.

4. Outstanding checks totaled $1,667.

5. A debit memorandum reported an EFT of $178 to Paco Utilities.

Be. 207

Foyle Company needs to make adjusting entries for each of the following reconciling items.

Identify the account to be debited and the account to be credited in each case.

1. A check for $59 written to the company by J. Hammond was returned NSF.

2. The monthly service charge by the bank was $34.

3. The bank collected a $1,000 note plus interest of $60 on the company’s

behalf. The company had not accrued the interest.

Fraud, Internal Control, and Cash

FOR INSTRUCTOR USE ONLY

7-45

Be. 208

The following reconciling items are applicable to the bank reconciliation for the Gunselman

Company. Indicate how each item should be shown on a bank reconciliation.

a. Outstanding checks.

b. Bank credit memorandum for collecting a note for the depositor.

c. Bank debit memorandum for service charge.

d. Deposit in transit.

Be. 209

At August 31 Kiner Company has this bank information: cash balance per bank $9,450;

outstanding checks $762; deposits in transit $1,700; and a bank service charge $20. Determine

the adjusted cash balance per bank at August 31, 2014.

Be. 210

Given the following information, determine the adjusted cash balance per books;

Balance per books as of June 30 $8,800

Outstanding checks $600

NSF check returned with bank statement $130

Deposit mailed the afternoon of June 30 $300

Check printing charges $30

Interest earned on checking account $40

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

7-46

Be. 211

The following information is available for Nichols Company for the month of February: expected

cash receipts $40,000; expected cash disbursements $44,000; cash balance February 1,

$11,000. Management wishes to maintain a minimum cash balance of $10,000. Prepare a basic

cash budget for the month of February.

Exercises

Ex. 212

Jim Gant has worked for Dr. Ken Flood for several years. Jim demonstrates a loyalty that is rare

among employees. He hasn't taken a vacation in the last three years. One of Jim's primary duties

at the medical office is to open the mail and list the checks received. He also takes cash from

patients at the cashier window as patients leave. At times it is so hectic that Jim doesn't bother

with giving patients a receipt for the cash paid on their accounts. He assures them he will see to it

that they receive the proper credit. When the traffic is slow in the office Jim offers to help Lisa

post the payments to the patients' accounts receivable. She is always happy to receive his help,

because he is a very conscientious worker.

Instructions

Identify any principles of internal control that may be violated in this medical office situation.

Ans: N/A, LO: 2, Bloom: C, Difficulty: Easy, Min: 10, AACSB: Communication, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Risk Analysis,

AICPA PC: Communication, IMA: Internal Controls

Fraud, Internal Control, and Cash

FOR INSTRUCTOR USE ONLY

7-47

Ex. 213

Listed below are seven errors or problems that might occur in the processing of cash

transactions. Also shown is a list of internal control principles. Evaluate each possible error and

cite a principle that is listed that would reduce the probability of the error occurring. If none of the

principles given will correct the problem, write "None." If you think more than one principle is

appropriate, list all principles that apply.

Possible Errors or Problems

1. An employee steals the cash collected from a customer for an account receivable and

conceals this theft by issuing a credit memorandum indicating that the customer returned the

merchandise.

2. A small fire destroys 3 days of cash receipts.

3. The official designated to sign checks is able to steal blank checks and issue them without

fear of detection.

4. A salesclerk in serving customers often rings up a sale for less than the actual amount and

then keeps the additional cash collected from the customer.

5. Three cashiers use one cash register drawer and the cash in the drawer is often short of the

balance kept on hand.

6. Each cashier counts his own register drawer each day and verbally reports the results to the

supervisor.

7. Cashiers with over 5-years experience are not bonded.

Internal Control Principles

a. Establishment of responsibility

b. Segregation of duties

c. Physical control devices

d. Documentation procedures

e. Independent internal verification

f. Human resource controls

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

7-48

Ex. 214

Using the following information, prepare a bank reconciliation for Hintz Company for July 31,

2014.

a. The bank statement balance is $3,506.

b. The cash account balance is $3,930

c. Outstanding checks totaled $1,285.

d. Deposits in transit are $1,670.

e. The bank service charge is $30.

f. A check for $98 for supplies was recorded as $89 in the ledger.

Ex. 215

Using the following information, prepare a bank reconciliation for Munoz Company for May 31,

2014.

a. The bank statement balance is $8,300.

b. The cash account balance is $6,562

c. Outstanding checks totaled $1,950.

d. Deposits in transit are $600.

e. The bank service charge is $12.

f. Collection of note by bank, $400.

Ans: N/A, LO: 5, Bloom: AP, Difficulty: Medium, Min: 10, AACSB: Analytic, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA PC:

Problem Solving, IMA: Reporting

Fraud, Internal Control, and Cash

FOR INSTRUCTOR USE ONLY

7-49

Ex. 216

Using the following information, prepare a bank reconciliation for Hammond Company for June

30, 2014.

a. The bank statement balance is $7,650.

b. The cash account balance is $6,422

c. Outstanding checks totaled $1,650.

d. Deposits in transit are $900.

e. The bank service charge is $22.

f. Collection of note by bank, $500.

Ans: N/A, LO: 5, Bloom: AP, Difficulty: Medium, Min: 10, AACSB: Analytic, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA PC:

Problem Solving, IMA: Reporting

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

7-50

Ex. 217

The Hartman Boat Company's bank statement for the month of November showed a balance per

bank of $7,000. The company's Cash account in the general ledger had a balance of $5,659 at

November 30. Other information is as follows:

(1) Cash receipts for November 30 recorded on the company's books were $6,000 but this

amount does not appear on the bank statement.

(2) The bank statement shows a debit memorandum for $40 for check printing charges.

(3) Check No. 119 payable to Maris Company was recorded in the cash payments journal and

cleared the bank for $248. A review of the accounts payable subsidiary ledger shows a $36 credit

balance in the account of Maris Company and that the payment to them should have been for

$284.

(4) The total amount of checks still outstanding at November 30 amounted to $5,800.

(5) Check No. 138 was correctly written and paid by the bank for $409. The cash payment

journal reflects an entry for Check No. 138 as a debit to Accounts Payable and a credit to

Cash in Bank for $490.

(6) The bank returned an NSF check from a customer for $560.

(7) The bank included a credit memorandum for $2,060 which represents collection of a

customer's note by the bank for the company; principal amount of the note was $2,000 and

interest was $60. Interest has not been accrued.

Instructions

(a) Prepare a bank reconciliation for the Hartman Boat Company at November 30.

(b) Prepare any adjusting entries necessary as a result of the bank reconciliation.

Fraud, Internal Control, and Cash

7-51

Solution 217 (Cont.)

Ex. 218

The bank statement for Cates Company indicates a balance of $1,730 on June 30. The cash

balance per books had a balance of $799 on this date. The following information pertains to the

bank transactions for the company.

1. Deposit of $760, representing cash receipts of June 30, did not appear on the bank

statement.

2. Outstanding checks totaled $340.

3. Bank service charges for June amounted to $25

4. The bank collected a note receivable for the company for $1,400 plus $56 interest revenue.

5. An NSF check for $80 from a customer was returned with the statement.

Instructions

a. Prepare a bank reconciliation for June 30.

b. Prepare any adjusting entries necessary as a result of the bank reconciliation.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

7-52

Ex. 219

The bank statement for Adcock Company indicates a balance of $830 on July 31. The cash

balance per books had a balance of $390 on this date. The following information pertains to the

bank transactions for the company.

1. Deposit of $840, representing cash receipts of July 31, did not appear on the bank statement.

2. Outstanding checks totaled $390.

3. Bank service charges for June amounted to $30.

4. The bank collected a note receivable for the company for $1,200 plus $48 interest revenue.

5. A NSF check for $328 from a customer was returned with the statement.

Instructions

a. Prepare a bank reconciliation for July 31.

b. Prepare any adjusting entries necessary as a result of the bank reconciliation.

Fraud, Internal Control, and Cash

FOR INSTRUCTOR USE ONLY

7-53

Ex. 220

Grier Food Store used the following information in recording its bank reconciliation for the month

of April.

Balance per books April 30 $ 905

Balance per bank statement April 30 $11,300

___________________________________________________________________________

(1) Checks written in April but still outstanding $6,300.

(2) Checks written in March but still outstanding $2,800.

(3) Deposits of April 30 not yet recorded by bank $4,900.

(4) NSF check of customer returned by bank $500.

(5) Check No. 210 for $594 was correctly issued and paid by bank but incorrectly entered in the

cash payments journal as payment on account for $549.

(6) Bank service charge for April was $40.

(7) A payment on account was incorrectly entered in the cash payments journal and posted to

the accounts payable subsidiary ledger for $824 when Check No. 318 was correctly

prepared for $284. The check cleared the bank in April.

(8) The bank collected a note receivable for the company of $6,000 plus $240 interest revenue.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

7-54

Ex. 220 (Cont.)

Instructions

Prepare a bank reconciliation at April 30.

Ans: N/A, LO: 5, Bloom: AP, Difficulty: Medium, Min: 20, AACSB: Analytic, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA PC:

Problem Solving, IMA: Reporting

Solution 220 (20 min.)

Ex. 221

Using the code letters below, indicate how each of the items listed would be handled in preparing

a bank reconciliation. Enter the appropriate code letter in the space to the left of each item.

Code

A Add to cash balance per books

B Deduct from cash balance per books

C Add to cash balance per bank

D Deduct from cash balance per bank

E Does not affect the bank reconciliation

Items:

____ 1. Outstanding checks

____ 2. Bank service charge

____ 3. Check for $320 correctly written and paid by the bank but incorrectly entered in the

cash payments journal for $230

____ 4. Deposit in transit

____ 5. Bank returns customer deposited check marked NSF

____ 6. Bank collects notes receivable and interest for depositor

____ 7. Bank debit memorandum for check printing fees

____ 8. Petty cash custodian has $86 in paid petty cash vouchers that have not been

reimbursed.

Fraud, Internal Control, and Cash

FOR INSTRUCTOR USE ONLY

7-55

Ex. 221 (Cont.)

____ 9. Bank charged a check against the company, which should have been charged to

another company.

____ 10. A check for $236 was correctly paid by the bank but was incorrectly entered in the

cash payments journal for $263

Ex. 222

The cash balance per books for Wellmeyer Company on November 30, 2014, is $10,740.93. The

following checks and receipts were recorded for the month of December 2014:

Checks Receipts

No. Amount No. Amount Amount Date

17 $372.96 22 $ 578.84 $ 843.86 12/5

18 780.62 23 1,687.50 941.54 12/21

19 157.00 24 921.30 808.58 12/27

20 587.50 25 246.03 1,367.00 12/31

21 234.15

In addition, the bank statement for the month of December is presented below:

Balance Deposits and Credits Checks and Debits Balance

Last Statement No. Total Amount No. Total Amount This Statement

$5,404.84 5 $9,578.36 10 $3,632.19 $11,351.01

________________________________________________________________________

Checks and other debits Deposits Date Balance

_________________________________________

No. Amount No. Amount No. Amount

________________________________________________________________________

14 148.29 17 372.96 22 578.84 5,484.38 12/1 $9,875.13

18 708.62 24 921.30 843.86 12/8 $9,219.03

19 157.00 25 246.03 941.54 12/23 $9,541.58

21 234.15 15.00 SC 808.58 12/29 $10,101.01

250.00 NSF 1,500.00 CM 12/31 $11,351.01

________________________________________________________________________

Symbols: NSF (Not sufficient funds) SC (Service charge) CM (Credit Memo)

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

7-56

Ex. 222 (Cont.)

Check No. 18 was correctly written for $708.62 for a payment on account. The NSF check was

from S. Gill, a customer, in settlement of an account receivable. An entry has not been made for

the NSF check. The credit memo is for the collection of a note receivable including interest of $60

that has not been accrued. The bank service charge is $15.00.

Instructions

(a) Prepare a bank reconciliation at December 31.

(b) Prepare the adjusting journal entries required by the bank reconciliation.

Fraud, Internal Control, and Cash

7-57

Solution 222 (Cont.)

Ex. 223

Seaver Company received a notice with its bank statement that the bank had collected a note

receivable for $18,000 plus $600 of interest. The bank had credited these amounts to Seaver's

account less a collection fee of $30. Seaver Company had already accrued the interest for this

note on its books.

(a) How will these items affect Seaver Company's bank reconciliation?

(b) Prepare the journal entry that Seaver Company will make to record this information on its

books.

Ex. 224

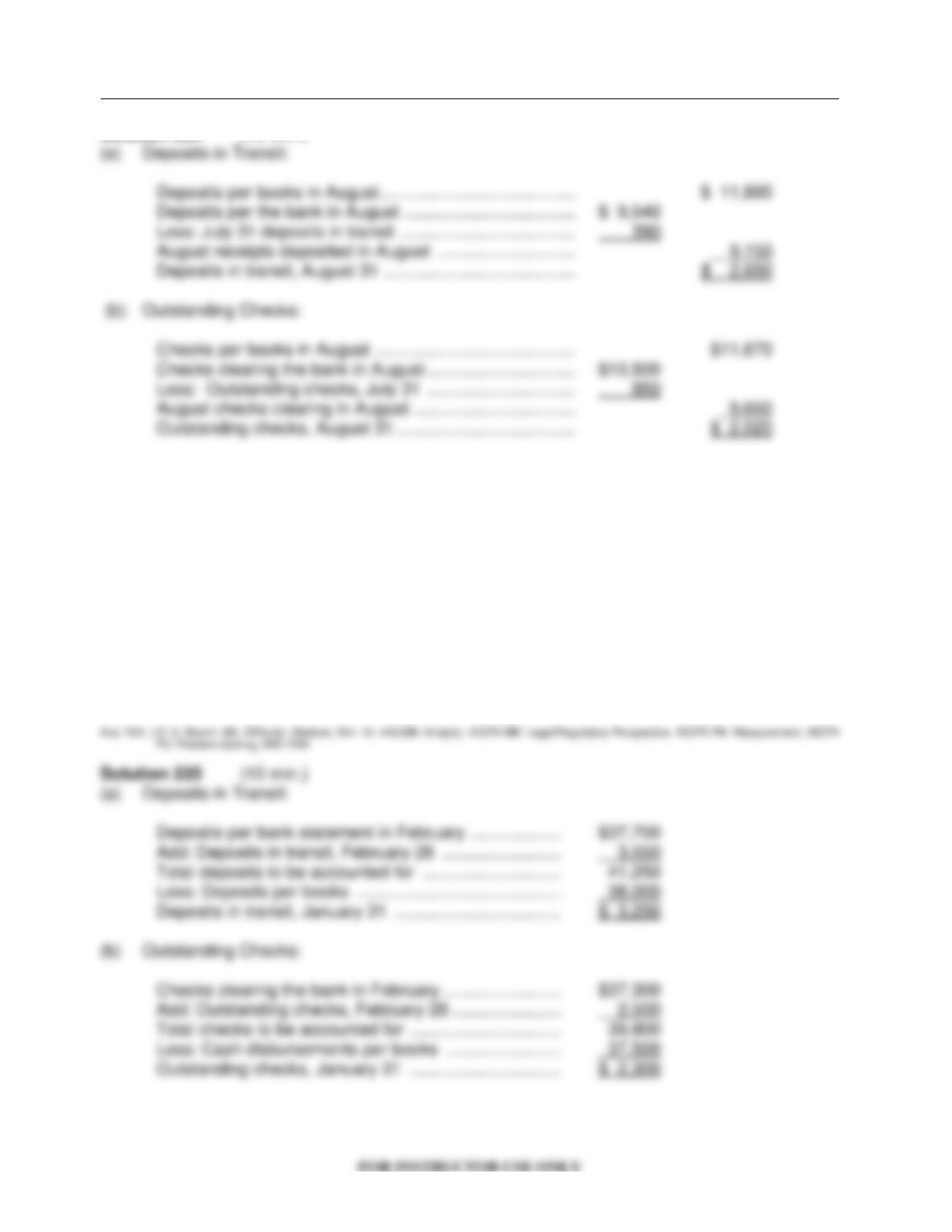

The cash records of the Dillon Company show the following:

1. The July 31 bank reconciliation indicated that deposits in transit totaled $390. During August

the general ledger account, Cash shows deposits of $11,800, but the bank statement

indicates that only $9,540 in deposits were received during the month.

2. The July 31 bank reconciliation also reported outstanding checks of $850. During the month

of August, the Dillon Company books show that $11,670 of checks were issued, yet the bank

statement showed that $10,500 of checks cleared the bank in August.

There were no bank debit or credit memoranda and no errors were made by either the bank or

the Dillon Company.

Answer the following questions:

(a) What were the deposits in transit at August 31?

(b) What were the outstanding checks at August 31?

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

7-58

Solution 224 (10 min.)

Ex. 225

The cash records of Grayson Company show the following:

1. In February, deposits per the bank statement totaled $37,700; deposits per books $38,000;

and deposits in transit at February 28 were $3,550.

2. In February cash disbursements per books were $37,500; checks clearing the bank were

$37,300; and outstanding checks at February 28 were $2,500.

There were no bank debit or credit memoranda and no errors were made by either the bank or

Grayson Company.

Answer the following questions:

(a) What were the deposits in transit at January 31?

(b) What were the outstanding checks at January 31?

Fraud, Internal Control, and Cash

FOR INSTRUCTOR USE ONLY

7-59

Ex. 226

Listed below are items that may be useful in preparing the March 2014, bank reconciliation for the

Carrinton Machine Works.

Using the code letters below, insert in the space before each item the letter where the amount

would be located or otherwise treated in the bank reconciliation process.

Code Located or Treated

A Add to the cash balance per books

B Deduct from the cash balance per books

C Add to the cash balance per bank

D Deduct from the cash balance per bank

E Does not affect the bank reconciliation

____ 1. Included with the bank statement materials was a check from Joe Terrell for $40

stamped "account closed”.

____ 2. A personal deposit by Ron Carrinton to his personal account in the amount of $300 for

dividends on his General Electric common stock was credited to the company account.

____ 3. The bank statement included a debit memorandum for $22.00 for four books of blank

checks for Carrinton Machine Works.

____ 4. The bank statement contains a credit memorandum for $42.75 interest on the average

checking account balance.

____ 5. The daily deposits of March 30 and March 31 for $3,362 and $3,125, respectively,

were not included in the bank statement postings.

____ 6. Two checks totaling $316.86, which were outstanding at the end of February, cleared

in March and were returned with the March statement.

____ 7. The bank statement included a credit memorandum dated March 28, 2014, for $62.00

for the monthly interest on a 6-month, $15,000 certificate of deposit that the company

owns.

____ 8. Four checks, #8712, #8716, #8718, #8719, totaling $5,369.65, did not clear the bank

during March.

____ 9. On March 24, 2014, Carrinton Machine Works delivered to the bank for collection a

$3,400, 3-month note from Tom Jacobs. A credit memorandum dated March 29, 2014,

indicated the collection of the note and $102.00 of interest.

____ 10. The bank statement included a debit memorandum for $20.00 for the collection

service on the above note and interest.

Ans: N/A, LO: 5, Bloom: C, Difficulty: Medium, Min: 10, AACSB: Analytic, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Measurement, AICPA

PC: Problem Solving, IMA: FSA

Solution 226 (10 min.)

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

7-60

Ex. 227

On April 30, the bank reconciliation of Baxter Company shows three outstanding checks: no. 354,

$650, no. 355, $920, and no. 357, $615. The May bank statement and the May cash payments

journal show the following.

Bank Statement

Cash Payments Journal

Checks Paid

Checks Paid

Date

Check No.

Amount

Date

Check No.

Amount

5/4

354

650

5/2

358

159

5/2

357

615

5/5

359

275

5/17

358

159

5/10

360

890

5/12

359

275

5/15

361

800

5/20

360

890

5/22

362

750

5/29

363

480

5/24

363

480

5/30

362

750

5/29

364

840

Instructions

Using step 2 in the reconciliation procedure, list the outstanding checks at May 31.

Ans: N/A, LO: 5, Bloom: AP, Difficulty: Medium, Min: 3, AACSB: Analytic, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Measurement, AICPA

PC: Problem Solving, IMA: FSA

Ex. 228

The information below relates to the Cash account in the ledger of Remington Company.

Balance September 1—$25,720 Cash deposited—$96,000.

Balance September 30—$26,100 Checks written—$95,620.

The September bank statement shows a balance of $24,635 on September 30 and the following

memoranda.

Credits

Debits

Collection of $3,750 note plus interest $50

$3,800

NSF check: J. E. Hoover

$635

Interest earned on checking account

$65

Safety deposit box rent

$75

At September 30, deposits in transit were $7,195, and outstanding checks totaled $2,575.

Instructions

Prepare the bank reconciliation at September 30.