Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

16 - 56

Solution 176 (Cont.)

Ex. 177

The Polishing Department of Estaban Company has the following production and manufacturing

cost data for September. Materials are entered at the beginning of the process.

Production: Beginning inventory 2,000 units that are 100% complete as to materials and 30%

complete as to conversion costs; units started during the period are 38,000, ending inventory of

6,000 units 10% complete as to conversion costs.

Manufacturing costs: Beginning inventory costs, comprised of $18,000 of materials and

$13,000 of conversion costs; materials costs added in Polishing during the month, $202,000

labor and overhead applied in Polishing during the month $176,200 and $312,500 respectively.

Instructions

(a) Compute the equivalent units of productions for materials and conversion costs for the

month of September.

(b) Compute the unit costs for materials and conversion costs for the month.

(c) Determine the costs to be assigned to the units transferred out and in process.

Process Costing

16 - 57

Solution 177 (Cont.)

Ex. 178

Grey Building Supplies' total materials costs are $40,000 and total conversion costs are $33,000.

Equivalent units of production for materials are 10,000, and 6,000 for conversion costs.

Instructions

Compute the unit costs for materials, conversion costs, and total manufacturing costs for the

month.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

16 - 58

Ex. 179

Glazer, Inc. has the following production data for June:

Transferred out 50,000 units

Ending work in process 5,000 units

The units in work in process are 100% complete for materials and 60% complete for conversion

costs. Materials costs are $4 per unit and conversion costs are $9 per unit.

Instructions

Determine the costs to be assigned to the units transferred out and the units in ending work in

process.

Ex. 180

Production costs chargeable to the Sanding Department in July in Magnum Company are

$30,000 for materials, $17,000 for labor, and $13,000 for manufacturing overhead. Equivalent

units of production are 25,000 for materials and 15,000 for conversion costs.

Instructions

Compute the unit costs for materials and conversion costs.

Ex. 181

Mayer Company uses a process cost system. The Molding Department adds materials at the

beginning of the process and conversion costs are incurred uniformly throughout the process.

Work in process on May 1 was 75% complete and work in process on May 31 was 40%

complete.

Instructions

Complete the Production Cost Report for the Molding Department for the month of May using the

above information and the information below.

Process Costing

16 - 59

Ex. 181 (cont.)

MAYER COMPANY

Molding Department

Production Cost Report

For the Month Ended May 31, 2013

Equivalent Units

QUANTITIES Physical Units Materials Conversion Costs

Units to be accounted for

Work in process, May 1 8,000

Started into production 27,000

Total units 35,000

Units accounted for

Transferred out 30,000

Work in process, May 31 5,000

Total units 35,000

COSTS

Unit costs Materials Conversion Costs Total

Costs in May $140,000 $160,000 $300,000

Equivalent units

Unit costs $ $ $

Costs to be accounted for

Work in process, May 1 $ 60,000

Started into production 240,000

Total costs $300,000

Cost Reconciliation Schedule

Costs accounted for

Transferred out $

Work in process, May 31

Materials $

Conversion costs

Total costs $300,000

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

16 - 60

Solution 181 (12–16 min.)

Ex. 182

Baker Winery manufactures a fine wine in two departments, Fermenting and Bottling. In the

Fermenting Department, grapes are aged in casks for a period of 30 days. In the Bottling

Department, the wine is bottled and then sent to the finished goods warehouse. Labor and

overhead are incurred uniformly through both processes. Materials are entered at the beginning

of both processes. Cost and production data for the Fermenting Department for December 2013

are presented below:

Cost data

Beginning work in process inventory $ 37,000 ($30,000 of materials cost)

Materials 390,000

Conversion costs 121,000

Total costs $548,000

Process Costing

16 - 61

Ex. 182 (cont.)

Production data

Beginning work in process (gallons) 5,000 (40%)

Gallons started into production 65,000

Ending work in process (gallons) 8,000 (25%)

Instructions

(a) Compute the equivalent units of production.

(b) Determine the unit production costs.

(c) Determine the costs to be assigned to units transferred out and ending work in process.

Ex. 183

The Assembly Department of Nitz Company has the following production and cost data at the end

of May, 2013.

Production: 25,000 units started into production; 20,000 units transferred out and 5,000 units

100% completed as to materials and 40% completed as to conversion costs.

Manufacturing Costs: Materials added at beginning of process, $90,000; labor, $72,000;

overhead $60,000.

Instructions

Prepare a production cost report for the month of May.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

16 - 62

Solution 183 (22–30 min.)

Ex. 184

Romero Company—Perth Division is a new state of the art production facility that manufactures

landing gears for airplanes. The September 30th ending work in process is comprised of labor

and overhead and is approximately 60% complete. All materials are assumed to be 100%

complete. Total materials costs during the period totaled $840,000.

Instructions

As the new plant accountant, you are asked to complete the production cost report which appears

as follows:

Process Costing

16 - 63

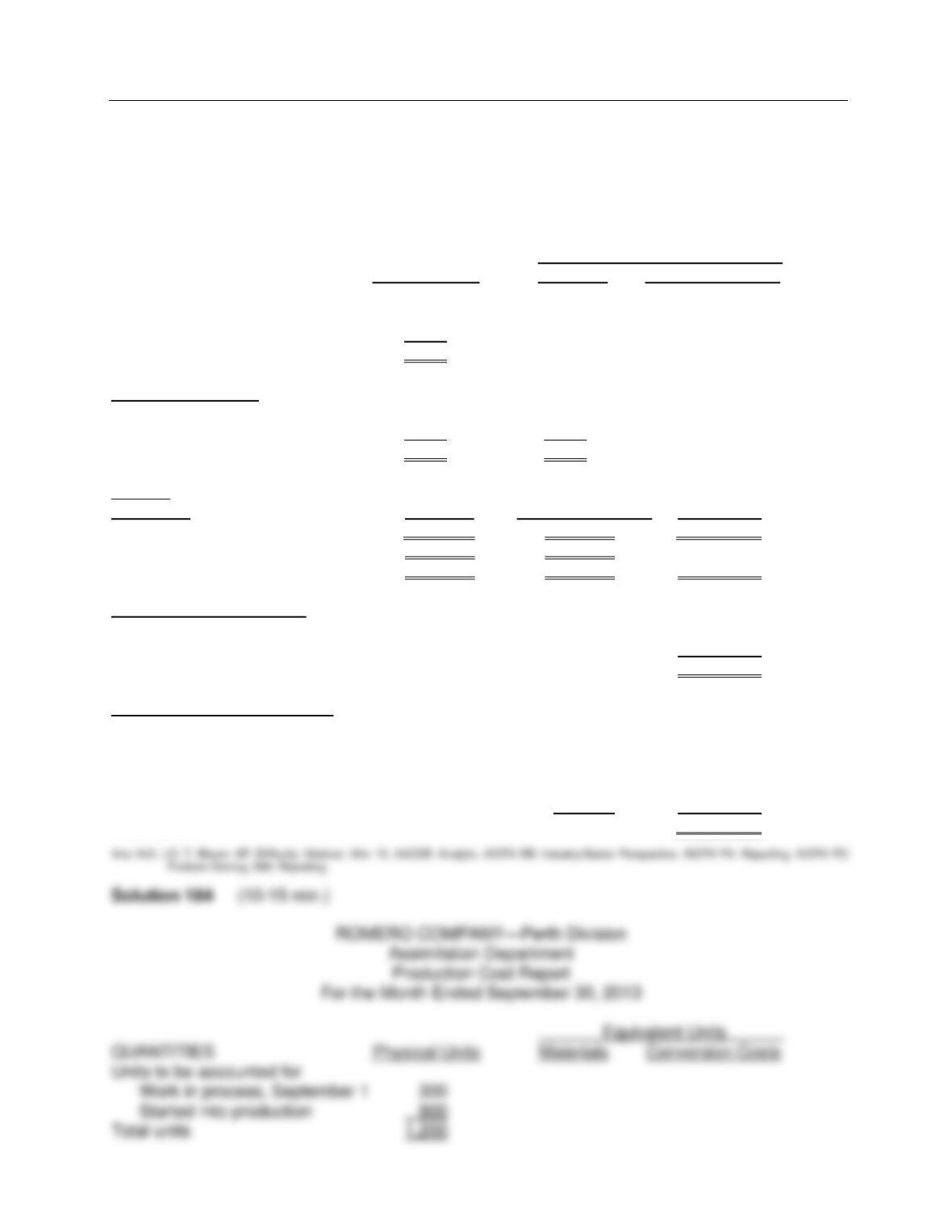

Ex. 184 (cont.)

ROMERO COMPANY—Perth Division

Assimilation Department

Production Cost Report

For the Month Ended September 30, 2013

Equivalent Units

QUANTITIES Physical Units Materials Conversion Costs

Units to be accounted for

Work in process, September 1 300

Started into production 900

Total units 1,200

Units accounted for

Transferred out 700 700 700

Work in process, September 30 500 500

Total units 1,200 1,200

COSTS

Unit Costs Materials Conversion Costs Total

Costs in September $840,000 $ $1,100,000

Equivalent units

Unit costs $ $ 260 $

Costs to be accounted for

Work in process, Sept. 1 $ 243,400

Started into production

Total costs $

Cost Reconciliation Schedule

Costs accounted for

Transferred out $

Work in process, September

Materials $

Conversion costs 78,000

Total costs $1,100,000

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

16 - 64

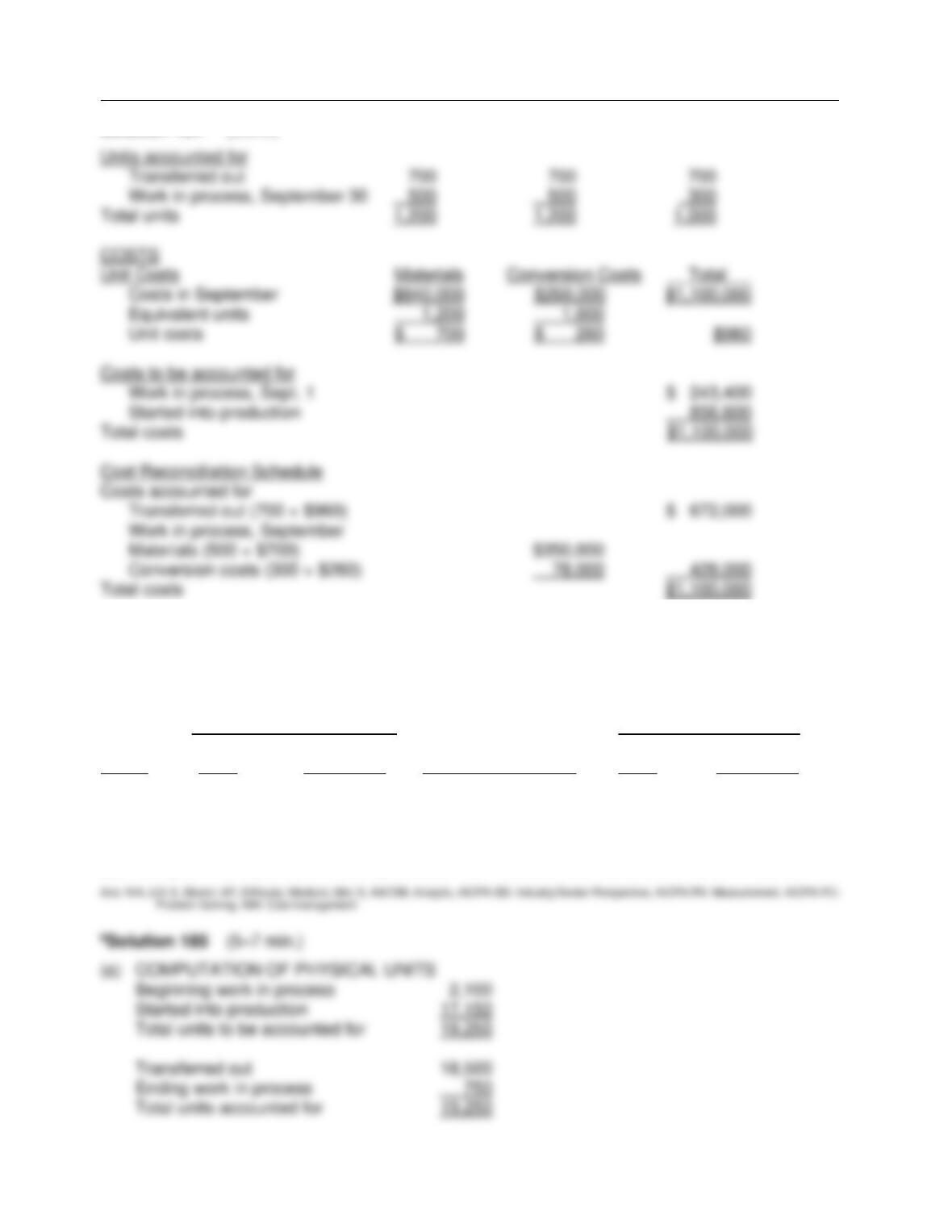

Solution 184 (Cont.)

aEx. 185

At Oxley Company, materials are entered at the beginning of each process. The company uses

the FIFO method for process costing. Work in process inventories, with the percentage of work

done on conversion, and production data for its Finishing Department for March are as follows:

Beginning Work in Process Ending Work in Process

Percentage Units Completed Percentage

Month Units Completed and Transferred Out Units Completed

March 2,100 60% 18,500 750 90%

Instructions

(a) Compute the physical units for March.

(b) Compute the equivalent units of production for materials and conversion costs for March.

Process Costing

16 - 65

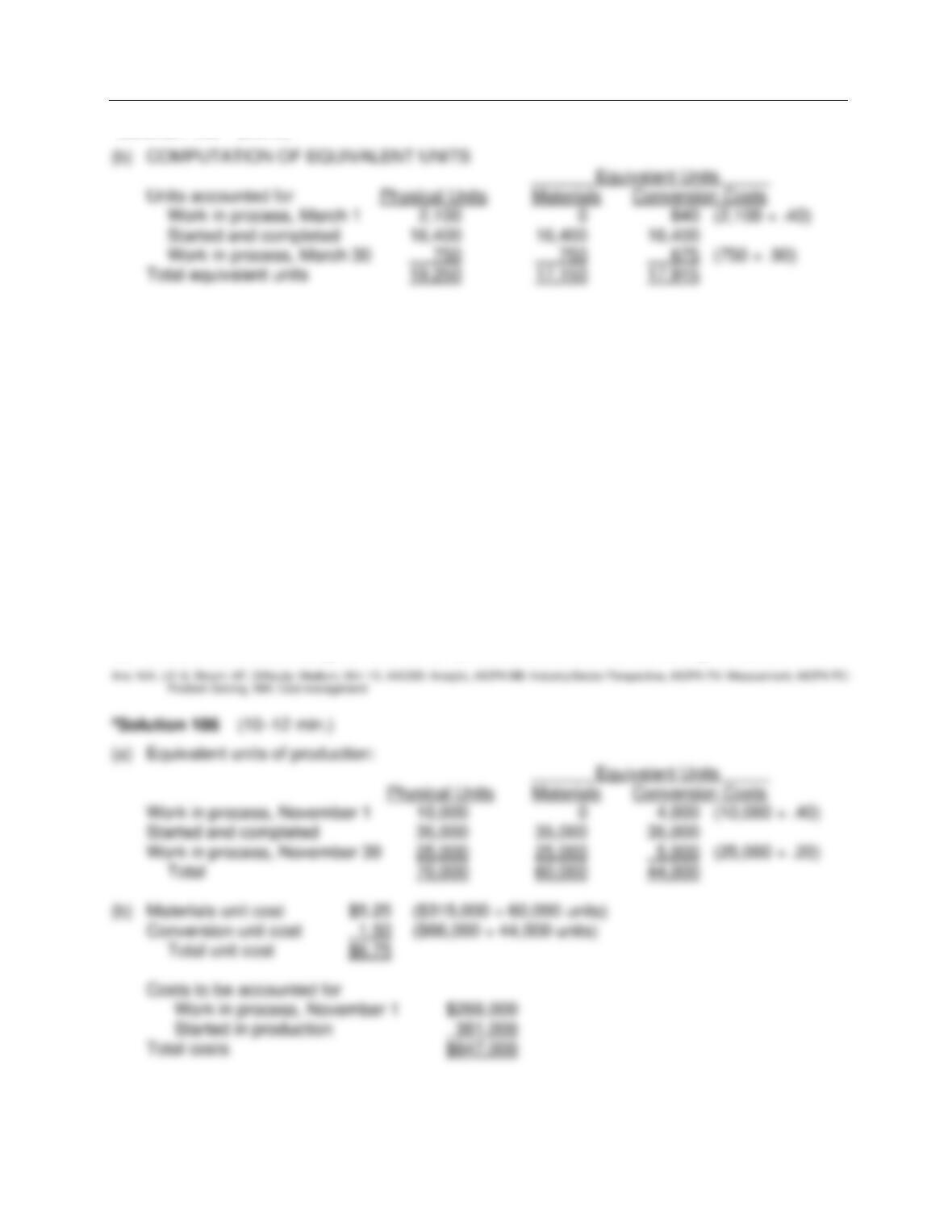

aSolution 185 (Cont.)

aEx. 186

Taco Ranch uses a process cost system and the FIFO cost flow assumption. Production begins

in the Crafting Department where materials are added at the beginning of the process and

conversion costs are incurred uniformly throughout the process. On November 1, the beginning

work in process inventory consisted of 10,000 units, which were 60% complete and had a cost of

$266,000, $140,000 of which were materials costs. During November, the following occurred:

Materials added $315,000

Conversion costs incurred $66,000

Units completed and transferred out in November 45,000

Units in ending work in process November 30 (20% complete) 25,000

Instructions

Answer the following questions and show the computations that support your answers:

(a) What are the equivalent units of production for materials and conversion costs in the Crafting

Department for the month of November?

(b) What are the costs assigned to the ending work in process inventory on November 30?

(c) What are the costs assigned to units completed and transferred out during November?

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

16 - 66

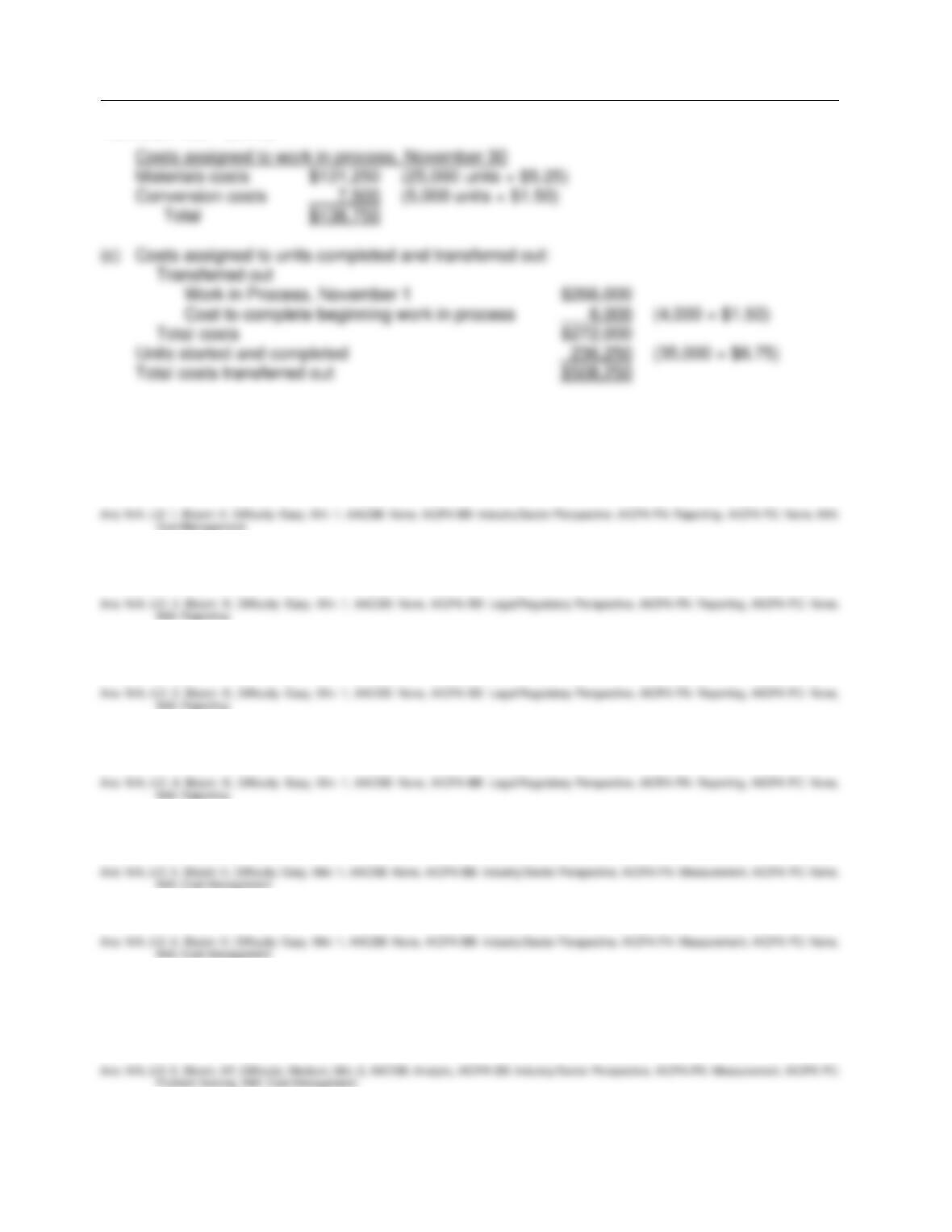

aSolution 186 (cont.)

COMPLETION STATEMENTS

187. Process cost systems are used to apply costs to similar products that are ____________

in a ____________ fashion.

188. Separate _________________ accounts are maintained for each production department

or manufacturing process in a process cost system.

189. In a process cost system, manufacturing costs are summarized in a ________________

report for each department.

190. A primary driver of overhead costs in continuous manufacturing operations is

_______________.

191. Equivalent units of production measure the work done during the period, expressed in fully

________________ units.

192. Unit production costs are expressed in terms of _____________ units of production.

193. If a processing department has 27,000 units in process at the beginning of the period,

completes and transfers out 90,000 and has 18,000 units in process at the end of the

period, then the number of units started into production during the period was

______________ units.

194. A cost reconciliation schedule is prepared to assign total costs to units ______________,

and to the units in the _________________ work in process.

195. The production cost report is an internal document that shows production quantity and

______________ for a production department.

Answers to Completion Statements

MATCHING

196. Match the items in the two columns below by entering the appropriate code letter in the

space provided.

A. Total manufacturing cost per unit E. Cost reconciliation schedule

B. Equivalent units of production F. Units transferred out

C. Total units accounted for G. Unit production costs

D. Production cost report H. Physical units

____ 1. A summary of both production quantity and cost data for a production department.

____ 2. Shows that the total costs accounted for equal the total costs to be accounted for.

____ 3. Work done during a period expressed in fully completed units.

____ 4. Costs expressed in terms of equivalent units of production.

____ 5. Actual units to be accounted for during a period, irrespective of any work performed.

____ 6. Units transferred out during the period plus units in ending work in process.

____ 7. Unit materials costs plus unit conversion costs.

____ 8. Total units accounted for minus units in ending work in process.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

16 - 68

SHORT-ANSWER ESSAY QUESTIONS

S-A E 197

Why do some companies need a cost accounting system while others do not? What are the

determining characteristics or factors that influence the type of cost accounting system that is

appropriate for a company?

S-A E 198

The production cost report summarizes the activities that have taken place in a department or

process over a period of time. Identify the major types of information found on a production cost

report, and indicate who in the business organization uses this type of information and for what

purpose the information is used.

S-A E 199

Your roommate is curious about the features of process cost accounting. Identify and explain the

distinctive features for your roommate.

Process Costing

16 - 69

S-A E 200

What purposes are served by a production cost report?

S-A E 201 (Ethics)

Dolly's Dream Homes, Inc. manufactures doll houses in a continuous process. Various

customizing features and furnishings are added at the end of the process to create the various

models that are sold. The basic design and floor plans of all the houses are identical, however.

During the most recent month, the lumber used in trimming the houses was inadvertently

recorded as direct materials. At month end, when the error was discovered, Susie Rief, the

accountant, was told by the accounting manager, Karen Tate, not to bother with correcting the

error, because the dollar amount of the error was not "worth it." Susie believes that the dollar

amount is not as important as the quality of the reports. She wonders whether she would be

committing an unethical act if she were to make the changes anyway, despite her superior's

telling her not to.

Required:

1. Who are the stakeholders in this situation?

2. Was it unethical for the company to ask that the error not be corrected? Explain briefly.

3. Would it be unethical for Susie to correct the error? Explain briefly.