Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Financial Analysis: The Big Picture

FOR INSTRUCTOR USE ONLY

13-79

Ex. 252 (Cont.)

Additional information:

1. Common stock outstanding January 1, 2014, was 30,000 shares, and 40,000 shares were

outstanding at December 31, 2014.

2. The market price of Gillman, Inc., stock was $15.86 in 2014.

3. Cash dividends of $16,000 were paid, $4,500 of which were to preferred stockholders.

Instructions

Compute the following measures for 2014.

(a) Earnings per share.

(b) Price-earnings ratio.

(c) Payout ratio.

(d) Times interest earned.

Ans: N/A, LO: 6, 8, Bloom: AP, Difficulty: Hard, Min: 10, AACSB: Analytic, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA PC:

Problem Solving, IMA: Performance Measurement

Solution 252 (10 min.)

Ex. 253

Belcanto Corporation experienced a fire on December 31, 2014, in which its financial records were

partially destroyed. It has been able to salvage some of the records and has ascertained the

following balances.

December 31, 2014 December 31, 2013

Cash $ 40,000 $ 15,000

Accounts receivable (net) 84,000 126,000

Inventory 200,000 180,000

Accounts payable 50,000 10,000

Notes payable 30,000 20,000

Common stock, $100 par 400,000 400,000

Retained earnings 170,000 101,000

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

13-80

Ex. 253 (Cont.)

Additional information:

1. The inventory turnover is 4.2 times

2. The return on common stockholders' equity is 14%. The company had no additional paid-in-

capital.

3. The accounts receivable turnover is 10.2 times.

4. The return on assets is 12.5%.

5. Total assets, Dec. 31, 2013 = 604,750.

Instructions

Compute the following values for 2014.

(a) Cost of goods sold.

(b) Net credit sales.

(c) Net income.

(d) Total assets.

Ans: N/A, LO: 6, 8, Bloom: AN, Difficulty: Hard, Min: 25, AACSB: Analytic, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA PC:

Problem Solving, IMA: Reporting

Solution 253 (25 min.)

Financial Analysis: The Big Picture

FOR INSTRUCTOR USE ONLY

13-81

Solution 253 (Cont.)

Ex. 254

The financial statements of Elcamino Company appear below:

ELCAMINO COMPANY

Comparative Balance Sheet

December 31,

___________________________________________________________________________

Assets 2014 2013

Cash ................................................................................................ $ 25,000 $ 40,000

Debt investments ............................................................................ 20,000 60,000

Accounts receivable (net) ............................................................... 50,000 30,000

Inventory ......................................................................................... 140,000 170,000

Property, plant and equipment (net) ............................................... 170,000 200,000

Total assets ............................................................................... $405,000 $500,000

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

13-82

Ex. 254 (Cont.)

Liabilities and stockholders' equity

Accounts payable ........................................................................... $ 25,000 $ 30,000

Short-term notes payable ............................................................... 40,000 90,000

Bonds payable ................................................................................ 75,000 160,000

Common stock ................................................................................ 160,000 145,000

Retained earnings .......................................................................... 105,000 75,000

Total liabilities and stockholders' equity ..................................... $405,000 $500,000

ELCAMINO COMPANY

Income Statement

For the Year Ended December 31, 2014

Net sales (all on credit) ................................................................... $360,000

Cost of goods sold .......................................................................... 184,000

Gross profit ..................................................................................... 176,000

Expenses

Interest expense ....................................................................... $11,000

Selling expenses ...................................................................... 30,000

Administrative expenses ........................................................... 20,000

Total expenses ................................................................... 61,000

Income before income taxes .......................................................... 115,000

Income tax expense ....................................................................... 35,000

Net income ..................................................................................... $ 80,000

Additional information:

a. Cash dividends of $50,000 were declared and paid on common stock in 2014.

b. Weighted-average number of shares of common stock outstanding during 2014 was 50,000

shares.

c. Market value of common stock on December 31, 2014, was $16 per share.

d. Net cash provided by operating activities for 2014 was $70,000.

Financial Analysis: The Big Picture

FOR INSTRUCTOR USE ONLY

13-83

Ex. 254 (Cont.)

Instructions

Using the financial statements and additional information, compute the following ratios for the

Lewis Company for 2012. Show all computations.

Computations

1. Current ratio _________.

2. Return on common stockholders' equity _________.

3. Price-earnings ratio _________.

4. Inventory turnover _________.

5. Accounts receivable turnover _________.

6. Times interest earned _________.

7. Profit margin _________.

8. Average days in inventory _________.

9. Payout ratio _________.

10. Return on assets _________.

11. Cash debt coverage _________.

Ans: N/A, LO: 6, 8, Bloom: AP, Difficulty: Hard, Min: 15, AACSB: Analytic, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA PC:

Problem Solving, IMA: Performance Measurement

Solution 254 (15-20 min.)

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

13-84

Solution 254 (Cont.)

Ex. 255

The following ratios have been computed for Southern Company for 2014.

Profit margin ratio 20%

Times interest earned 12 times Current ratio 2.5:1

Accounts receivable turnover 5 times Debt to assets ratio 24%

The 2014 financial statements for Southern Company with missing information follows:

SOUTHERN COMPANY

Comparative Balance Sheet

December 31,

——————————————————————————————————————————

Assets

2014 2013

Cash .......................................................................................... $ 25,000 $ 35,000

Debt Investments ........................................................................ 15,000 15,000

Accounts receivable (net) .......................................................... ? (6) 50,000

Inventory .................................................................................... ? (7) 50,000

Property, plant, and equipment (net) ......................................... 200,000 160,000

Total assets ........................................................................ $ ? (8) $310,000

Financial Analysis: The Big Picture

FOR INSTRUCTOR USE ONLY

13-85

Ex. 255 (Cont.)

Liabilities and stockholders' equity

Accounts payable ...................................................................... $ 15,000 $ 25,000

Short-term notes payable .......................................................... 35,000 30,000

Bonds payable .......................................................................... ? (9) 20,000

Common stock .......................................................................... 200,000 200,000

Retained earnings ..................................................................... 47,000 35,000

Total liabilities and stockholders' equity .............................. $ ? (10) $310,000

SOUTHERN COMPANY

Income Statement

For the Year Ended December 31, 2014

——————————————————————————————————————————

Net sales ................................................................................... $200,000

Cost of goods sold .................................................................... 100,000

Gross profit ................................................................................ 100,000

Expenses:

Depreciation expense ......................................................... $ ? (5)

Interest expense .................................................................. 5,000

Selling expenses ................................................................. 10,000

Administrative expenses ..................................................... 15,000

Total expenses .............................................................. ? (4)

Income before income taxes ..................................................... ? (2)

Income tax expense ............................................................ ? (3)

Net income ................................................................................ $ ? (1)

Instructions

Use the above ratios and information from the Southern Company financial statements to fill in the

missing information on the financial statements. Follow the sequence indicated. Show

computations that support your answers.

Ans: N/A, LO: 6, 8, Bloom: AN, Difficulty: Medium, Min: 35, AACSB: Analytic, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA PC:

Problem Solving, IMA: Performance Measurement

Solution 255 (35-40 min.)

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

13-86

Solution 255 (Cont.)

Financial Analysis: The Big Picture

FOR INSTRUCTOR USE ONLY

13-87

Solution 255 (Cont.)

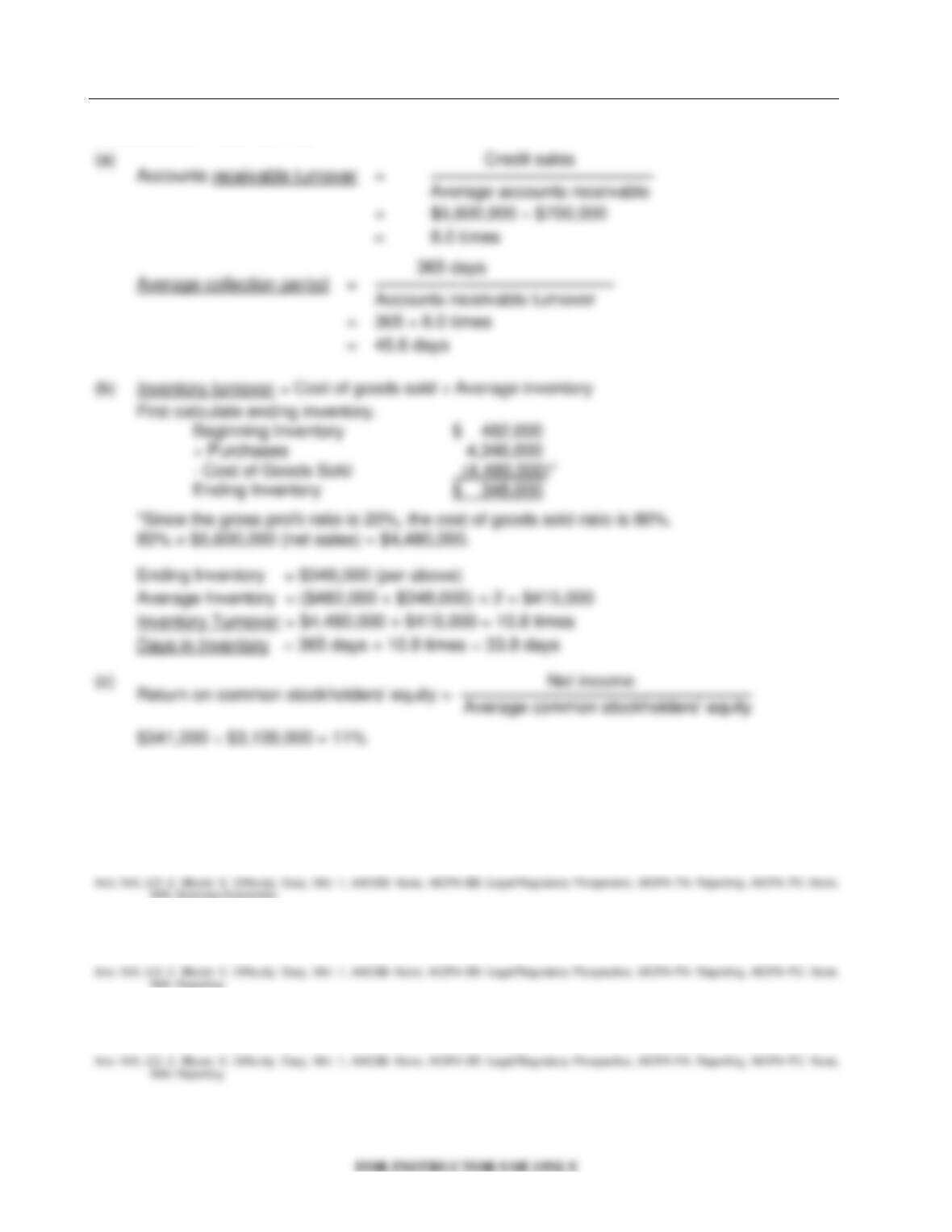

Ex. 256

B. Jones Corporation has issued common stock only. The company has been successful and has

a gross profit rate of 20%. The information shown below was taken from the company's financial

statements.

Beginning inventory $ 482,000

Purchases 4,346,000

Ending inventory ?

Average accounts receivable 700,000

Average common stockholders' equity 3,100,000

Sales revenue (all on credit) 5,600,000

Net income 341,000

Instructions

Compute the following:

(a) Accounts receivable turnover and the average number of days required to collect the

accounts receivable.

(b) The inventory turnover and the average days in inventory.

(c) Return on common stockholders' equity.

Ans: N/A, LO: 6, 8, Bloom: AP, Difficulty: Medium, Min: 13, AACSB: Analytic, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA PC:

Problem Solving, IMA: Performance Measurement

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

13-88

Solution 256 (13-18 min.)

COMPLETION STATEMENTS

257. Discontinued operations refers to the disposal of a __________________ of a business.

258. The two criteria necessary for an item to be classified as an extraordinary item are that the

transaction or event must be (1) _______________ and (2) ________________.

259. A change in depreciation methods during the year would be classified as a change in

____________________.

Financial Analysis: The Big Picture

13-89

260. ______________ analysis, also called trend analysis, is a technique for evaluating a series

of financial statement data over a period of time.

261. Expressing each item in a financial statement as a percent of a base amount is called

______________ analysis.

262. For analysis of the financial statements, ratios can be classified into three types:

(1)_____________ ratios, (2)_____________ ratios, and (3)______________ ratios.

263. The times interest earned is calculated by dividing ___________________ before

__________________ and __________________ by interest expense.

264. The liquidity ratio, known as the _______________ ratio, has a disadvantage that it uses

year-end balances for current assets and current liabilities. The ___________ partially

corrects for this problem by using cash provided by operating activities and average

current liabilities rather than point in time numbers.

265. The accounts receivable turnover is calculated by dividing ________________ by average

___________________.

266. If the inventory turnover is 7.3 times, and the average inventory was $600,000, the cost of

goods sold during the year was $______________ and the average days to sell the

inventory was ______________ days.

267. Hobson Corporation had net sales for the year of $300,000 and average total assets of

$200,000. The asset turnover is ____________ times.

268. The ______________ ratio measures the percentage of earnings distributed in the form of

cash dividends.

269. The lower the _______________ to _______________ ratio, the more equity "buffer" is

available to the creditors if the company becomes insolvent.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

13-90

Answers to Completion Statements

MATCHING

SET A

270. For each of the ratios listed below, indicate by the appropriate code letter, whether it is a

liquidity ratio, a profitability ratio, or a solvency ratio.

Code:

L = Liquidity ratio

P = Profitability ratio

S = Solvency ratio

____ 1. Price-earnings ratio

____ 2. Return on assets

____ 3. Accounts receivable turnover ratio

____ 4. Earnings per share

____ 5. Payout ratio

____ 6. Current cash debt coverage

____ 7. Current ratio

____ 8. Debt to assets ratio

____ 9. Free cash flow

____ 10. Inventory turnover

Financial Analysis: The Big Picture

FOR INSTRUCTOR USE ONLY

13-91

SET B

271. Match the ratios with their formulas by entering the appropriate letter in the space provided.

A. Current ratio F. Times interest earned

B. Current cash debt coverage G. Inventory turnover

C. Profit margin H. Average collection period

D. Asset turnover I. Average days in inventory

E. Price-earnings ratio J. Payout ratio

____ 1.

Cost of goods sold

Average inventory

____ 2.

Net income

Net sales

____ 3.

Cash dividends declared on common stock

Net income

____ 4.

Net sales

Average total assets

____ 5.

Current assets

Current liabilities

____ 6.

365 days

Accounts receivable turnover

____ 7.

Market price per share of stock

Earnings per share

____ 8.

365 days

Inventory turnover

____ 9.

Income before income taxes and interest expense

Interest expense

____ 10.

Net cash provided by operating activities

Average current liabilities

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

13-92

SHORT-ANSWER ESSAY QUESTIONS

S-A E 272

Explain sustainable income. What relationship does this concept have to the treatment of irregular

items on the income statement?

Ans: N/A, LO: 1, Bloom: C, Difficulty: Easy, Min: 5, AACSB: Communications, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA PC:

Communications, IMA: Reporting

Solution 272

S-A E 273

What issues must be considered when determining whether or not a loss from earthquake

destruction should be treated as an extraordinary item?

Ans: N/A, LO: 2, Bloom: K, Difficulty: Easy, Min: 5, AACSB: Communications, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Measurement, AICPA

PC: Communications, IMA: FSA

Solution 273

S-A E 274

Tim Forsyth, the CEO of Magical Products, is a successful entrepreneur and his focus is his

products, not his accounting system. He asks you to explain to him, in a memo, the bases of

comparison for ratio analysis.

Ans: N/A, LO: 3, Bloom: K, Difficulty: Easy, Min: 5, AACSB: Communications, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA PC:

Communications, IMA: Performance Measurement

Solution 274

Financial Analysis: The Big Picture

FOR INSTRUCTOR USE ONLY

13-93

S-A E 275

Horizontal and vertical analyses are analytical tools frequently used to analyze financial

statements. What type of information or insights can be obtained by using these two techniques?

Explain how the output of horizontal analysis and vertical analysis can be compared to industry

averages and/or competitive companies.

Ans: N/A, LO: 4, 5, Bloom: C, Difficulty: Easy, Min: 5, AACSB: Communications, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA

PC: Communications, IMA: Performance Measurement

Solution 275

S-A E 276

What does each type of ratio measure?

(a) Liquidity ratios.

(b) Solvency ratios.

(c) Profitability ratios.

Ans: N/A, LO: 6, 8, Bloom: K, Difficulty: Easy, Min: 5, AACSB: Communications, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA

PC: Communications, IMA: Performance Measurement

Solution 276

S-A E 277

Identify and explain factors that affect quality of earnings.

Ans: N/A, LO: 7, Bloom: C, Difficulty: Easy, Min: 5, AACSB: Communications, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA PC:

Communications, IMA: Performance Measurement

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

13-94

Solution 277

S-A E 278 (Communication)

Zip Delivery specializes in the overnight transportation of medical equipment and laboratory

specimens. The company has selected the following information from its most recent annual

report to be the subject of an immediate press release.

• The financial statements are being released.

• Net income this year was $3.1 million. Last year's net income had been $2.8 million.

• The current ratio has changed to 2:1 from last year's 1.6:1.

• The debt to assets ratio has changed to 4:6 from last year's 3:6.

• The company expanded its truck fleet substantially by purchasing ten new delivery vans.

• The company already had twelve delivery vans. The company is now the largest medical

courier in the mid-Atlantic region.

Required:

Prepare a brief press release incorporating the above information. Include all information. Think

carefully which information (if any) is good news for the company, and which (if any) is bad news.

Ans: N/A, LO: 6, 8, Bloom: S, Difficulty: Easy, Min: 5, AACSB: Communications, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA

PC: Communications, IMA: Performance Measurement

Solution 278

Financial Analysis: The Big Picture

13-95

IFRS QUESTIONS

1. Under IFRS, there is no classification for

a. changes in accounting estimates.

b. changes in accounting principles.

c. discontinued operations.

d. extraordinary items.

2. The accounting for each of the following is the same under IFRS and GAAP except for

a. extraordinary items.

b. discontinued operations.

c. changes in accounting principles.

d. changes in accounting estimates.

3. Distinguishing normal levels of income from irregular items is of interest for the

FASB IASB

a. no no

b. no yes

c. yes no

d. yes yes

4. All revenue and expense items are considered ordinary in nature under

a. both IFRS and GAAP.

b. GAAP.

c. IFRS.

d. neither IFRS or GAAP.

5. Under IFRS, the statement of comprehensive income can be prepared under

a. the one-statement approach only.

b. the two-statement approach only.

c. either the one-statement approach or the two-statement approach.

d. either the two-statement approach or the stockholders' equity statement approach.

6. Under IFRS, the components of other comprehensive income can be reported in each of the

following ways except

a. the one-statement approach.

b. the two-statement approach.

c. the statement of stockholders' equity approach.

d. All of the above are acceptable.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

13-96

7. Which of the following is not an acceptable way of displaying the components of other

comprehensive income?

a. Combined statement of retained earnings

b. Second income statement

c. Combined statement of comprehensive income

d. All of these answer choices are acceptable.

8. Under IFRS, other comprehensive income must be displayed(reported) in

a. the equity section of the statement of financial position.

b. a second income income statement.

c. the income statement.

d. the retained earnings statement.