Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Business Activities—The Source of Accounting Information ♦ 67

72. A credit entry is used to record increases to

a.

cost of goods sold

b.

notes payable

c.

wages expense

d.

cash

73. As used in accounting, what do the terms "debit" and "credit" mean?

a.

bad and good things, respectively, that happen to a business

b.

down and up, respectively

c.

left and right sides, respectively, of an account

d.

first and second, respectively

MATCHING

For each of the account names below, identify which type of account it is. Use the following

identification system:

a.

asset

b.

liability

c.

owners' equity

d.

revenue

e.

expense

1. Contributed capital

2. Cost of goods sold

3. Land

4. Supplies inventory

5. Investment by owners

6. Retained earnings

7. Notes payable

8. Employee wages

9. Sales

10. Merchandise inventory

11. Cash

12. Equipment

68 ♦ Chapter 2

Indicate the organizational activity which best describes the events listed below:

a.

Financing

b.

Investing

c.

Operating

13. Issuance of Stock

14. Payment of wages

15. Purchase of land

16. Sale of merchandise

17. Borrowing money

18. Sale of old equipment

Business Activities—The Source of Accounting Information ♦ 69

For each of the following transactions for Bartlett Co., indicate whether it is a:

a.

Financing Activity

b.

Investing Activity

c.

Operating Activity

19. Borrowed $45,000 from a bank

20. Paid $300 for electricity

21. Paid $3,000 for a delivery truck

22. Paid $600 toward the loan in #19 above

23. Received $3,000 cash from owner

24. Paid $800 for inventory

25. Sold Equipment for $1,000

26. Received $900 for sale of inventory

27. Paid $2,000 to employees for wages

28. Owner withdrew $75

70 ♦ Chapter 2

PROBLEM

1. William & Sons had the following transactions during February:

1. Received cash from owners investing in the business.

2. Paid wages for February.

3. Purchased equipment and signed a note payable for payment in the future.

4. Performed services for customers for cash.

5. Paid utilities for February.

6. Paid an amount on the note payable(in #3) .

Required:

For each transaction, show how its financial effects would affect the different elements of the

firm's accounting system. Indicate increases with a plus (+) sign and decreases with a minus (-).

Where there is no effect on an item, leave the space blank.

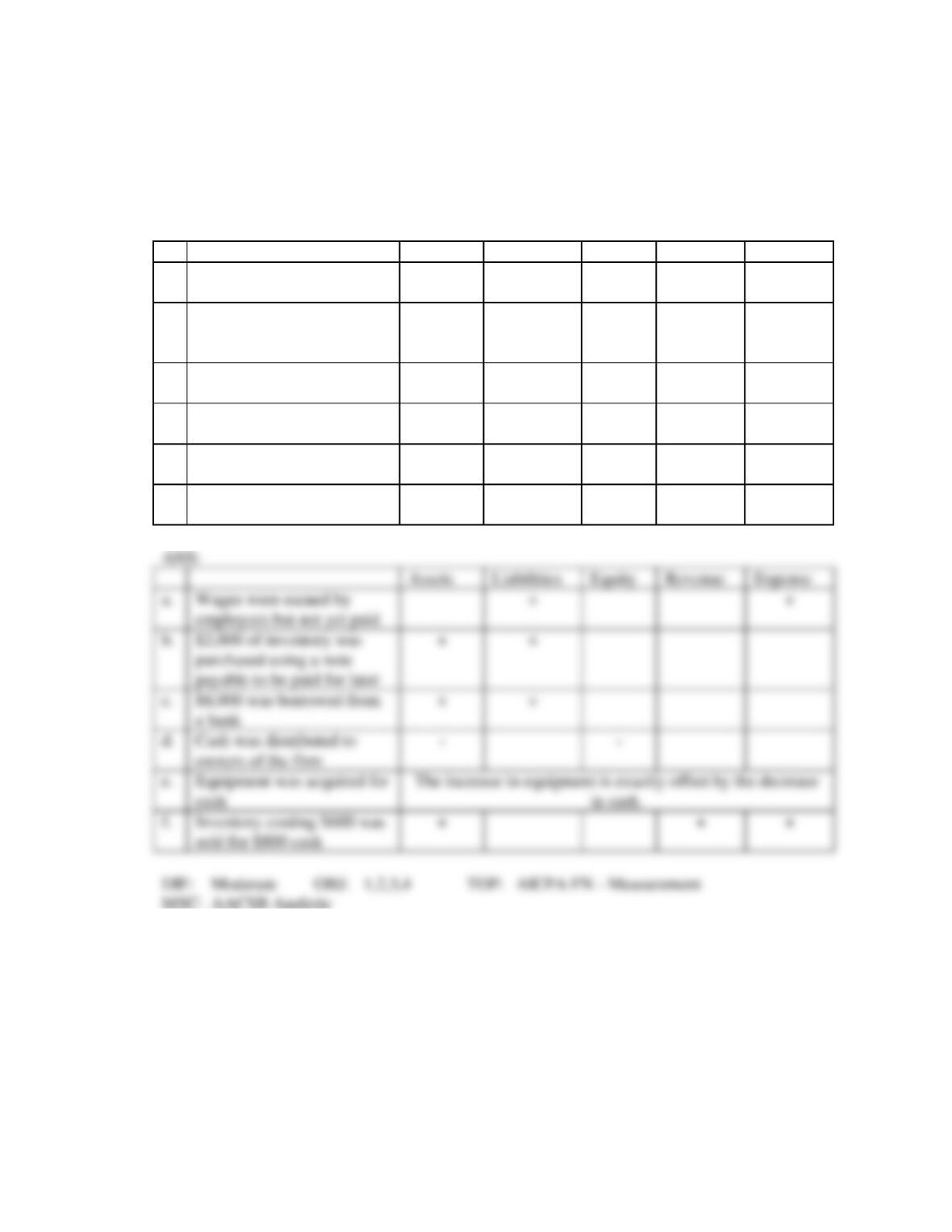

Item

Assets

Liabilities

Equity

Revenue

Expenses

ANS:

Business Activities—The Source of Accounting Information ♦ 71

2. For each event below, determine which of the categories in the firm's accounting system would be

changed. If a category would increase, indicate this with a plus (+). If a category would decrease,

indicate this with a minus (-). If a category would not change, leave that line blank. (Item "a" is

completed as an example.)

NOTE: Do NOT make entries to the accounting system here. Instead, you are determining the

EFFECT of a transaction on account balances.

Assets

Liabilities

Equity

Revenue

Expense

a.

Wages earned by employees

but not yet paid

+

+

b.

$2,000 of inventory was

purchased using a note

payable to be paid later

c.

$8,000 was borrowed from

a bank

d.

Cash was distributed to

owners of the firm

e.

Equipment was acquired for

cash

f.

Inventory costing $600 was

sold for $800 cash

72 ♦ Chapter 2

3. Adams Enterprises had the following events occur during a recent month. For each event,

determine which of the categories in the firm's accounting system would be changed. If a category

would increase, indicate this with a plus (+). If a category would decrease, indicate this with a

minus (-). If a category would not change, leave that line blank. (Item "a" is completed as an

example.)

NOTE: Do NOT make entries to the accounting system here. Instead, you are determining the

EFFECT of a transaction on account balances.

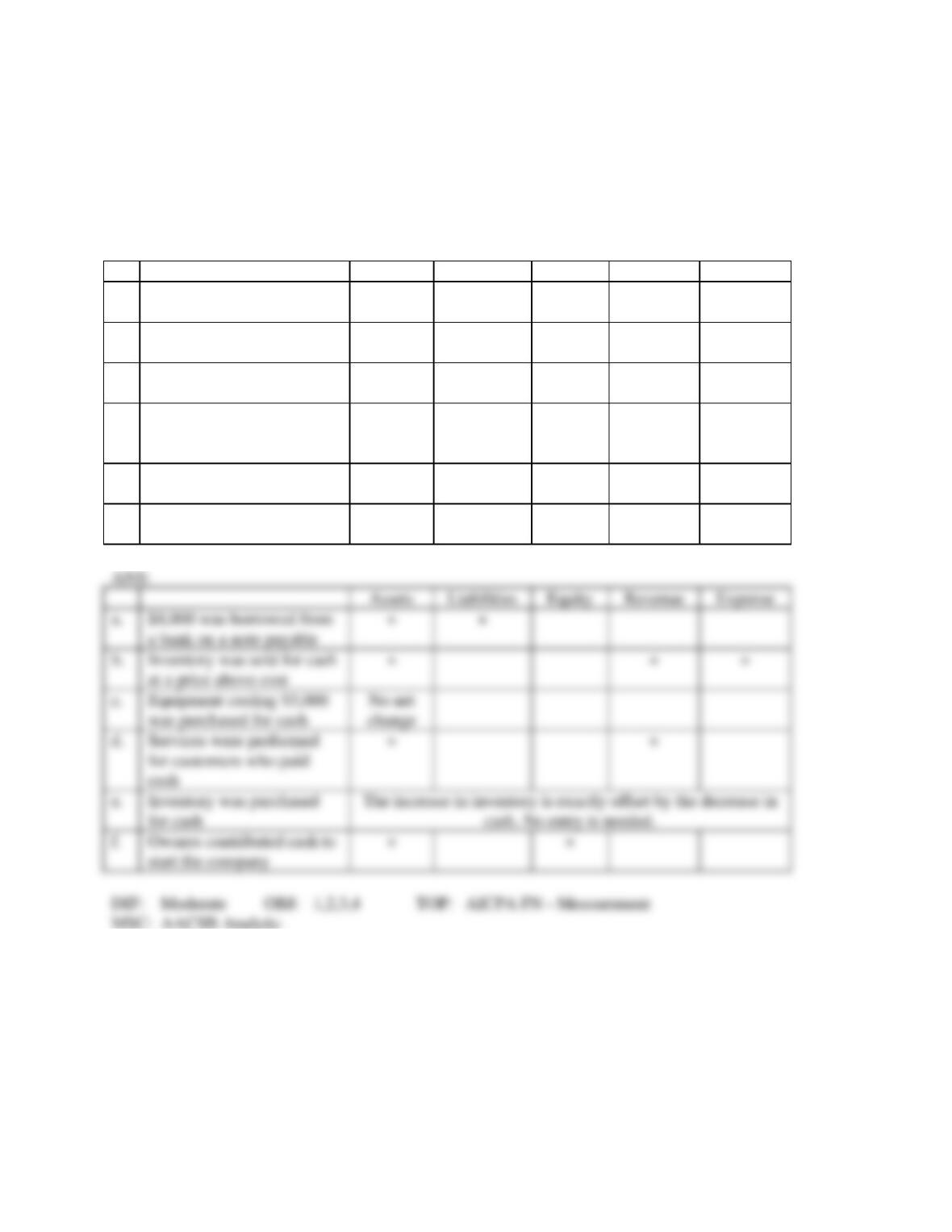

Assets

Liabilities

Equity

Revenue

Expense

a.

$8,000 was borrowed from

a bank on a note payable

+

+

b.

Inventory was sold for cash

at a price above cost

c.

Equipment costing $5,000

was purchased for cash

d.

Services were performed

for customers who paid

cash

e.

Inventory was purchased

for cash

f.

Owners contributed cash to

start the company

Business Activities—The Source of Accounting Information ♦ 73

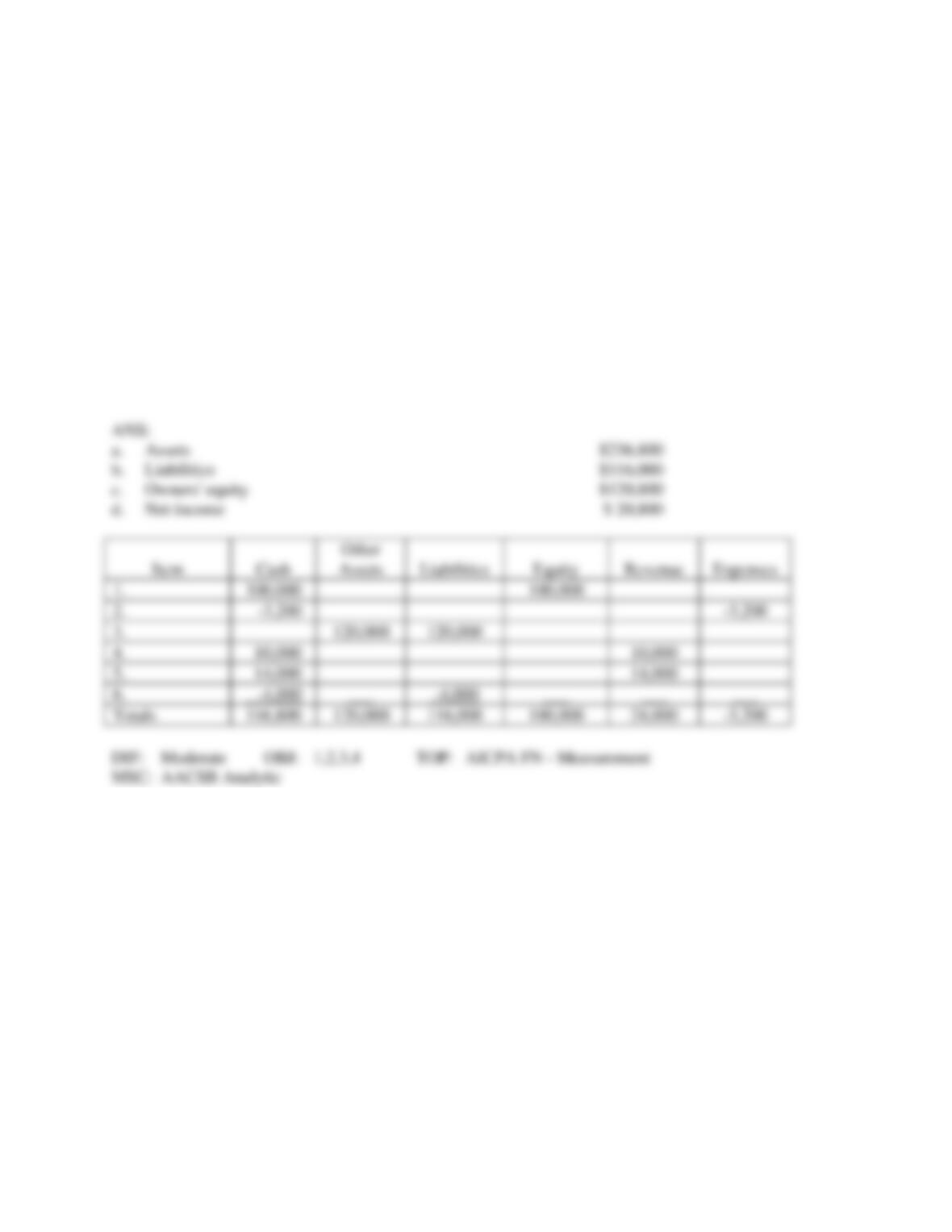

4. Young & Company completed the following transactions during October, its first month of

operations:

1. Owners invested $60,000 cash in the business.

2. $1,800 was paid for one month's office rent.

3. Equipment was purchased by signing a $8,000 note.

4. Services were performed for customers for $5,000 cash.

5. Goods were sold to customers for $8,000 cash.

6. Paid $2,000 on the note signed in transaction #3.

Required:

After these transactions, what is the total amount of:

a. Assets

b. Liabilities

c. Owners' equity

d. Net income

74 ♦ Chapter 2

5. Seaside Company completed the following transactions during, March, its first month of

operations:

1. Owners invested $100,000 cash in the business.

2. $3,200 was paid for one month's office rent.

3. Equipment was purchased by signing a $120,000 note.

4. Services were performed for customers for $10,000 cash.

5. Goods were sold to customers for $14,000 cash.

6. Paid $4,000 on the note signed in transaction #3.

Required:

After these transactions, what is the total amount of:

a.

Assets

b.

Liabilities

c.

Notes payable

d.

Owners' equity

Business Activities—The Source of Accounting Information ♦ 75

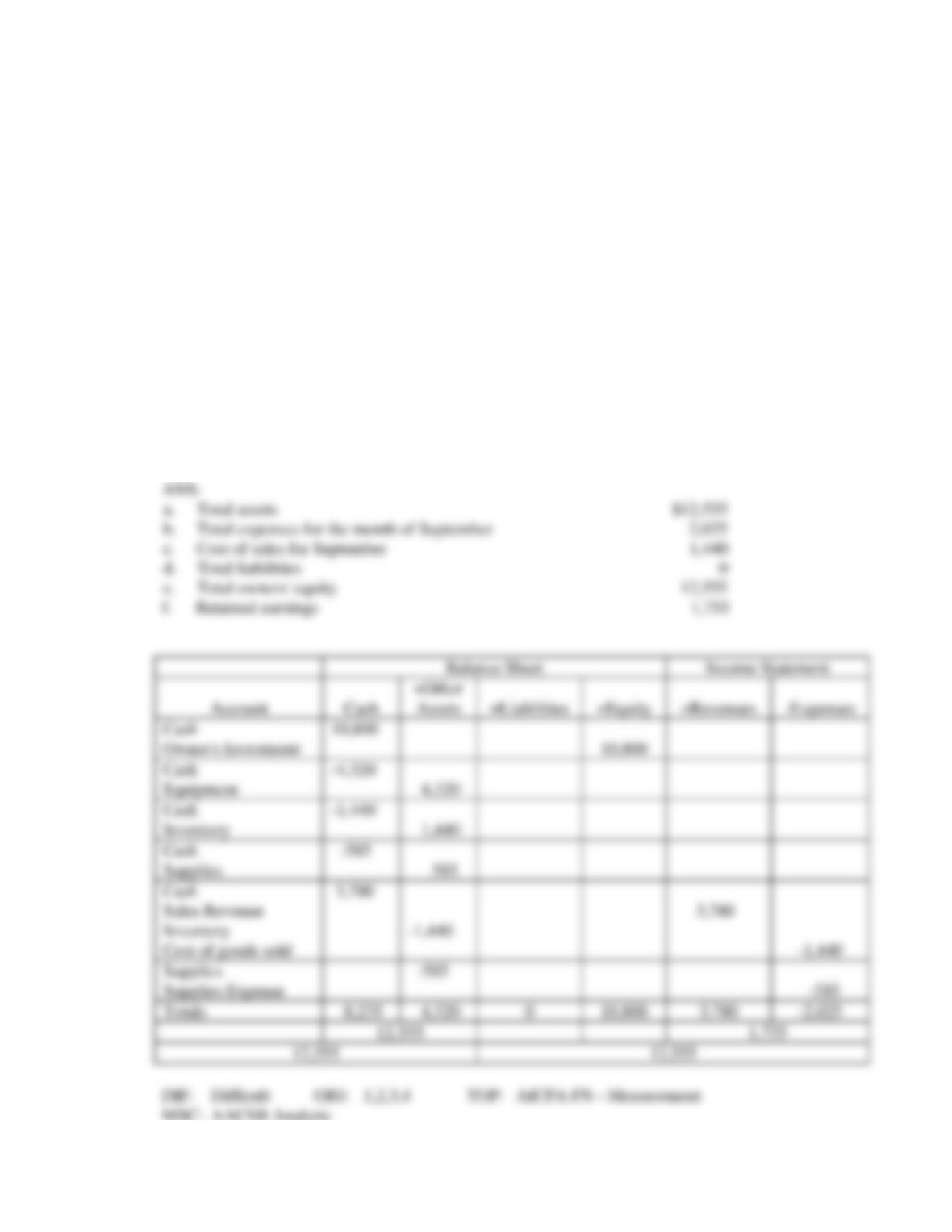

6. Marine Stock Company began business on September 1. Transactions for the first month of

business were as follows:

Sept 1:

Tony and Ken each contributed $5,400 to the firm.

Sept 5:

Equipment costing $4,320 was purchased with cash.

Sept 12:

Inventory costing $1,440 was acquired for cash.

Sept 21:

Supplies having a cost of $585 were purchased for cash.

Sept 25:

The entire inventory was sold to a customer for $3,780 cash.

Sept 30:

The last of the supplies were used up.

Required:

Answer the following questions as of the close of business on September 30:

a.

Total assets

b.

Total expenses for the month of September

c.

Cost of sales for September

d.

Total liabilities

e.

Total owners' equity

f.

Retained earnings

76 ♦ Chapter 2

7. The five major categories of information in an accounting system are assets, liabilities, equities,

revenues, and expenses. Below are listed several business events. Indicate which category (or

categories) of information will be INCREASED by each event.

Information category (or categories)

that will increase

a.

An auto dealership sold three

cars, costing a total of $60,000,

for $90,000.

b.

Mark Evers, the owner of Evers Company,

rented a video projector to show his

employees three training films. At

the time of renting, he paid the fee.

c.

Fox Drugstore borrowed $6,000

from the local bank.

d.

Martin Supply paid $8,000 to its

landlord for the current month's

rent.

e.

Sage Corporation sold $200,000 in

stock to investors.

Business Activities—The Source of Accounting Information ♦ 77

8. For each of the transactions that follow, identify the accounts in the accounting system that would

be affected by the transaction and indicate whether the account balance would increase or

decrease:

Transaction

Account

Increase or

Decrease?

a.

Three partners invested

$50,000 in their partnership.

b.

A carpet cleaning business

cleaned the carpeting in an

office building for $1,000

cash.

c.

Office supplies costing $300

were used during the month.

d.

Owners withdrew cash

totaling $15,000.

e.

A grocery sold inventory

costing $25,000, for $35,000.

f.

Meyerson Company paid off

a $800 note it owed to a

supplier.