Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

International Economics, 10e (Krugman/Obstfeld/Melitz)

Chapter 20 (9) Financial Globalization: Opportunity and Crisis

20.1 The International Capital Market and the Gains from Trade

1) If you are offered a gamble in which you win 500 dollars 3/8 of the time and you lose 500

dollars 5/8 of the time, what is your expected payoff and your behavior given that you are a risk-

lover?

A) $500, take the gamble

B) -$125, take the gamble

C) -$125, it is unclear what you would do without further information

D) $500, decline the gamble

E) -$125, decline the gamble

2) The two types of trade, intertemporal and pure asset swap ________ perfect substitutes,

because ________.

A) are; they both offer considerable payoff and are equal in the long run

B) are; they both involve the smoothing out of now and future consumption

C) are not; asset swapping is immediate and involves only assets, while intertemporal trade takes

two time periods and involves both assets and goods/services

D) could possibly be; different economic states occur at different points in time

E) are not; asset swapping never relates to intertemporal trade

3) For the following question assume the following facts:

(1) Balance of Payments = 0 prior to the transactions.

(2) Person A (who lives in the United States) purchases an airplane from British Airways for

$150,000.

(3) Person A pays with a check from his account at First Union Bank in the United States.

(4) British airways, since it will need dollars in 1 month, deposits the check at the Bank of

England.

(5) Bank of England deposits the $150,000 at Commonwealth bank, which is located in the

United States.

Due to the transactions above, what are the effects on the balance of payments?

A) -$150,000 due to import of good (current account debit)

B) +$150,000 due to import of good (current account credit)

C) -$150,000 due to deposit of Bank of England (capital account debit)

D) +$150,000 due to deposit of Bank of England (capital account credit)

E) No effect (150,000 current account debit and 150,000 capital account credit)

4) For the following questions assume the following facts:

(1) Balance of Payments = 0 prior to the transactions.

(2) Person A (who lives in the United States) purchases an airplane from British Airways for

$150,000.

(3) Person A pays with a check from his account at First Union Bank in the United States.

(4) British airways, since it will need dollars in 1 month, deposits the check at the Bank of

England.

(5) Bank of England deposits the $150,000 at Commonwealth bank, which is located in the

United States.

Due to the transactions above, what are the effects on the reserve at the Fed?

A) Fact 2 is a decrease of $150,000, fact 5 is a decrease of $150,000, a net effect of -$300,000.

B) Fact 3 is a decrease of $150,000, fact 5 is an increase of $150,000, a net effect of 0.

C) Fact 3 is an increase of $150,000, fact 5 is a decrease of $150,000, a net effect of 0.

D) Both fact 3 and fact 5 result in increases of $150,000, a net effect of +$300,000.

E) Both fact 3 and fact 5 result in decrease of $150,000, a net effect of -$300,000.

5) Suppose one is offered a gamble in which you win $1,000 half the time but lose $1,000 half

the time. Since in this case one is as likely to win as to lose the $1,000, the average payoff on this

gamble—its expected value—is:

0.5 ∗ $1,000 + 0.5 ∗ (-$1,000) = 0.

Under such circumstances:

A) no one will take the gamble.

B) risk averse individuals will take the gamble.

C) risk lovers individuals will not take the gamble.

D) risk neutral individuals will not take the gamble.

E) risk lovers and risk neutral individuals may take the gamble.

6) For most practical matters, economists assume that

A) individuals are risk neutral.

B) individuals are risk lovers.

C) individuals are risk averse.

D) most individuals are risk lovers.

E) most individuals are risk neutral.

7) People who are risk averse

A) value a collection of assets only on the basis of its expected returns.

B) value a collection of assets only on the basis of the risk of that return.

C) value a collection of assets not only on the basis of its expected returns but also on the basis

of the risk of that return.

D) are less likely to invest in life insurance.

E) are less likely to have a diverse portfolio.

8) The idea of risk aversion

A) is at odds with the idea of insurance.

B) help explain the profitability of insurance companies.

C) has nothing to do with insurance companies.

D) help explain the losses suffers by the insurance industry.

E) help explain why insurance companies in the long run are zero profit companies.

9) Risk averse people

A) will never hold bonds denominated in several different currencies because of transaction

costs.

B) will always hold bonds denominated in several different currencies because of transaction

costs.

C) may hold bonds denominated in several different currencies.

D) may hold bonds denominated in several different currencies only if satisfying the well known

interest party condition.

E) will hold only domestic bonds because of the home bias effect.

10) Imagine that there are two countries, Home and Far Far Away, and that residents of each

own only one asset, domestic land yielding an annual harvest of mangoes. Assume that the yield

on the land is uncertain. Half the time, Home's land yields a harvest of 5,000 tons of mangoes at

the same time as Far Far Away's land yields a harvest of 2,500 tons. The other half of the time

the outcomes are reversed. The average for each country mango harvest is

A) 2500.

B) 2750.

C) 3500.

D) 3750.

E) 3000.

11) Equity Instruments include

A) stocks.

B) bonds.

C) banks deposits.

D) receipts.

E) bank statements.

12) What would best describe the international capital markets?

A) the market of exchange of bonds

B) the market of exchange of stocks

C) the market of exchange of real-estate

D) the market in which residents of different countries trade assets

E) the currency market

13) Describe three types of gains from trades?

A) trades of exchange rates for goods or services, trades of goods or services for property, and

trades of gold for textiles

B) trades of goods or services for goods or services, trades of goods or services for assets, and

trades of assets for assets

C) trades of imports for exports, trades of exports for imports, and trades of natural resources for

financial assets

D) trades of services for goods, trades of currency for services, and trades of one type of

currency for another

E) trades of current goods for future services, trades of currency for gold, and trades of one type

of currency for another

14) Asset trades that deal with debt instruments are best described as

A) share of stock.

B) exchange rate.

C) receipts.

D) factors.

E) bonds or bank deposits.

15) Asset trades that deal with equity instruments are best described as

A) share of stock.

B) exchange rate.

C) bonds.

D) bank deposits.

E) factors.

16) The international capital market is:

A) the international currency exchange.

B) a market in which capital assets are exchanged for services.

C) the market that is subject to intense regulation and must file a report to the Basel committee

on a biannual basis.

D) not really a single market, but a group of closely interconnected markets in which asset

exchanges with some international dimension take place.

E) an organization of fiscal policies that dictate international trade.

17) Intertemporal trade is

A) the exchange of goods but not services for claims to future goods.

B) the exchange of services but not goods for claims to future services.

C) the exchange of good and services for claims to future goods and services.

D) the exchange of domestic goods and services for foreign goods and services.

E) the type of trade that the U.S. government focuses most upon.

18) What is the basic motive for asset trade?

A) the belief that large risks will lead to large returns

B) restoration of the balance of payments

C) portfolio unification

D) economic stability

E) increase expected returns and reduced risk

19) Using international asset trade, countries can

A) never really eliminate all risk.

B) eliminate all risk.

C) actually increase their risk in some cases.

D) eliminate all their risk except for emerging markets.

E) never really diversify their holdings.

20) What are the three types of transactions between the residents of different countries?

21) What are the three types of gains from international transactions between the residents of

different countries?

22) How international trade in assets can make both countries better off?

23) Explain Tobin's idea of "Don't put all your eggs in one basket."

24) Why is it useful to make a distinction between debt and equity instruments?

25) Define risk aversion and give an example of a risk-averse person?

26) Why is portfolio diversification so important in international trade?

27) What is the difference between equity instruments and debt instruments?

28) Why is the foreign exchange market so vital?

29) Suppose you are offered a gamble in which you win $1,000 half the time but lose $1,000 half

the time. If you are risk averter will you take the gamble?

30) Suppose you are offered a gamble in which you win $1,000 1/3 half the time but lose $800

2/3 half the time. If you are risk lover will you take the gamble? What will your expected payoff

be?

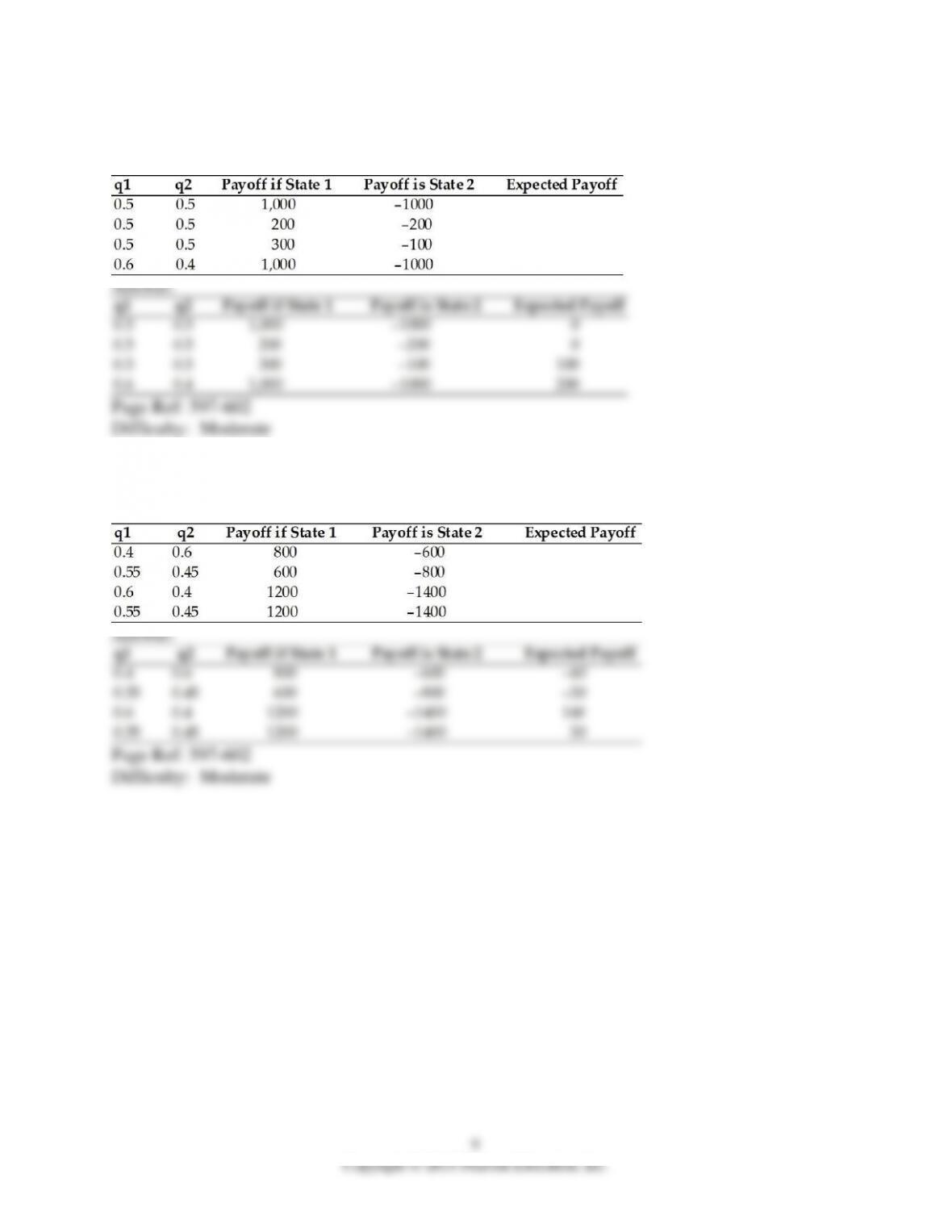

31) Calculate the expected payoff for the following cases, where q1 and q2 are the probabilities

of state 1 and 2, respectively.

32) Calculate the expected payoff for the following cases, where q1 and q2 are the probabilities

of state 1 and 2, respectively.

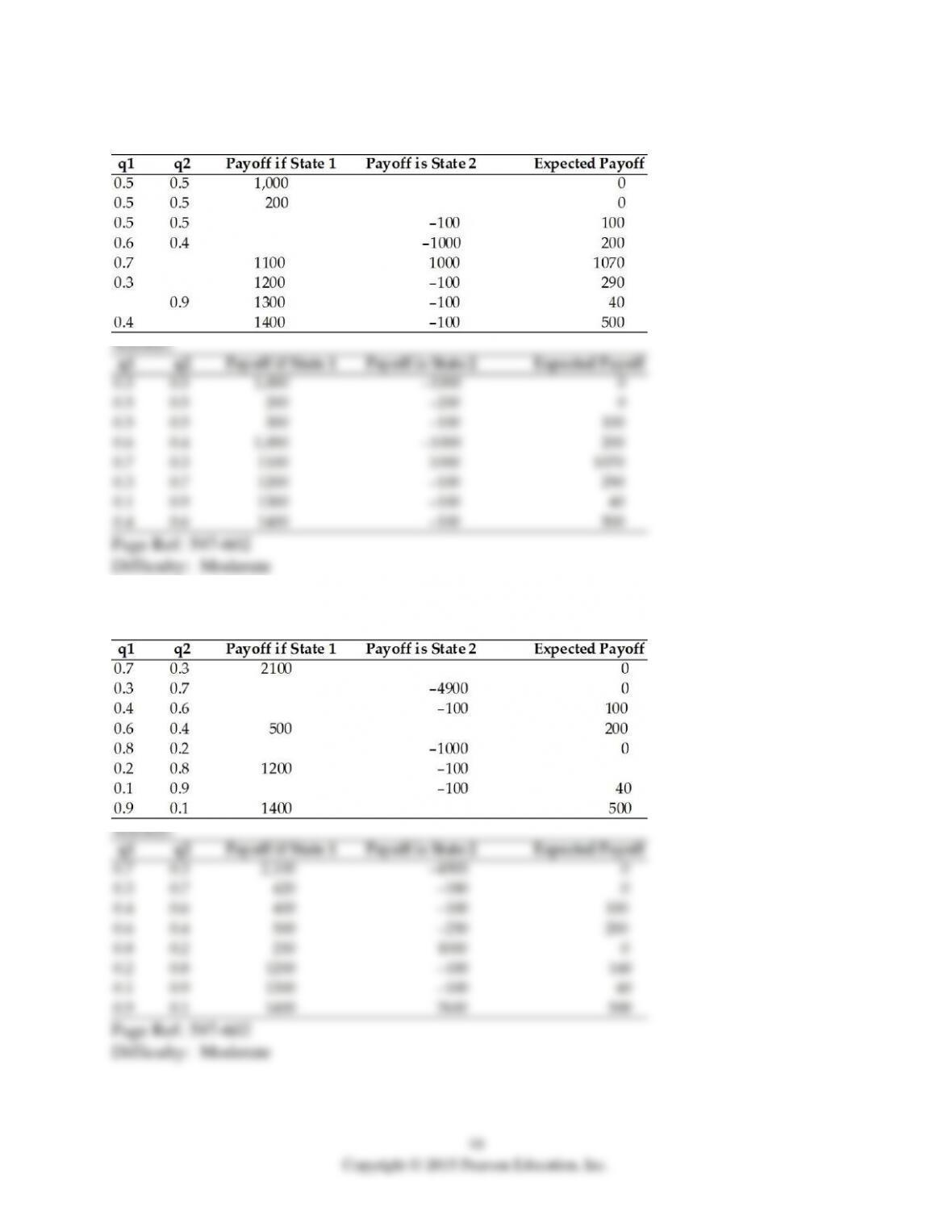

33) Complete the following table.

34) Complete the following table.

11

Copyright © 2015 Pearson Education, Inc.

The following simple two-country question illustrates how countries are made better off by trade

in assets. Imagine that there are two countries, Home and Foreign, and that residents of each own

only one asset, domestic land yielding an annual harvest of kiwi fruit. Assume that the yield on

the land is uncertain. Half the time, Home's land yields a harvest of 100 tons of kiwi fruit at the

same time as Foreign's land yields a harvest of 50 tons. The other half of the time the outcomes

are reversed. The Foreign's harvest is 100 tons, but the Home harvest is only 50.

35) Calculate the average, for each country of kiwi harvest.

36) Suppose the two countries can trade shares in the ownership of their perspective assets.

Further, assume that a Home owner of a 10 percent share in Foreign land. He will receive 10

percent share in Foreign land, and thus receives 10 percent of the annual Foreign kiwi fruit

harvest. Further assume that a Foreign owner of a 10 percent share in Home land is permitted. In

this case, a Foreigner is entitled to 10 percent of the Home harvest. Calculate the expected value

of kiwi fruit for each investor. Is the investor better off?

37) Suppose the two countries can trade shares in the ownership of their perspective assets.

Further assume that a Home owner of a 25 percent share in Foreign land. He will receive 25

percent share in Foreign land and thus receives 25 percent of the annual Foreign kiwi fruit

harvest. Further assume that also that a Foreign owner of a 25 percent share in Home land is

permitted. In this case, a Foreigner is entitled to 25 percent of the Home harvest. Calculate the

expected value of kiwi fruit for each investor.

38) Suppose the two countries can trade shares in the ownership of their perspective assets

without any restrictions. Assume that the consumers in both countries would like to totally

smooth their consumption. Describe the outcomes.

39) Suppose that trade in asset is not allowed but the two countries sign a treaty that guarantee

the sending of 25 tons of kiwi in good time by the high output country in that season. What will

the outcome of such a treaty? Explain why.

13

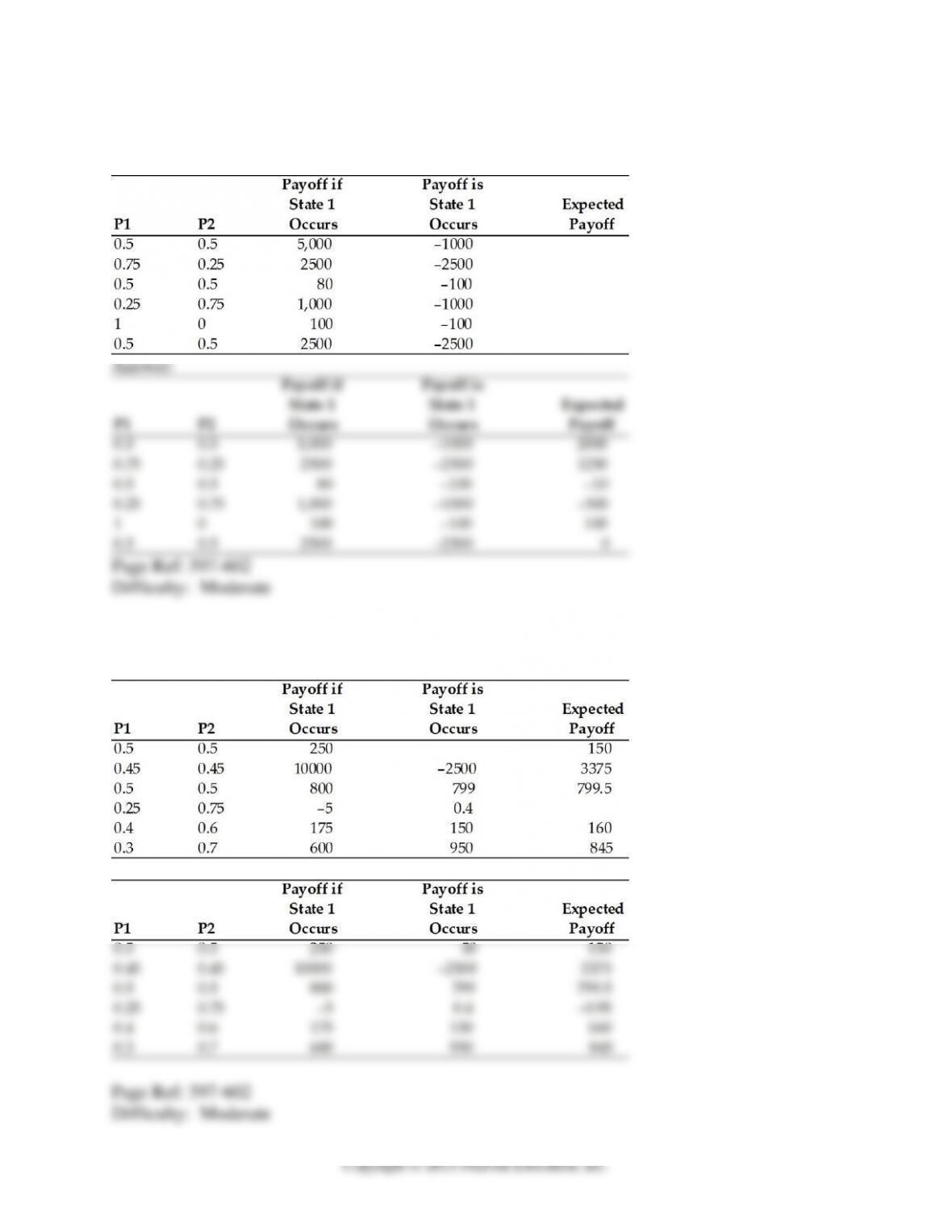

40) Calculate the expected payoff for the following cases with the formula: (P1) * (payoff if state

1) + (P2) * (payoff if state 2), where P1 and P2 are the probabilities of state 1 and 2, respectively.

41) Complete the following table with the formula (P1) * (payoff if state 1) + (P2)* (payoff if

state 2), where P1 and P2 are the probabilities of state 1 and 2, respectively.

Answer:

1) As a country begins to liberalize its capital account, what would you expect to happen to the

difference between the interest rates for similar assets in this country and another country with

open capital markets?

A) get larger

B) get smaller

C) stay the same

D) it depends on the existing exchange rate.

E) exponential divergence

2) Investment banks in the U.S. are

A) regular banks specializing in investment projects.

B) not banks at all but institutions which specialize in underwriting sales of stocks and bonds.

C) special arm of the U.S. government for U.S. banks operating outside the U.S.

D) regular banks specializing in investment projects, but allowed to offer limited domestic

transactions.

E) international banks that are heavily invest in the U.S.

3) Credit Suisse, Goldman Sachs, and Lazard Freres are examples of

A) commercial banks.

B) corporations.

C) non-bank financial institutions, such as insurance companies, pension funds, and mutual

funds. This includes investment banks, which specialize in underwriting sales of stocks and

bonds by corporations and in some cases governments.

D) central banks and other government agencies.

E) non-profit organizations.

4) A country can control

A) its flexible exchange rate.

B) monetary policy oriented toward domestic goals.

C) international capital movements.

D) foreign inflationary policies.

E) and avoid risks in international trade.

5) Under a gold standard, countries control

A) its flexible exchange rate.

B) monetary policy oriented toward domestic goals.

C) international capital movements.

D) foreign inflationary policies.

E) and avoid risks in international trade.

6) After Bretton Woods period, countries chose to control

A) fixed exchange rate only.

B) monetary policy oriented toward domestic goals only.

C) freedom of international capital movements only.

D) fixed exchange rate and freedom of international capital movements.

E) fixed exchange rate and monetary policy oriented toward domestic goals.

7) Under the unified Euro regime, the European countries control

A) fixed exchange rate only.

B) monetary policy oriented toward domestic goals only.

C) freedom of international capital movements only.

D) monetary policy oriented toward domestic goals and freedom of international capital

movements.

E) fixed exchange rate and freedom of international capital movements.

8) Which one of the following possibilities is TRUE?

A) Much of eurocurrency trading occurs in Europe.

B) Much of eurocurrency trading occurs in the United States.

C) Eurocurrencies trading occurs everywhere except the United States.

D) Eurocurrencies trading occurs everywhere except Europe.

E) Eurocurrencies trading occurs everywhere except China.

9) Eurodollars are

A) dollar deposits located in the United States.

B) dollar deposits located in Europe.

C) dollar deposits located outside Europe.

D) dollar deposits located outside the United States.

E) dollar deposits located outside both Europe and the United States.

10) Eurobanks are

A) all European Banks.

B) all non American banks.

C) banks that accept deposits denominated in Eurocurrencies excluding Eurodollars.

D) banks that accept deposits denominated in Eurocurrencies including Eurodollars.

E) banks that do not take U.S. dollars.

11) The leading center of Eurocurrency trading is

A) New York City.

B) Chicago.

C) London.

D) Paris.

E) Frankfurt.

12) The Fed's Regulation Q

A) placed a ceiling on the interest rates U.S. banks could pay on time deposits to foreigners.

B) placed a ceiling on the interest rates U.S. banks could pay on time deposits.

C) placed a ceiling on the amount U.S. residents can deposits in Euro banks.

D) placed a ceiling on the amount foreign residents can deposits in domestic American banks.

E) placed a ceiling on the amount foreign banks can pay on time deposits.

13) Which type of main institution in the international capital market most often is involved in

foreign exchange intervention?

A) central banks

B) non-bank financial institutions

C) insurance companies

D) corporations

E) commercial banks

14) The difference between an agency office located abroad and a subsidiary bank located

abroad is

A) an agency office is just a home bank in another country while a subsidiary bank is controlled

by a foreign bank and subject to the same regulations as local banks.

B) an agency office is just a home bank in another country while a subsidiary bank arranges

loans and transfers funds but does not accept deposits.

C) an agency office arranges loans and transfers funds but does not accept deposits while a

subsidiary bank is controlled by a foreign bank and subject to the same regulations as local

banks.

D) an agency office arranges loans and transfers funds but does not accept deposits while a

subsidiary bank is just a home bank in a foreign country.

E) an agency office is controlled by a foreign bank and subject to the same regulations as local

banks while a subsidiary bank arranges loans and transfers funds but does not accept deposits.

15) Besides world trade growth, what can explain the growth of international banking since the

1960s?

A) war in the Middle East

B) government focus on banking regulation.

C) an increase in world travel.

D) the emergence of developing countries like China.

E) desire of depositors to hold currencies outside the jurisdiction of the countries that issue them

16) The Eurodollar market's early growth was stimulated by the Cold War between the United

States and U.S.S.R. Why?

A) Soviets feared the U.S. might confiscate dollars place in American banks if conditions of

Cold War were to worsen.

B) The United States didn't feel safe holding as many dollars in American banks.

C) The Cold War did not stimulate the Eurodollar market's early growth.

D) Developing technologies required larger money transfers than central banks could handle.

E) Soviets developed a new banking system with new allies developed during the tension.

17) Rising inflationary pressure caused the U.S. to tighten its monetary policy at the end of the

1960s. As a result, market interest rates rose above the Regulation Q ceiling and American banks

found it impossible to attract time deposits for re-lending. How did the banks get around this

problem?

A) by setting their own interest rates and then using better business as compensation for

government regulations

B) by borrowing funds from European branches, which faced no restriction on the interest they

could pay on Eurodollar deposits

C) by pushing through new legislation that nullified Regulation Q

D) by creating subsidiary branches in foreign countries

E) by waiting to trade time deposits until Regulation Q no longer applied

18) What structures make up the international capital markets?

A) stock market, IFM, and the World bank

B) bond market, foreign exchange rates, IFM, and the World bank

C) commercial banks, corporations, non-bank financial institutions, the central banks, and other

government agencies

D) commercial banks and corporations

E) the central banks and non-bank financial institutions

19) What are the types of institution banks used to conduct foreign business?

A) corporations

B) central banks

C) commercial banks

D) agency offices, subsidiary banks, and foreign branches

E) state-owned enterprises

20) A business's use of a bank located outside of the home country is called

A) Swiss banking.

B) offshore banking.

C) international banking.

D) domestic banking.

E) international swapping.

21) The scale of transactions in the international capital market has

A) grown more quickly than world GDP since the early 1970s.

B) grown less quickly than world GDP since the early 1970s.

C) grown about the same rate as the world GDP since the early 1970s.

D) been fixed by international regulations.

E) decreased more quickly than world GDP since the early 1970s.

22) If a country chooses to have a monetary policy oriented toward domestic goals and a fixed

exchange rate, then

A) it can have the freedom of international capital movements.

B) it cannot have the freedom of international capital movements.

C) it cannot balance its current account.

D) it cannot have fiscal policy oriented toward domestic goals.

E) it cannot control money supply growth.

23) If a country chooses to have a monetary policy oriented toward domestic goals and the

freedom of international capital movements, then

A) it can have a fixed exchange rate.

B) it cannot have a fixed exchange rate.

C) it cannot balance its current account.

D) it cannot have a fiscal policy oriented toward domestic goals.

E) it cannot control money supply growth.

24) Offshore banking can take place at which institution?

A) agency office only

B) subsidiary bank only

C) foreign bank only

D) subsidiary bank and foreign bank

E) agency office, subsidiary bank, and foreign bank

25) The fact that assets of the political opponents of the U.S. were frozen in U.S. banks

A) was challenged as unconstitutional.

B) lead to an increased amount of funds being placed in Eurobanks.

C) lead to a violation of the Law of One Price.

D) lead to the Cold War.

E) lead to a violation of Regulation Q.

26) Regulatory asymmetries can explain why the following places have become main

Eurocurrency centers

A) the United States.

B) Germany.

C) Zurich, Somalia, and Mozambique.

D) London, Luxembourg, and The United States.

E) London, Luxembourg, and Hong Kong.

27) Who are the main actors in the international capital market?